5G IoT – a Breakthrough for Satellite/MNO Integration

Satellite IoT has for years been a niche market compared to the overall M2M and IoT market and something that hasn’t been too seriously considered by mobile network operators (MNOs) to date. Although there has been desire for “dual-mode” services that can connect to terrestrial networks and satellite networks, this has traditionally added great complexity, higher terminal pricing and more complicated billing arrangements. Consequently, there has been limited uptake of this kind of usage. However, this is about to change.

The 3GPP Release 17 was established in early 2022, and its inclusion of non-terrestrial networks (NTN) will change the future of satellite technologies. This is due to the standard allowing terrestrial IoT devices to connect to satellites, greatly removing the friction needed to form agreements between MNO/MVNOs and satellite operators. Therefore, relatively straightforward roaming agreements, like those that MNOs have had in place for decades, will be extended to satellite service providers, along with all the benefits, and revenue, which that provides.

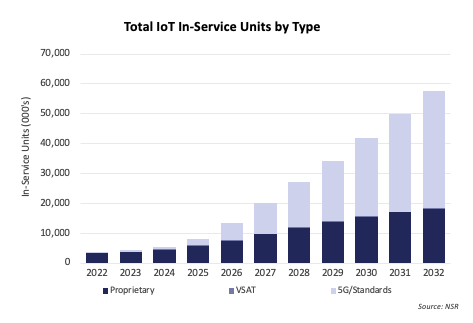

With this in mind, in NSR’s recently released M2M and IoT via Satellite, 14th Edition, it was found that by 2032, 68% of 57.7 million in-service satellite IoT units will be connected via 5G or other standards-based protocols (including LoRa), up from almost nothing at 2022-year end.

However, it will take some time for sales and usage to ramp up. While roaming agreements are straightforward and ready, compatible devices are not. It will only be once the chipset manufacturers implement the standard into their future designs that this will unlock a huge new addressable market. With this not expected to occur in any scale until 2026, there is time for MNOs to start looking into agreements with satellite operators. Work will need to be done now to ensure that current terrestrial IoT end users will have a seamless experience as possible with this newfound satellite roaming capability.

This will involve MNOs laying the technical groundwork to ensure data flow is efficient in a high latency and bandwidth constrained satellite environment. This includes greater deployment and optimisation of edge computing resources. While most customers won’t have any need for satellite connectivity, those with mobile assets which are outside of terrestrial range for 1-5% of the time, will often gain an order of magnitude greater value by closing the connectivity gap.

However, despite the huge new opportunity that this provides, there is still more work to do be done on standards-based satellite IoT. Concerns have been raised by IoT operators that handover between 5G networks is less efficient, resulting in potential capacity issues on the satellite side. Proprietary solutions and legacy MSS M2M services still have their place, so 5G IoT will be best suited to end users who regularly move in and out of terrestrial network coverage.

The Bottom Line

5G IoT services, both over traditional MSS operators and newer IoT-dedicated small-satellite operators, will provide the potential for huge new revenue opportunities across the IoT value chain. However, for MNOs to capture this opportunity, they will need to work with satellite operators to obtain the right technical expertise ahead of time before establishing roaming agreements. While it may be tempting to not bother with the integration effort and focus on terrestrial only for now, there will come a time when an IoT device feels “broken” if it can’t connect to satellite out of terrestrial range, much like with the iPhone 14 range today.