Demystifying Satellite Big Data

Data has been called the oil of the digital economy, and the power of Big Data analytics has rapidly caught up among various sectors of economic activity, including the satellite industry. Satellites are undoubtedly a source of Big Data, orbiting the Earth and generating petabytes of sensor data every day. However, the complexity of accessing and exploiting satellite data, combined with in-depth thematic knowledge, makes the satellite Big Data industry different from other Big Data businesses, due to the need for specialized raw data processing.

NSR’s Big Data via Satellite report takes a deep dive into this upcoming market, and forecasts a cumulative revenue opportunity of $15.8 billion until 2026, only for the satellite industry! A common finding of the research, which was developed for 7 different vertical markets, was that the creation of successful services from satellite Big Data will be dependent on the bundling of information derived from satellite data with other available non-space data sources. The trick is to make satellite data components invisible for the final users, because their concern is related to information usability and utility, not data.

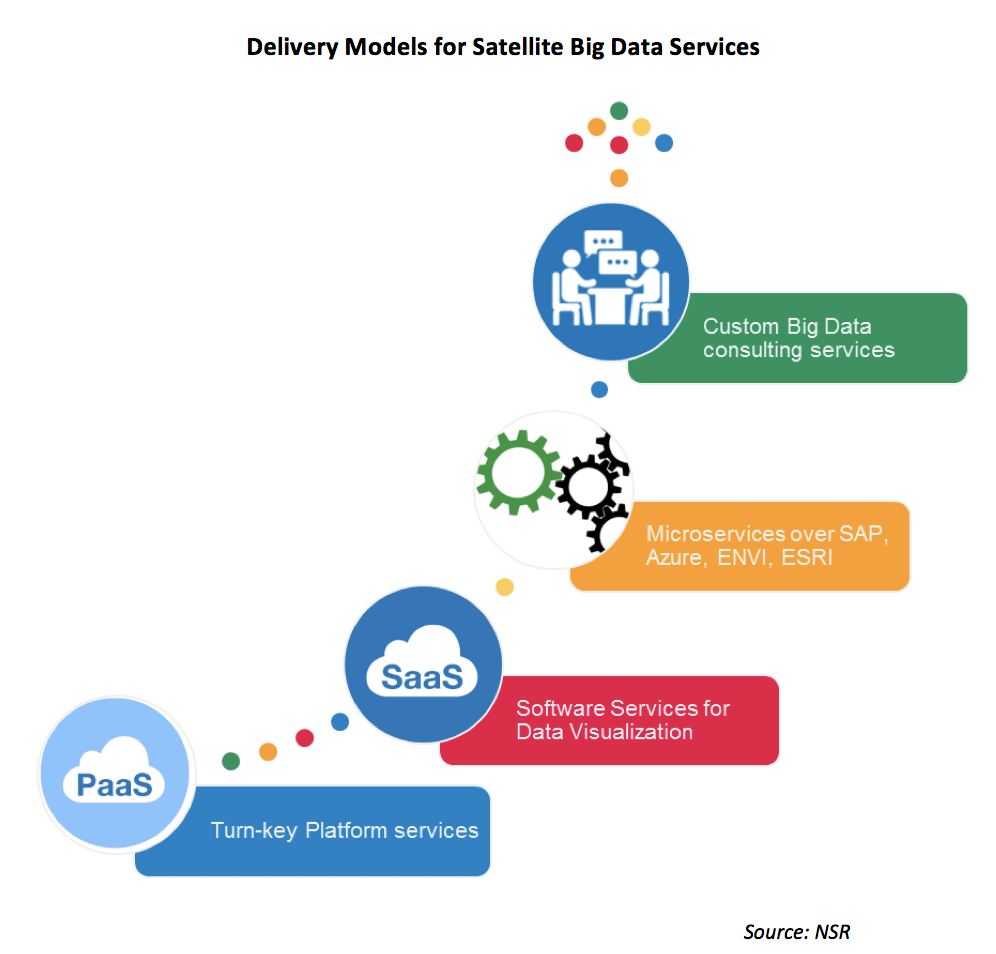

While the 4Vs – Volume, Velocity, Variety, and Veracity of data remain the pillars for satellite Big Data as well, the most important ‘V’ for satellite-based solutions is the ‘value’ created for the end-user. The importance of value creation for the end-user has surprisingly been understated by the majority of the satellite Big Data industry, with the focus being more on the technology stack used for creating new applications. There has been sufficient interest from the market for such specialized niche services; however, the discussion on closing the business case of companies into satellite Big Data analytics must touch upon aspects such as the ‘critical mass’ of customers, strategic partnerships for product development, and sales and distribution channels (SaaS/PaaS/Custom Consulting), which NSR believes would become the KPIs for the success of such services & solutions.

NSR found the satellite M2M/IoT Big Data business is currently more established than Earth Observation (EO) applications, due to a multitude of tracking and remote monitoring solutions enabled by narrowband satellite services. However, EO Big Data applications are expected to rapidly grow to 48% of the total satellite Big Data revenues by 2026, with most vertical market expected to register growth at more than 15% CAGR. Even though traditional geo-information companies have the advantage of having an established customer base, NSR expects satellite EO Big Data companies to create and develop their markets from scratch at a considerable pace, since they do not come with the baggage of traditional satellite EO industry mindset.

With international agencies like the United Nations and World Bank having shown a strong interest in investigating the viability of using satellite EO Big Data for improving official statistics on a wide variety of topics, spanning from agriculture, the environment, business activity, to transport, the success of this nascent industry with be largely driven by how the current and future stakeholders roll out their business moving forward. To elaborate on this point and quote Matt Epstein, Managing Director at Aremet Energy, “B2B business is tough, because the customer knows more about his business than the solution or service provider, and will only agree to pay up when there is a visible value-addition to his business. Hence, the more time, money, and effort satellite Big Data companies spend with their target clientele, specifically with early adopters, the easier it will be for them to figure out the triggers that would get these customers onboarded on their solutions & services”.

Bottom Line

The satellite Big Data business is here to stay as an integral part of the general Big Data analytics industry. With so many technological avenues to serve a variety of applications, satellite Big Data analytics companies will require a closer relationship with their clientele, focusing on the efforts of these companies towards saving time, cost, and effort, as they develop niche and valuable solutions, by bunding satellite data with non-space data.

With any emerging business, especially one so dependent on technology, there is a tendency to engineer solutions and look for customers later. NSR believes the churn the satellite industry (both EO and Satcom) is currently undergoing will act as a cautionary note against falling in the “product-market fit” trap again while creating a Big Data strategy, and keep the focus trained on the needs of the customer.