5G Satellite-to-Device Connectivity

Direct satellite connectivity to Mobile, at affordable prices, has been one of the moonshot objectives of the industry for many years. Leveraging the advances in 5G, multiple projects are pursuing this vision, attracting huge levels of interest in its way (AST & Science going public through a SPAC valuing the company at $1.8B). But what are the opportunities and limitations of adopting Mobile standards for Satellite communications?

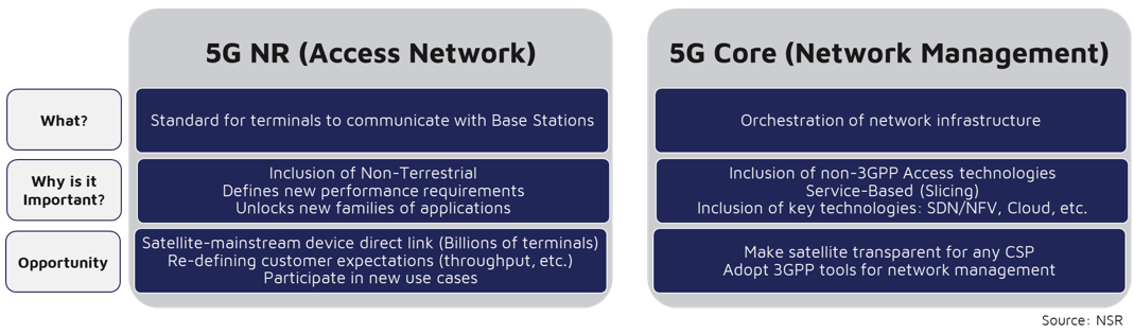

One of the most relevant elements of the 5G NR access network standard is its adaptation to allow direct connectivity from devices to Non-Terrestrial Networks. This has a truly transformative potential for the Satellite industry. In fact, NSR’s 5G via Satellite report forecasts the largest number of units to be connected over Satellite to come from this new capability.

Opening a Vast Addressable Market

The fact that the same off-the-shelf device that connects to a terrestrial station will be able to close the link with a satellite is no minor feat. This instantly opens the door for Satellite to go mainstream and leverage the mass-market production and the distribution ecosystems.

The good news is that major chipset manufacturers are embracing this opportunity, and the race to adapt their products and influence the standards yields promising technology demonstrations (MediaTek-Inmarsat). Using standardized chipsets and leveraging the scale of mainstream devices production will obviously drastically cut equipment prices.

The capability to communicate with mainstream devices means a paradigm shift in the definition of the addressable market. A standard device that is located outside of the terrestrial coverage (be it an IoT device in a mobile platform, or an end-user going on a weekend trek) could potentially roam to the satellite network. In the same line, this opens global scale distribution channels with satellite operators acting as wholesale providers for MNOs that want to offer truly ubiquitous coverage.

Total Cost of Ownership and Performance for Various Satellite Use Cases

Performance levels might vary when roaming to a satellite network. Satellites can obviously not support the user density of terrestrial networks, and power and link budgets will be very different with orbiting Base Stations. But for use cases where the terminal and the subscriber acquisition cost (SAC) are the primary drivers of the Total Cost of Ownership (TCO) (Narrowband IoT, consumer handhelds, etc.), optimizing the equipment cost and opening mainstream sales channels makes a lot of sense.

However, for Broadband use cases, the advantages might not be so clear. The lower cost of the terminal and SAC will not be enough to compensate the losses on the radio interface compared with satellite-specific waveforms (DVB-S2X) and architectures (FSS Bands). In a Consumer Broadband terminal (300-350 USD), using a standard 5G chipset might generate savings of ~5% (other components like BUCs, LNBs, IDU, etc. make up the bulk of the cost), which is not enough to justify the transition. The analysis is even more extreme for high-throughput sites (Backhaul, Aeronautical, Maritime, etc.), where the cost of the terminal is a minor contributor to TCO.

Bottom Line

Direct satellite connectivity to mainstream devices is possible, and the entire ecosystem (terrestrially-focused chipset vendors, satellite operators, startups, standardization bodies, etc.) is working hard to adapt 5G NR to Non-Terrestrial Networks.

This will unlock extraordinary opportunities for the satellite industry. Opening access to cheap mainstream devices, changing the definition of the addressable market (now counted in Billions), and access to global scale distribution will change the paradigm for Narrowband applications (IoT, Consumer Handheld, etc.).

There are some limitations, especially for Broadband use cases, where bandwidth inefficiencies heavily penalize TCO. Satellite-specific waveforms will still be dominant in high throughput applications (Trunking, Consumer Broadband, etc.), where satellite will cover the middle-mile of the network and the last-mile can still be deployed with Mobile-specific access technologies (5G, Wi-Fi, etc.).

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.