A Regional Shift in the Cruise Market Ahead?

While the major cruise lines in North America announce another round of departure delays, some regions and operators are already resuming services. This week, Norwegian operator Hurtigruten resumed its costal cruise services. In the next couple of weeks, depending on health conditions, three more ships will return to passenger cruise service. While Hurtigruten ‘technically’ never stopped sailing as a ferry service – these are some of, if not the first, cruises to resume services. Later this week, American Cruise Lines will restart river-focused services in the Pacific Northwest. And, other cruise lines are still slated to resume some type of limited services before the end of the year.

What does all this mean for Satellite Connectivity for Passenger Maritime Services? NSR’s Maritime SATCOM Markets, 8th Edition dived into this topic back in May – and, just as we saw in the early days of widespread cancellations – the near-term market looks different:1, A Shift Towards River Cruises; and 2, More “Out and Back” Itineraries.

1. A Shift Towards River Cruises

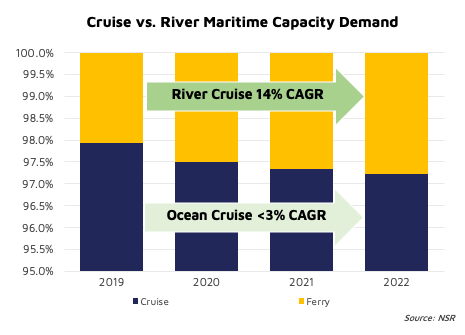

While Cruise Markets will still comprise 95%+ of overall SATCOM Demand through 2022, River Cruise Capacity Demand is growing significantly faster over the next couple of years compared to Ocean Cruises. With both segments operating at 50% capacity, slowly phasing in higher capacity rates based on health conditions, the real shift is an opening of new routes and markets such as the Missouri River in the United States.

For the U.S. as an example, states are introducing different travel/quarantine practices as the summer vacation season starts – all complicating river cruise operator plans. Until widespread restrictions are lifted (and passenger density increases), what were a couple of hot spots around the world will likely be better distributed demand for river cruise maritime connectivity.

2. More “Out and Back” Itineraries

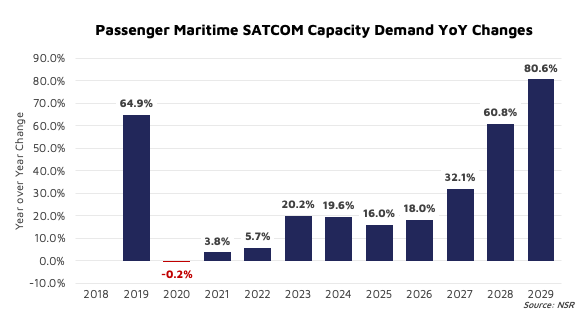

Where once ‘double-digit’ year over year growth was commonplace from 2018 to 2019, 2019 to 2020 saw a shift in demand growth as vessels were re-tasked for crew repatriation missions. Looking across 2020 and into 2021, the ‘ocean going’ ships are likely to go into international waters to enable the full range of onboard amenities. However, they are unlikely to enter foreign ports. While these ships may visit a few ports along a countries’ coast, that too is still up in the air.

Topline demand looks mostly flat, geographic shifts ahead. Meaning, Satellite Operators and Service Providers with access to well dispersed capacity footprints might gain a slight upper-hand as the market works towards ‘right-sizing’ itself.

So – it seems that the passenger market is working towards safely returning to service, and that structurally vessel positions and routes will look a little different than last year (if for no other reason than a staggered return to service plan is skewing the ‘active vessel’ distribution.) What is the “Big Unknown”?

The “Big Unknown” Remains Per-Passenger Demand. More than just vessel capacity, will passengers require/demand more connectivity while afloat? Does it increase by 50%? Maybe more? Given long-term, minimum contractual commitments between Service Providers and End-users, once vessels return to service how likely is it that these vessels will resume their ‘minimum CIR’ rates if for no other reason that they are contractually obligated? With all the work/learn/socialize from home activities that people have adopted in the past few months, it seems unlikely that demand is the same or less.

Bottom Line

Vessels are likely to spend more time at-sea, meaning people will probably spend more time aboard… and have fewer terrestrial roaming options. River cruises continue to expand into new routes, and coastal cruises will be highly dependent on the health situation on the ground. While there might be a staggered introduction of vessels over the next couple of months, Bottom line, while the market is shaping up to be more geographically distributed demand remains.