A 1st-Order Solution: More Broadband Maritime Vessels

The Maritime Satellite Communications market is at a crossroad; more capacity is available in all frequencies and orbits thanks to Iridium’s recently launched Certus plans, VSAT terminals are getting lighter and cheaper, and end-users continue to find value in some flavor of higher throughput connectivity. Unlike Aeronautical Markets that struggle with complex business plans, the Maritime sector is very much in the ‘connect-it’ mode.

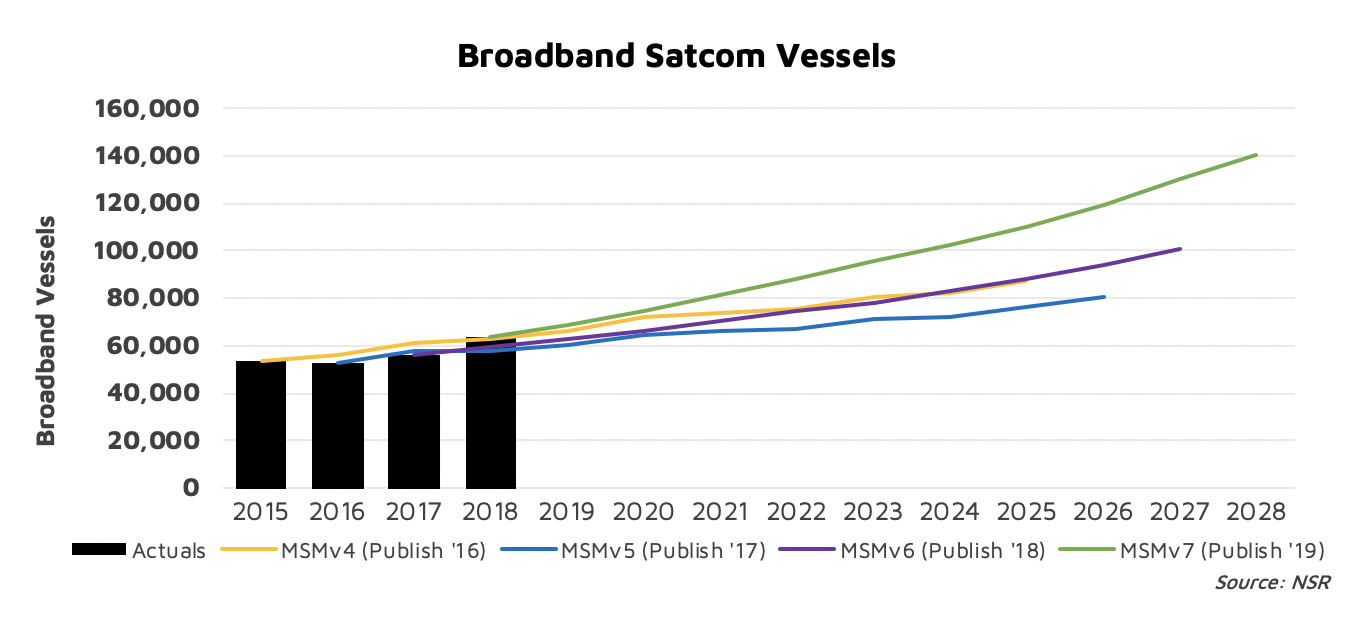

As NSR explores in Maritime Satcom Markets, 7th Edition, Maritime vessels are adopting broadband satellite services at an ever-increasing rate. From 2017 to 2018 over 7,700 vessels adopted some flavor of VSAT or MSS Broadband connectivity – nearly double the rate from 2016 to 2017. By 2028, NSR’s latest projections place the market at over 140,000 vessels with broadband connectivity, more than half of which will be VSAT. So, the simple question is: What’s Changed in a Year?

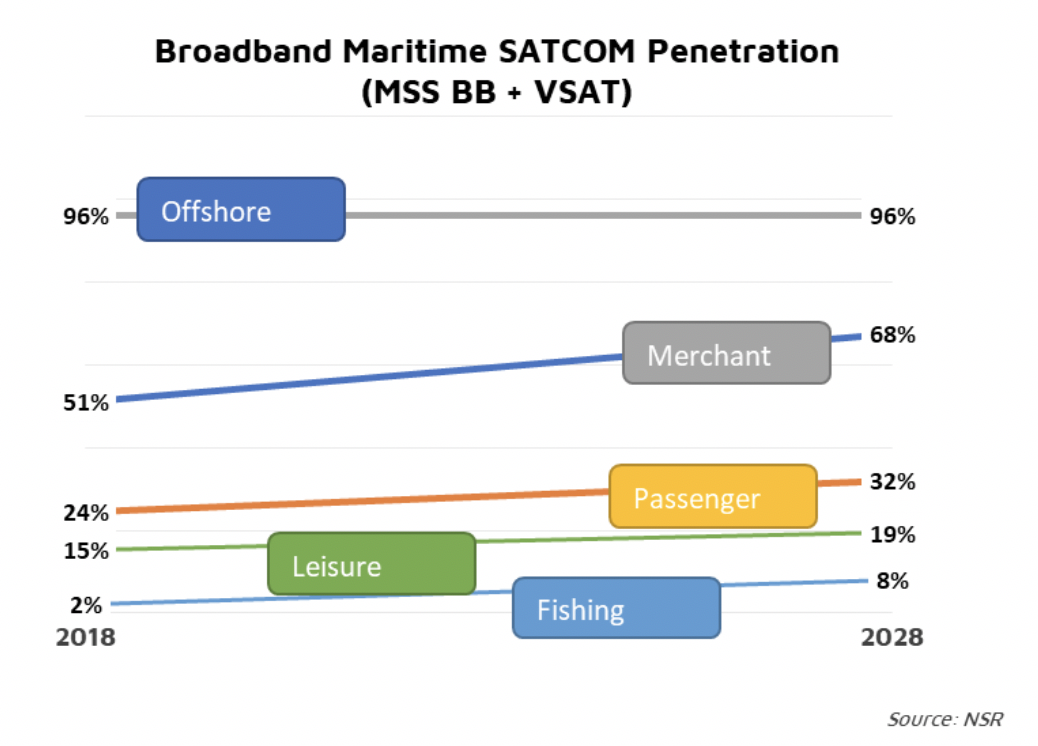

Going down the markets of Merchant, Offshore, Passenger, Fishing, and Leisure, they all show signs of expanding at the bottom ends of their addressable segments. Cheaper VSAT terminals sit alongside more MSS services pushing into Broadband (thanks Iridium), helping to push down some of the CAPEX-sensitive sides of the market as both enable lower up-front costs and greater access to broadband services. Lower capacity prices for VSAT (and greater competition in MSS Broadband) are keeping recurring costs under control. Overall, the greater ‘need for connectivity’ has finally centered around a common goal of greater broadband penetration for the Maritime sector.

For ‘business applications’, Merchant customers are adopting more and more digital services either by choice or by force via regulatory reforms. Offshore has always been well connected – and a slightly improved outlook towards 2028 means new opportunities. Leisure and fishing are both in a growth phase – better/cheaper/lighter terminals for VSAT and MSS, combined with lower cost connectivity plans boost the lower end of the market, aka ‘growing the pie’. Passenger growth continues, both from new-builds in the ocean and river cruise segments as well as ferries adopting broadband services for the first time. Across all the major Maritime segments, there are plenty of places for a range of low/medium/high-end customers and solutions.

Quite simply, a perfect storm of cheap(er) terminals and cheap(er) capacity is opening up the addressable Maritime markets. For service providers, efforts should be focused on increasing access to terminals, gaining more installation capabilities, and securing access to additional capacity – in all orbits and frequencies. Ocean Cruise is a niche play for the biggest of players, Offshore has challenges. Fishing and Leisure have a range of low/med/high and a highly fragmented service provider landscape – while facing an increasing demand for connectivity. Merchant is where the vessels are to be connected, with more than half of the broadband vessels throughout the forecast. All said, the future looks bright for a 1st order solution – connect more vessels to broadband services.

Bottom Line

For most of the Maritime Satcom Market, the business is on getting the first broadband connection – not building “Awesome Guest Wi-Fi”*. Monetization schemes, revenue-shares and other services being explored in the IFC sector are almost another world away for most Maritime customers. Instead, Maritime customers* are looking at getting lighter terminals to reduce installation expenses, better throughput per dollar, and only starting on the pathway to “Awesome Onboard experiences.”

*Unless you are an Ocean Cruise customer – Stay tuned for NSR’s Next Maritime Bottom Line where we focus on the over 800 Gbps of Capacity Demand Passenger Maritime will require by 2028 to build “Awesome Guest Wi-Fi”.