Satcom in 2019: Leasing vs. services and the year ahead

NSR Bottom Line article was carried in SatelliteProMe.com Read More

NSR Bottom Line article was carried in SatelliteProMe.com Read More

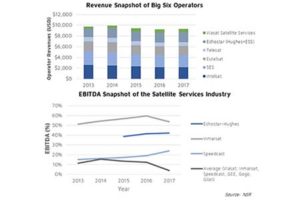

2018 emerged as an understatement compared to the hype generated by satellite operators. Revenue didn’t rebound according to expectations, pricing and backlog both declined across operators, and video finally showed no signs of further growth, as multiple operators posted revenue declines in video even with marginally increasing demand. Looking downstream, suffice it to say that.

Recent (Q2 or Q3) financial results have been a mixed bag for the industry. Video revenues have consistently declined on a YoY basis for most operators including Intelsat, Eutelsat, SES and EchoStar Satellite Services, while most operators have posted gains in network connectivity – most prominently in Government and mobile connectivity verticals, including ViaSat. To.

The traditional satcom industry can be argued to be entering its third transition phase, after the FSS video boom until 2010 and the HTS influenced pricing decline more recently. With languishing growth in 2018, alongside declining EBITDA margins and backlog, the operator industry remains uncertain on video, while debating on the merits of going fully.

C-band reallocation debates between satellite operators and telecom providers aren’t new. Mid C-band spectrum is seemingly ideal for low frequency applications and resistant to rain fade, with recent 5G technology promoters terming the 3.7-4.2 GHz spectrum as a sweet spot. This part of C-band traditionally has fallen under the purview of the larger 3.4-4.2 GHz.