Are Small GEOs the “Next Big Thing”?

If there is something certain in the current satcom market, it’s that Video is stagnating, and Data is the future growth driver. However, many satellite operators are still cautious adopting HTS. The options are more varied than ever and there isn’t a clear “dominant design” for satellite operators to adhere to when planning their HTS payloads. Given the lower CAPEX and lower risks involved, are Small GEO payloads one viable option for capacity deployment in strategic markets and applications? Judging from early announcements and industry interest, the answer may be “yes”.

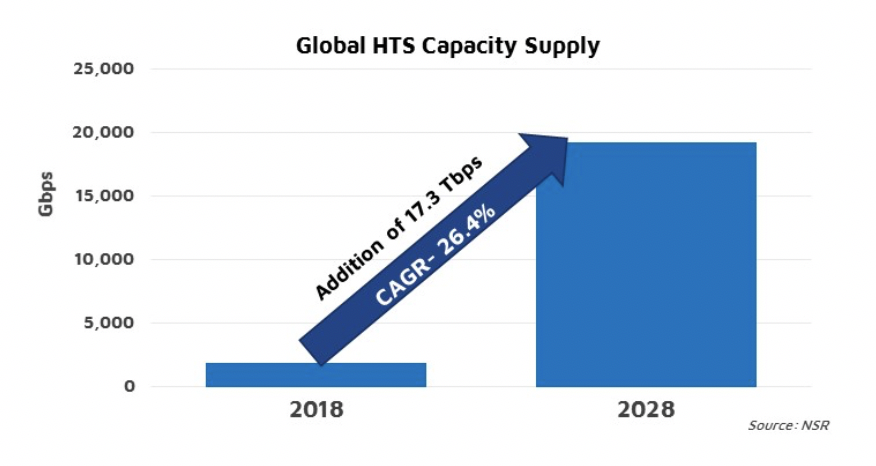

With HTS going mainstream and a bigger number of satellite operators announcing plans to incorporate HTS to their fleets, capacity supply will skyrocket in the coming years. According to NSR’s Global Satellite Capacity Supply and Demand, 16th Edition report, GEO-HTS capacity supply will climb at 26.4% CAGR in the next 10 years, approaching 20 Tbps by 2028. It would be very easy for the industry to fall in the oversupply trap: scale does offer advantages in metrics like cost/Gbps of supply, and the market is generally dispersed with some regions hosting up to 9 actors with market share upwards of 5%, all these not forgetting the national interests preventing M&As. Furthermore, some satellite operators do not feel comfortable with data-driven business models as they require a much higher engagement in demand stimulation. In this context, Small GEOs can be an interesting alternative, offering operators the option to adopt HTS in a more focused way, serving only their core markets and putting lower CAPEX at risk.

Finding the Right Balance

In the current market scenario, satellite operators are in front of one of the most challenging times for fleet planning. Finding the right balance between growth, technology evolution and legacy markets is not straightforward. While Video will show scarce opportunities for growth, cumulative revenues are still large. On the contrary, Data drives extraordinary growth but requires significant investments and a transformation of business models. This creates diverging supply strategies for different satellite operators.

While some operators invest in large VHTS payloads to minimize CAPEX/Mbps hoping to activate elasticities and fill the satellites rapidly, other operators with a greater exposure to FSS try to balance profitable legacy customers like Video with growth coming from Data launching Hybrid payloads. Small GEOs can be enticing for those operators interested in following a step by step approach to supply hoping for rapid technology evolution and minimizing cost per Mbps sold.

Staying Cost-Effective

This right balance depends on the return on investment along with the risk associated. While VHTS payloads can essentially cost $700K per Gbps with a break-even pricing of $12/Mbps/month (including ground segment), small payloads can range between $3-$4M per Gbps, with a break-even pricing above $25/Mbps/month. This reduces risk with just 20-25 Gbps to fill, though reduces the competitiveness as well at a very high break-even point.

Seeking the Right Use Case

It would be very difficult for a Small GEO platform to compete head to head in cost / Gbps supplied against VHTS platforms. However, other attributes make them superior for specific use cases. Time to market can sometimes be significantly more critical than purely economical performances. While not a case for HTS, the need from the C-Band Alliance to have 8 new operational satellites in a 18-36 month timeframe can be an excellent example.

A recurrent challenge for satellite operators newly adding HTS capacity is being able to develop sales channels and stimulate demand, especially after large amounts of CAPEX have been spent on a satellite order leaving little room for investment in distribution channels. A smaller payload can be more manageable leveraging a first mover advantage and developing market efforts in a more focused manner. This can also be the case for niche markets like Alaska, where Astranis and PDI partnered to launch a Small GEO HTS platform. This same model may be replicated in underserved or concentrated markets where time to market is essential and the need is currently high.

Small GEOs could also be an alternative to legacy models like hosted payloads. Independence is highly valued among Government customers, and a wider range of nations could have access to their own GovSatCom satellites. Even some large private consumers of satellite bandwidth (cruise, energy, etc) could be interested in such technologies to gain another layer of security and control. Similarly, some actors downstream in the value chain could potentially be interested in Small GEOs with custom payloads like the recent order from Ovzon for a small-class GEO satellite from Maxar.

Bottom Line

Data will undoubtedly be the future growth driver, and operators must find ways into these new markets. Consequently, HTS is gaining traction among operators. However, with a wide range of supply options and different customer profiles and risk appetite, operators are in front of one of the most challenging times when designing their future payloads.

Small GEOs do present interesting benefits like smaller CAPEX and less complex transition to data-driven business models. However, in a purely economical comparison, large HTS payloads can be significantly more cost-efficient. All in all, large HTS payloads will generate the bulk of the supply, but Small GEOs will capture niche opportunities from specific use cases like ultra-local supply requirements, custom payloads willing to pay a premium for independence or when time-to-market is critical. NSR has recently learned from numerous satellite operators that small GEOs are now being considered for deployment (in markets like Asia), so we do expect more news to come on small GEOs in the future supply equation.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.