New EO sensors: expanding the pie or stealing the slice?

The industry has witnessed a recent surge in investment in a new class of Earth Observation (EO) sensors such as thermal infrared (TIR), hyperspectral, radio frequency (RF) monitoring and greenhouse gases emissions monitoring. These recent investments demonstrate an excitement for new datasets, for new use cases, and different ways to address the current market. However, whenever something new is introduced, stakeholders often struggle to determine if the result will be market expansion or replacement. Will it expand the pie or take a slice out of it?

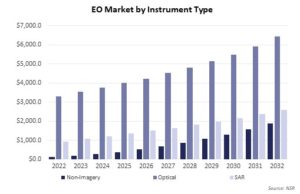

NSR’s Satellite-based Earth Observation, 15th Edition report forecasts that the non-imagery segment, which consists of these emerging sensor types, is growing at a CAGR of 31.5%, indicating an increasing market opportunity with a growing addressable market. Overall, non-imagery will generate $8.7 billion in cumulative revenues by the next decade, which is 11% of the $78.5 Billion global EO market cumulative revenues.

New sensors expanding use-cases

Hyperspectral imaging boasts diverse applications in agriculture, environmental monitoring, and weather forecasting, with the potential to replace some current use of optical sensors, due to a greater number of bands that generate more information. Similarly, Thermal Infrared (TIR) sensors with higher resolution and accuracy are enhancing the capability to detect wildfire monitoring, industrial tracking, and emergency response. Companies such as GHGSat and Kayrros are offering solutions targeting climate change, which is currently a major driver for EO adoption.

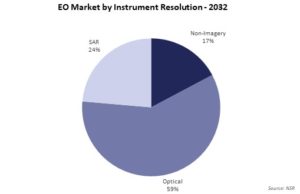

As a result of these changes, the non-imagery data sources are expected to take a 17% overall EO market share by 2032, from a mere 3% in 2022.

Adoption of new datasets depends on both the expertise to use the said data, and the customers’ awareness as to its value, specific to each market vertical. Pricing also plays a crucial role to choose between satellite and ground-based systems, with factors like timelines, analytics, and costs already influencing early-adopter budget decisions from governmental and military entities.

Governments leading the charge

Government & military are the primary market drivers here, with NSR forecasting $742.3 million in cumulative revenues over the decade for the former, and $1.2 billion for the latter. To provide better market access and harness these revenues, providers need closer collaboration with customers, through initiatives such as the Early Access Programs (EAPs) which improves customer awareness, provides tailored solutions based on end-user requirements, and results in easier adoption once satellites are launched. Early-stage companies who have launch plans in the short-term, such as Satellite Vu, Pixxel, HyperSat, and Orbital Sidekick, are already engaging with customers through EAPs.

The Earth Observation market, despite facing adoption inertia and long revenue realization timelines, is at a tipping point for increased adoption. The commoditization of datasets, including optical and SAR imagery, is yet to be achieved, and the nascent non-imagery market adds complexity. Market expansion depends on overcoming these challenges by satellite operators and providers. Despite hurdles, rapid growth is expected in the next decade, with non-imagery market share projected to rise ten-fold, from $55 million in 2022 to $526 million in 2032 due to increased addressability.

The Bottom Line

So, are these new satellite sensors expanding the pie or stealing the slice in the EO industry? The answer lies within the ability of these new sensors to complement existing technologies. In certain use-cases, they may replace traditional satellite imagery where value-add versus pricing will play a pivotal role in adoption.

In addition, the ability to complement existing technologies will further determine the level of integration into existing ecosystems. However, these new sensors are mainly expanding the EO pie by tapping into new budgets allocated by government customers and users or replacing ground-based systems where cost optimization or cost benefit is key by utilizing satellite imagery, instead of traditional ground-based systems. However, while new datasets may be expanding the pie, providers need to collaborate closely with potential customers to be able to benefit from any market expansion.