Connectivity-as-a-Service for Transport Operations

The adoption of Industrial IoT (IIoT) continues to drive the digitization and automation of the commercial transportation sector, whether it is land, maritime or air transport. As the need for tracking and monitoring applications increases, there are more bits streaming from containers, engines and vehicles – ample opportunity for the satellite communications industry to move beyond just the role of a connectivity service provider, into an integrated end-to-end digital solutions provider.

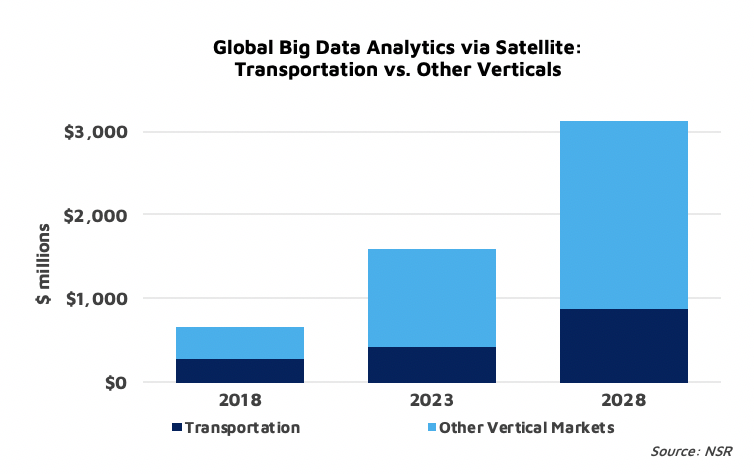

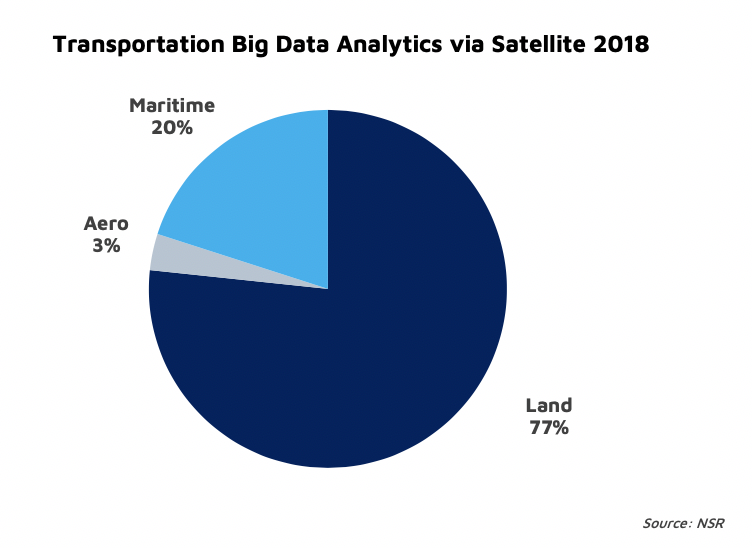

NSR’s Big Data Analytics via Satellite, 3rd Edition report identifies this Transportation sector to be the largest vertical market at close to $280 million generated in 2018, just over 40% of global satellite-based Big Data revenues as of last year. Users of these services in the aviation, cargo and shipping industries rely on applications ranging from fleet management and cargo telematics to maritime domain awareness and crew safety. However, despite other market verticals such as Energy, Infrastructure & Services and Gov/Mil eating into the revenue share by 2028 and pushing the Transportation sector down to 28% of the global satellite Big Data opportunity, it will continue to remain the largest sector, growing at 12.3% CAGR through the coming decade.

Existing and upcoming regulations are a significant driver of analytics adoption in this industry for the short term, but fleet owners can expect to derive significant returns from digitalization in the long term. Compliance requirements with the ELD mandates to boost driver safety continue to make a mark in North America are but one example of this trend. End-to-end supply chain traceability and regulations for cold perishables and pharmaceutical transportation is another. Meanwhile in the maritime industry, a global cap on Sulphur content of emissions in 2020 is expected to come into force, pushing the need for emissions monitoring and tracking applications. Regulatory compliance for normal/distress mode airline tracking is also expected to drive this market, with the use of space-based ADS-B and connected cockpit solutions.

M2M/IoT based transportation analytics solutions remains one of the more mature “Big Data” plays for the satcom industry, in contrast to the recent rise of EO-based applications in the financial services and agriculture sectors. It features a variety of microservices already established with best practices and standardization, that existing service providers can take advantage of to provide deeper insights and value-add to their customers. Orbcomm, for instance, has strengthened its hold over the market for end-to-end solutions through acquisitions and partnerships in recent years, shifting its focus downstream towards land telematics and AIS-based analytics. Maritime satcom players are not far behind, as evidenced by the Marlink-Transmetrics partnership that aims to tackle existing inefficiencies in cargo transport and the logistics chain. AI-powered diagnostics solutions for the airline industry is yet another example, allowing airlines to tackle fuel efficiency issues with Big Data.

While M2M/IoT based applications drive a majority of the Transportation vertical for satellite Big Data, Earth Observation-based applications are also on the rise. Planet’s maritime monitoring services allow customers to pair its maritime datasets with other AIS feeds for an integrated vessel tracking solution. Meanwhile, the Big Data opportunity driven by the market for connected/autonomous vehicles cannot be ignored completely, as next-gen location intelligence systems become more important in the long term: satellite players are beginning to make headway on this front.

The Bottom Line

Data in the mobility markets is inherently complex, providing enough opportunity for satellite players to roll out Big Data services that help customers optimize operations and track assets. IoT Connectivity-as-a-Service is slowly becoming more prevalent, and regulatory compliance requirements will drive the market for satellite Big Data services in the Transportation vertical over the coming decade.

Competitive pressure is expected from terrestrial players in the long term, especially as low power WANs roll out in the future. However, an increasing need for visibility into global transport operations in the wake of cyber-risk concerns will sustain demand for reliable, secure and single platform satellite M2M/IoT solutions.