C-band Spectrum Reallocation: Too Lucrative to Ignore?

C-band reallocation debates between satellite operators and telecom providers aren’t new. Mid C-band spectrum is seemingly ideal for low frequency applications and resistant to rain fade, with recent 5G technology promoters terming the 3.7-4.2 GHz spectrum as a sweet spot. This part of C-band traditionally has fallen under the purview of the larger 3.4-4.2 GHz band licensed by ITU for Fixed Satellite Services (space to earth), radio and mobile links through satellite and other such services worldwide. While various countries have already implemented several measures to either purchase or forcefully take the band from satellite operators and auction off to telecom operators, the case in U.S. has been more uncertain until last year.

Satellite Demand Play

The majority rights holders to 3.7-4.2 GHz of spectrum in the U.S. are Intelsat and SES, two major, global satellite operators in terms of in-orbit satellites and transponders leased. They account for almost ~90% of the U.S. C-band spectrum and service various cable customers across the U.S. for video distribution. However, with spectrum rights expected to expire in mid 2020s and YoY performance on the C-band U.S. business declining fast (owing to capacity pricing declines and OTT pressure), revenues associated with C-band spectrum do not make economic sense (-6% CAGR in 10 years) in the future as demonstrated in the NSR’s GSCSD 15th Edition report.

Satellite Revenues vs. Spectrum Proceeds?

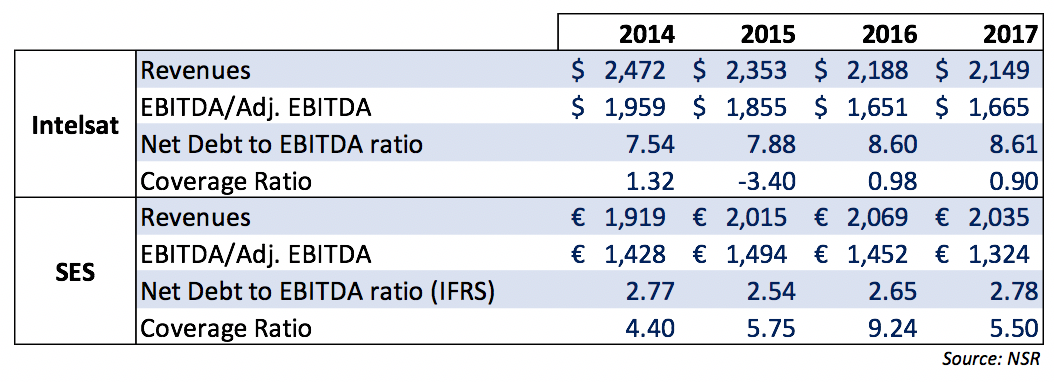

Similarly, telecom industry proponents have increasingly demanded the FCC in the U.S. to free up 500 MHz of spectrum for 5G use. Thus, already laden with high debt, Intelsat (Net debt to Adj. EBITDA ratio of 8.61) teamed up with Intel in October 2017 to submit a win-win proposal to reallocate 100 MHz of this spectrum towards 5G, in a span of 2-3 years, while reallocating multiple TV channels to other/new satellites. Recent developments have seen SES, and until recently Eutelsat and Telesat join the proposal, now termed as C-band Alliance. The proposal aims to remove C-band footprint from major U.S. metropolitan areas where the first deployment of 5G would take place, in-turn compensating cable head-ends for a required change in filters and ground equipment (antennas, repointing), amounting to a total cost of roughly ~$900M, taking into account a registered 4,700+ Earth Stations in the U.S., and approximately ~30,000 more unlicensed ones.

Now, even with declining pricing and consequent declining revenues, and high reimbursements towards broadcasters/cable operators along with a years-long painstaking process of dissecting the spectrum, the proposal makes sense due to the high arbitration reward available with the auction of the 100 MHz to 500 MHz of spectrum. Following similar spectrum sales of 600 MHz in other countries and bands in the U.S., a 2x-4x higher MHz-pop value (Kerrisdale) could be allocated to the total 500 MHz spectrum sale in question. Thus, with other countries establishing a $0.17-$0.38 MHz-pop spectrum sale rate, the U.S. valuation could easily be $0.5-$0.6 conservatively, and with the need of a guard band for removing the interferences (of ~50-100 MHz), the total value of the 400 MHz spectrum for 330 million U.S. population could theoretically be $60-$75 billion. And with Intelsat and SES, approximately possessing 45% of the spectrum each, both could (again, theoretically) net at least $20-$25 billion in proceeds after tax.

Constraining Economic Factors

However, this massive valuation of proceeds should be interpreted with caution. Several more economic factors are at play, as follows:

- Costs would certainly be higher than the reimbursements to broadcasters/cable providers, given both Intelsat and SES may need to launch a new satellite (<$200M) to retain customers. However, with the new compression HEVC using DVB-S2X, almost all video distribution channels could fit in under 30% of Ku-band satellite capacity.

- There would be a certain loss of capacity revenue per year, in situations where customers don’t decide to switch to other satellites of the same operator.

- Change in necessities on guard band allocation, as the mid C-band spectrum is very sensitive to interference.

- Change in economic value for the sale of the first 100 MHz of spectrum as compared to the last 100 MHz, and the demand profile in low frequency changes and subsequently the bargaining power of the operators reduces on ‘usage definition’ as most customers are moved to Ku-bands.

- Finally, the FCC could resort to partial allocation of spectrum assets from satellite operators to telecom ones, while forcefully auctioning the other part once the rights expire in the next ~6-8 years.

- Moreover, with the current U.S. regime, satellite operators may only be partially allowed to take the proceeds to their domicile countries or forced to invest the proceeds in U.S. markets.

What Happens Outside of the U.S.?

With respect to other regions around the world, there is precedent with many operators in Asia having to relinquish rights in extended C-band already, where many hadn’t been compensated appropriately. Most underdeveloped countries do not pursue fairness to spectrum rights as the U.S. FCC does, and with lack of procedural conformity and weak(er) historical precedence of receiving proceeds through sale of spectrum, it is unpredictable that operators in Asian or even Latin American/Middle East countries may get a fair share from a similar auction. Europe, in all likelihood, could have the same ramifications as the U.S., albeit with a 1.5.x-2.5x lower MHz-pop valuation as compared to U.S., which makes sense for Eutelsat to join the alliance.

Bottom Line

Economic and regulatory factors such as above lower the high arbitrage potential with an overlay of operational, CAPEX and regulatory costs, but nevertheless Intelsat and SES have a great opportunity to offset their complete debts with the spectrum sale. Even with SES’s maximum 200 MHz spectrum sale possibility, the costs and regulatory factors, Intelsat and SES each may gain between mid to high single-digit billion dollars (considering Intelsat’s >6B tax losses), wiping of 70%-100% of their debt.

Faced with net losses in C-band satellite video distribution and data due to extremely low fleet efficiencies (as reported in NSR’s SIFA 8th Edition), a limited mid C-band spectrum sale remains to be the best bet for these operators clearing debts and investing in new hybrid satellite architectures, constellations and consumer broadband.

Although, even with successful spectrum sale precedents in U.S. before, the proceeds and their subsequent transfer to Luxembourg domiciled SES/Intelsat would remain in question, primarily due to the current U.S. administration’s aversion on such an outflow. Even if the proceeds are allowed from escrow (auction funds), notwithstanding the years it can take in clearing up total spectrum, operators may be forced to invest in an already saturated U.S. market, that would inherently be loss making, thus reducing the ultimate cash benefit available to both operators. Finally, the share price surge may be less substantiated in the long term, if due to the above factors, only a fraction of proceeds materialize into direct cash opportunity.