Consumers, COVID, and Cannibalisation of Land Mobile Satcom

2020 was a tumultuous year, and overall had the expected impact for Land Mobile usage, with handhelds, fixed voice and Push-to-Talk (PTT) revenues down year-over-year. One positive out of last year’s experience is a boost in demand for consumer handheld form factors as consumers seek more experiences with social distancing in remote areas. However, these lower ARPU devices are becoming increasingly used with enterprise customers as well, which reflects some risk of market cannibalisation. With consumer devices on the rise, what does this mean for operators and how should they tap into this growing usage?

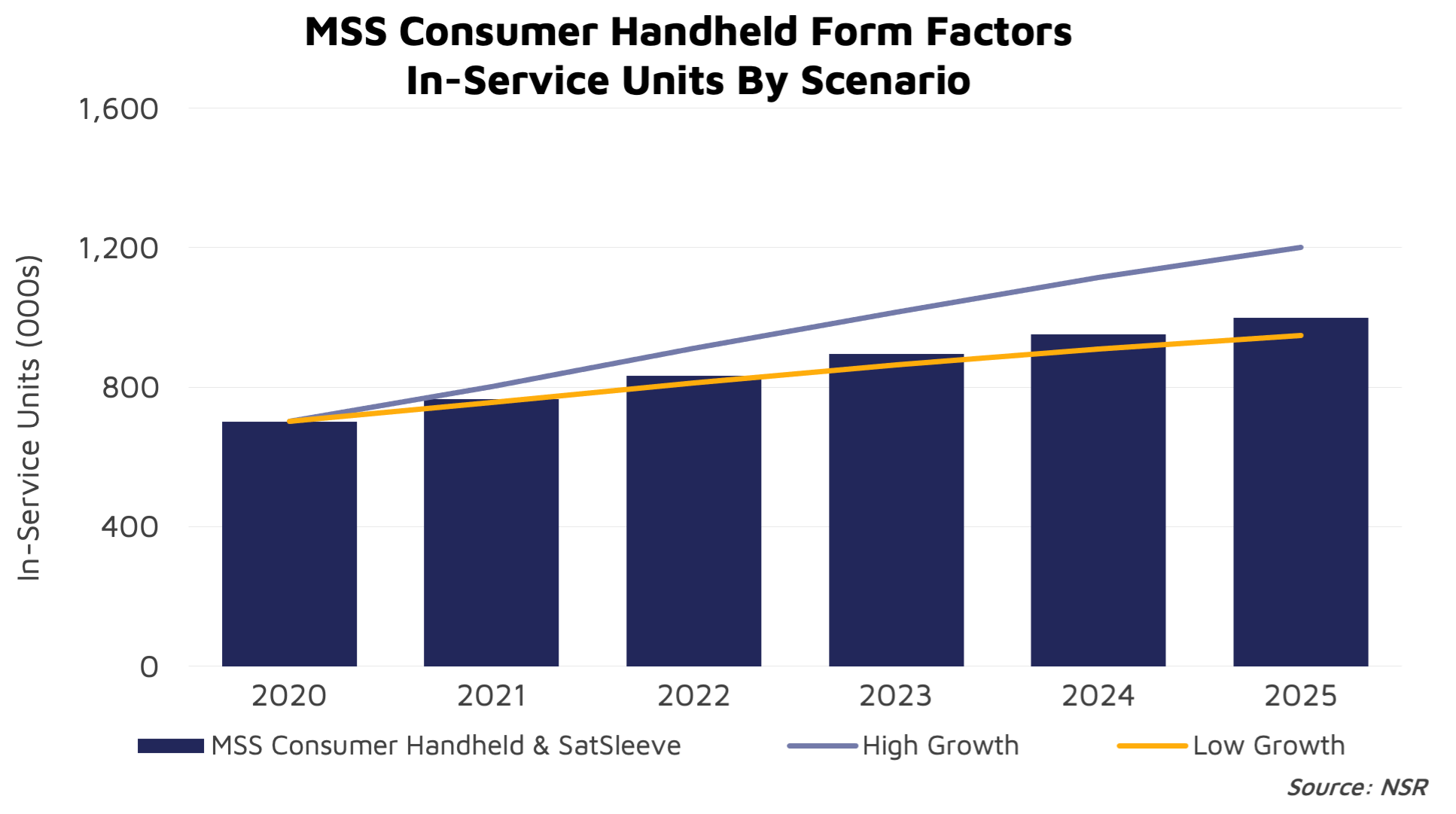

Consumer handhelds have gone from strength to strength the past year, all the while the main types of users haven’t changed: mountaineers, outback travellers, and eco-tourism usage. NSR’s recently released Land Mobile via Satellite, 9th Edition, found that the number of active devices will increase from 702,000 in 2020 to 1.2 million in 2030, with a higher growth scenario of over 1.6 million active units should there be a stronger marketplace of consumer form factor handhelds.

ARPUs remain very low compared to other applications; however, not all consumers are price-sensitive in this market and are more likely to have greater levels of disposable income. Globalstar for instance, reported an increase in usage throughout the year combined with a raise in pricing plans, demonstrating this. To cater to this increasing demand, a number of new consumer handheld form factors, have been released, with the newest entrant being Zoleo. Moving to 2021, air travel is on the rise, especially in the United States, resulting in consumers feeling more comfortable travelling further away from home to rural regions. This has further boosted equipment sales of consumer units in the latter half of 2020 and moving into 2021. Put together, NSR expects this growth trajectory to continue.

However, NSR views that there is only one satcom winner from this growth (for now): Iridium. This is in part due to Iridium’s open model strategy in supporting external partners to develop such devices to use on their network. This encourages many companies to go to market with the Iridium network. This contrasts with Globalstar’s closed model, which limits product usage to the SPOT device range. While strategically this offers Globalstar a greater portion of the subscription revenue base, the product range is more limiting and restricts growth potential from a broader product line-up.

The main downside of Iridium’s strategy is that with the level of growth of consumer on Iridium’s network, so much of this is dominated by Garmin, that the company may become overly dependent on the product for growth, which could be problematic if Garmin changes technologies or completely new products come along. For now, this is manageable.

Alongside this strong growth, is potential cannibalisation of higher ARPU services and more fully featured hardware such as hotspots and traditional satellite handhelds. We are already seeing Government agencies, such as those operating in rural areas, including the U.S. and France’s Forestry Services, also use SPOT devices in addition to consumers, and will increasingly drive demand in agencies for safety applications, contributing to further growth. Other types of usage include basic vehicle/cargo tracking, personnel safety and alerts.

From Iridium’s perspective this cannibalisation isn’t much of a problem as this keeps end-users in their ecosystem, with an end user going for a Garmin InReach over another Iridium MSS product is a win. This has already occurred to some extent, driving blended Iridium overall ARPUs ever lower. However, this could be a larger problem for Inmarsat due to the lack of consumer-friendly alternatives. There is perhaps potential for Inmarsat to join the party with their recent agreement with SkyLo.

Further, implementation of such as a strategy, despite cannibalisation risk, is key due to the introduction of smallsat constellations. While these will primarily be used for IoT type use cases, the companies are planning on introducing two-way messaging use cases on some devices and networks, which will overlap with current consumer handheld form factors, but with much lower pricing expected.

Bottom Line

Consumer handhelds grew in demand during 2020 and share of consumer handheld form factors will increase in the medium term. This is likened to increasing consumerization in IT years ago. Longer term, revenue growth will decelerate slightly as NSR expects such devices to attract less “low hanging fruit” on the consumer side, with lower price points and more sporadic usage. However, it will remain important for satellite operators to keep up consumer devices and continue to innovate along with strategic broadening of the user base with dual-mode solutions, especially as Iridium Certus devices are rolled out. All preferably with a strategy that permits a “free market” of form factors. Operators leaving out the development of the consumer side of the market will not only leave revenues on the table but will also cede these revenues to competitors.