Are small GEOs the answer to L-band Maritime Economics?

The L-band services are the cornerstone of maritime safety systems. Recent disruptions in the Asia-Pacific region, leaving L-band users without connectivity and safety systems, reminded the industry of its importance – and of the vulnerabilities. Despite the C/Ku/Ka-bands growing in demand due to their higher connectivity speeds L-band still provides critical services to maritime end-users. Satellite operators must balance the legal obligations of safety services against the commercial economics of L-band. Small GEOs are a novel solution to increase service resiliency in a low-growth market opportunity.

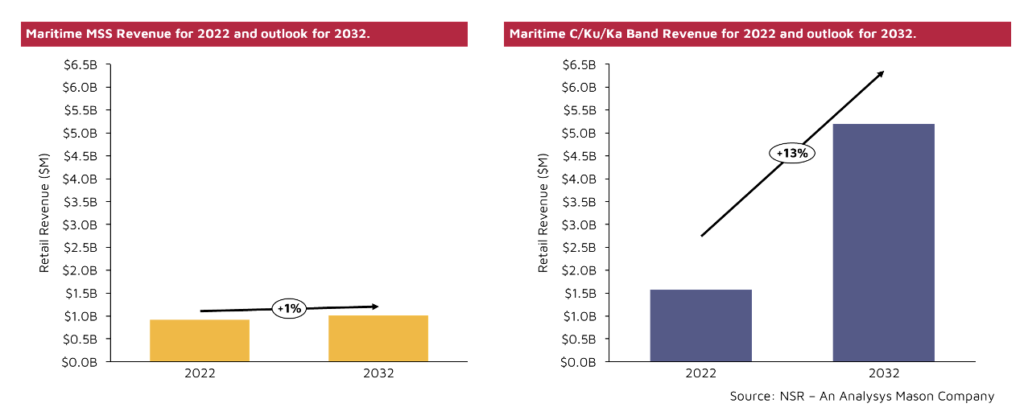

A Low-Growth Outlook for Maritime L-band Services:

NSR’s Maritime Connectivity Report, 11th Edition predicts a 1% CAGR in retail revenues for Mobile Satellite Services (MSS) which is built on L-band. MSS provides an indispensable service to mariners such as critical and regulated safety of life connectivity, out-of-band backup for higher speed C/Ku/Ka services, and other dedicated use-cases such as IoT or vessel tracking. Despite the usually higher recurring monthly cost associated L-band, it remains a dependable, stable connectivity option on which the maritime industry still heavily relies on.

The recent suspension of services from Inmarsat L-band I-4 F1 satellite caused major disruption for the Asia-Pacific region. This most recent event highlighted the need for resilient and robust L-band services. To address these concerns, Inmarsat has invested in three I-8 satellites, all being small GEO satellites manufactured by Swissto12. As NSR stated 4 years ago, small GEOs can provide a cost-effective solution with reduced CAPEX risk for niche markets and use-case such as L-band. These new and innovative approaches are required going into the future – satellite operators must have a robust and diverse investment strategy which balances time-to-market, technical risks, and service obligations to end-users and other stakeholders.

Is Small GEO the future of L-band services?

Inmarsat joins Intelsat’s IS-45 in using these small GEO platforms for providing mobility services from Swissto12. Even though L-band is not the lucrative option it once was, it remains widely used in maritime, aero, and other mobility markets. Additionally, the inclusion by Inmarsat of PNT-augmentation capability through their Satellite-Based Augmentation System (SBAS) on these I-8 satellites can provide additional resiliency and monetization opportunities such as a nearly $190M award to Inmarsat from Australia and New Zealand for SouthPAN services. This announcement by Inmarsat to use small GEOs will ensure L-band availability and reliability into the future.

Investing in a GEO satellite can be costly and unfavorable for satellite operators. Small GEOs can meet CAPEX budgets as they are less expensive to produce. They can address the lack of capacity or network resiliency faster than standard GEO satellites as their construction lead time is shorter. Satellite operators opting for small GEOs can limit CAPEX and can witness cost savings in both production and launch, compared to traditional GEO satellites. For maritime applications, L-band remains crucial for safety and is expected to remain so into the future. In an era of constrained CAPEX budgets, NSR expects to see more announcements that use novel on-orbit approaches to service high-availability services such as PNT-augmentation and maritime safety.

The Bottom Line

L-band provides a dependable and resilient safety service which is essential to the maritime industry. Even though L-band connectivity revenue will not drive revenue growth in the maritime market, it remains an essential service. The recent disruptions in the Asia-Pacific region are a reminder that it is crucial to have redundancy for L-band. Small GEOs offer satellite operators an affordable approach to address demand in niche markets, and ultimately enhance service resiliency.