Turning the Satellite Business Model Upside-Down

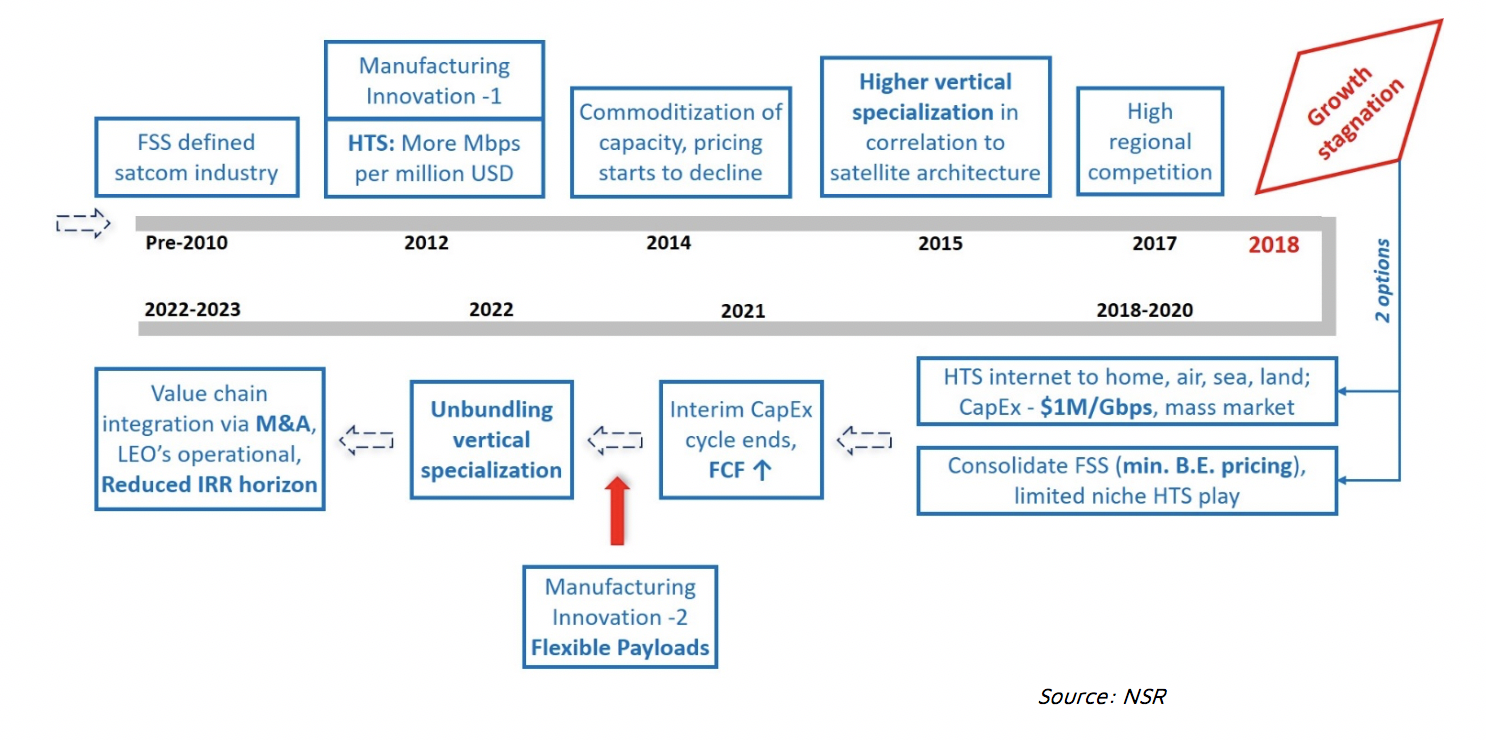

The traditional satcom industry can be argued to be entering its third transition phase, after the FSS video boom until 2010 and the HTS influenced pricing decline more recently. With languishing growth in 2018, alongside declining EBITDA margins and backlog, the operator industry remains uncertain on video, while debating on the merits of going fully downstream in the long term. Several factors such as high regional competition, video demand absorption through higher compression, supply-demand mismatch impact on pricing, pressure from OTT, and commoditization of capacity have driven the market to a stagnation point. However, no trend is bigger than the continuous manufacturing innovation to pack more Mbps per unit of million dollars cost. By pushing CAPEX per Gbps to ever more efficient levels, operators are able to undercut competitors on lease pricing, forcing many to sell at or below break-even profit margins, creating a zero-sum effect overall.

Industry’s 3rd Transition

While, indeed, the innovation looks promising to take the satellite industry more mass market in the longer term, this transition has brought into the limelight two clear strategies that operators look to execute:

- Give Broadband to All – direct to home, via backhaul for village Wi-Fi, to air, sea and land mobility. Go mass market through service offerings, with extreme efficiencies both on capacity and modem/antenna

- Consolidate FSS via regional market positioning, increase margins, enter a limited HTS play specializing towards a vertical

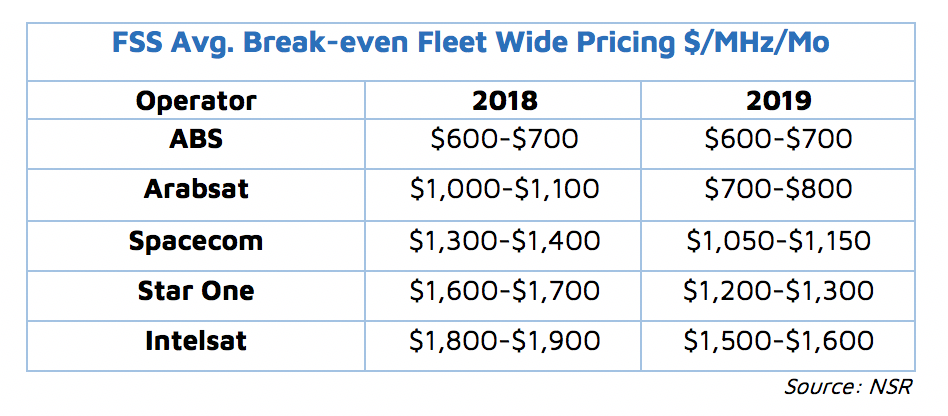

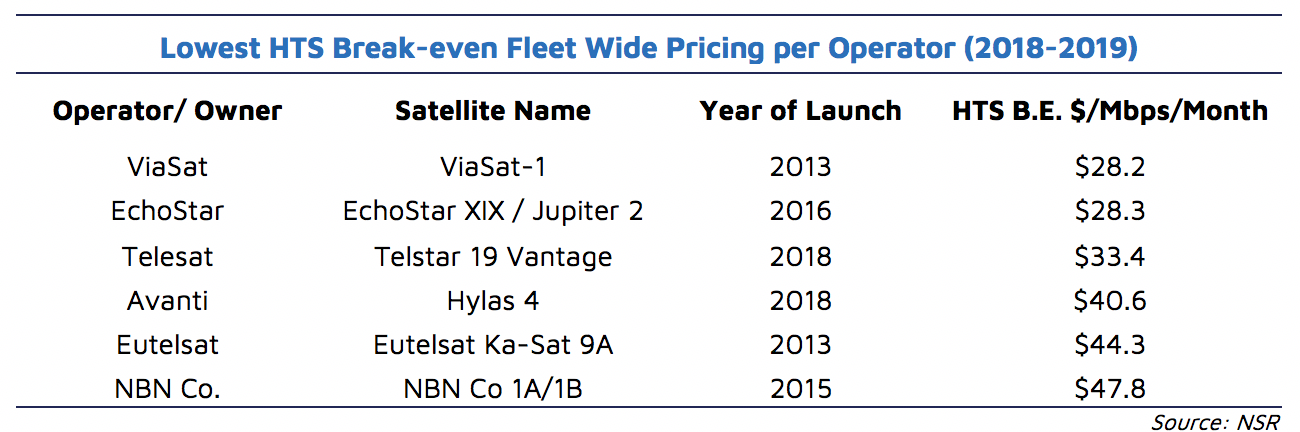

At the heart of these strategies is the relative competitiveness of each player, where irrespective of the service offering, an ability to bottom out capacity pricing (at >15% IRR) remains key. This is achieved by having the lowest Break-even fleet wide pricing* (pricing at zero profit margin) in both FSS and HTS fleets – essentially packing more Gbps at the same cost, alongside reduced launch costs.

This constant decline of CAPEX cost has a significant rollover effect on the entire ecosystem, as older fleets can’t cope with pricing pressure from new/efficient fleets, consequently reducing planned 15-year IRR margins. This, in turn, reduces cash on hand for longer term replenishment, creating higher Net debt to EBITDA than anticipated and an indecisive 15-year outlook on pricing stability. Metaphorically, this is a circle of doom that many operators may not escape in the long term, even as service offerings stabilize the market in the short to medium term.

In addition, with supply exceeding 4-5x times that of demand in 2027 (in combination with potential LEO constellations), another race to the bottom for pricing is expected to ensue, rendering several individual satellite assets to under-perform. With C-band already affected, fixed data and video distribution applications look most stressed in the medium term, while pricing for backhaul and consumer verticals declines at low double-digits in a bid to go mass market.

Thus, as a must pivot, NSR believes the satcom industry will witness a renewed fleet innovation and business strategy to match CAPEX spend with long term sustainability. The Break-even metric indicates the risk of betting on a fixed vertical/geography for 15 years, when in the next 5 years – CAPEX per Gbps thresholds can be broken again, rendering the satellite asset toxic. Thus, as the CAPEX cycle ends between 2019-2021 for most operators, and free cash flow (FCF) increases, both HTS mass market and FSS consolidation strategy options will be on the table. But more importantly, operators will need to consider launching flexible payloads catering to most demand verticals and changing beams, frequencies, distribution channels and VAS on the go. Consequently, consolidation becomes key to succeed in such a strategy.

Secondly, reliance on high fill rates, 18% IRR margin, >75% EBITDA margin and 10% ROCE will shift to strategizing high ARPU, plug and play distribution partnerships and cross-vertical selling between operators or service providers. This divergence from a pure play lease model to a network and vertical agnostic user-oriented play can flip the 15-year satellite business plan as we witness today.

Bottom Line

From higher vertical specialization to unbundling, from pure play lease to bundling network, content and entertainment services and from commoditization to mass market flexibility – the industry is witnessing a key change: accurate prediction of IRR over a 15-year horizon is impossible. Under-performing assets are a liability in space due to tighter replenishment cycles, and without innovation towards fleet flexibility, capital investment in this industry could become riskier. Beam flexibility and a network + application agnostic platform demands plug and play distribution channels, that in turn force partnerships into mergers in the long term – producing clear winners and losers. Coupled with a shorter IRR horizon, the traditional satcom business model is surely transforming.

*Break-even pricing is a proprietary NSR metric introduced in Satellite Industry Financial Analysis, 8th Edition, that ties in the entire value chain of the industry – from the effectiveness towards manufacturing and launch cost, SG&A in a business model of selling MHz, operator’s cost of finance and impact towards 15-year IRR, and eventually business model of selling Mbps through inclusion of ground system costs. Representative of zero-profit margin, Break-even pricing is calculated in terms of $/MHz/Month or $/Mbps/Month. This metric enables an industry entrant (per geography or application) to analyze the toughest possible competition in the short-to-medium term, and the consequent measures needed to reduce the cost for pricing lower than the competitor. The metric provides a unique way to future-proof the satellite operator business.