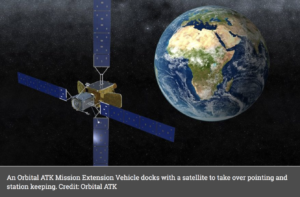

Servicing satellites in geosynchronous orbit is a “nascent industry” with significant future potential. Companies are weighing “service-or-replace trade-offs.” In an uncertain business climate, satellite manufacturers and operators are looking for new ways to manage their fleets, and might find life-extension services a compelling option. NSR in January published the industry’s first study on the in-orbit.

Following the launch of the Gaofen 6 satellite last weekend, China matched – and three days later surpassed – its 2017 launch rate a mere 5 months into the year. If China achieves its planned cadence to exceed 40 launches in 2018, it would more than double last year’s total and quadruple the rate of.

Satellite capacity prices have dropped by 35 to 60 percent over the past two years, according to Northern Sky Research, with high-throughput satellites contributing to the decline.

According to Northern Sky Research’s (NSR) Aeronautical Satcom Markets, 6th Edition report, In-flight connectivity revenue will be driven primarily by new HTS services and greater penetration in all regions of the world. NSR projects that demand will reach almost 295 Gbps of high-throughput satellite (HTS) capacity and more than 92 transponders of FSS Ku-band demand.

Forecasters at Northern Sky Research (NSR) said they expect to see a near-doubling of inflight-connectivity (IFC) revenue and 50% more aircraft with IFC capabilities this year. Moreover, IFC will generate $37 billion in cumulative revenue by 2027, the consultants said as part of unveiling the latest, sixth edition of its Aeronautical Satcom Market report. NSR.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.