Did the Satcom Industry Hit a Hard Reset?

It is no longer news that the global satcom industry is stuck in a period of stunted growth, revenue declines and uneven investor appetite. When it appeared 2020 might be a sigh of relief following industry-resetting M&As of the 2016-19 era, COVID-19 emerged, further exacerbating an already distressed industry. However, the “hard reset” in 2020 may actually have created a stronger, but very different, satcom industry post COVID-19.

According to NSR’s Satellite Industry Financial Analysis, 10th Edition (SIFA10) report, the global satcom industry contracted by 2.7% in 2019 on the back of continued decline of video revenues. However, this is not a one-off revenue decline but a sustained manifestation of headwinds in the satcom industry’s critical segment: satellite operations.

While video shows no signs of recovery due to the growth of OTT platforms and the massive shift of advertising revenues away from TV to social media platforms, other segments, notably broadband, mobility and Gov/Mil with promising growth paths required much more capital investment and innovation to become profitable.

The industry’s challenges persisted into 2020 when COVID-19 kicked in the door, forcing debt-laden operators and cash-strapped service providers to file for bankruptcies. Industry leaders like Speedcast and GEE were unable to weather the COVID-19 headwinds with low cash reserves – declaring bankruptcy, while Gogo sold its commercial aviation division to Intelsat in mid-2020. Notable bankruptcies also included Intelsat and OneWeb, which needed to restructure debt or raise fresh funds.

Was That Just COVID-19?

Well, it appears COVID-19 only accelerated the events that were a long way coming and is on a path to force widespread industry hard reset. Findings from NSR’s SIFA10 Report indicate some of the industry’s concerning trends continued in 2019, and it was just a matter of time before the new wave of bankruptcies and M&As began. The following critical trends signaled an industry in need of a reset, although this might have happened gradually without COVID-19 becoming widespread in 2020.

-

Declining Backlog and Years of Backlog to Annual Revenue

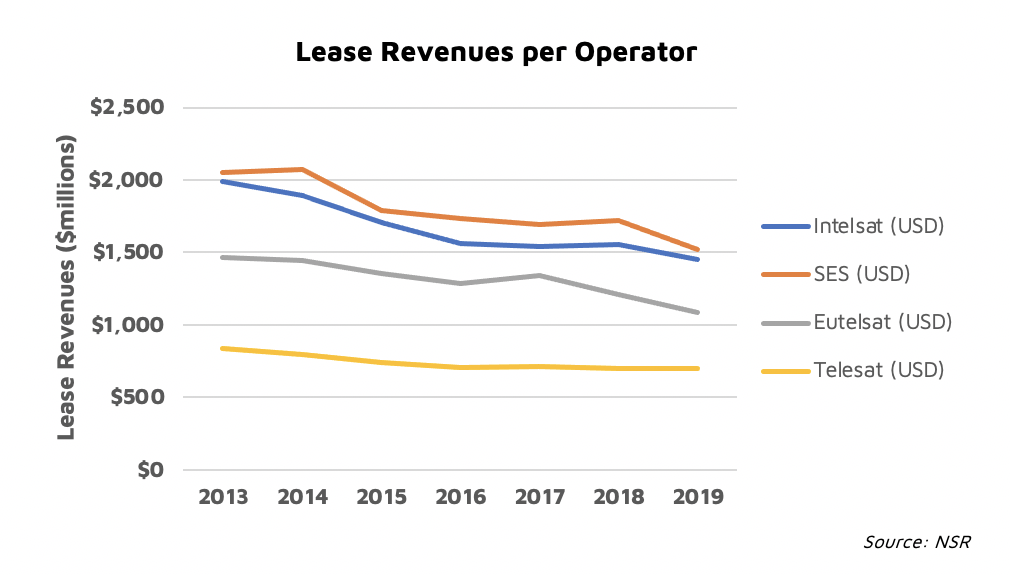

Over the last several years, most operators, including the Big Six, have reported YoY backlog decline across all verticals coupled with growing preference for short-term contracts. Thus 1-3 years is fast becoming typical contract duration in the network segment with options to renegotiate price annually, while the video segment is declining to 3-7 years. This trend gives service providers some leverage to seek more discounts on price and volume in line with rapidly evolving market dynamics. Its implication for operators is multi-fold as it breeds uncertainty, threatens customer retention and pushes the adoption of a subscription-based model.

-

Mixed Top-line and EBITDA Decline

Top-line figures show mixed results with a decline in video/lease revenues and increased service/non-video revenues. However, increasing service/non-video revenue has come at the expense of EBITDA, forcing service providers with a low cash reserve into bankruptcies. Examples include Speedcast and GEE.

EBITDA margin has been on a downward spiral for service providers on the back of increasing customer acquisition cost, and now for operators due to declining revenues. Integrated operators, such as Hughes and ViaSat, are the exception as revenue and EBITDA increased YoY.

-

ROCE and Pricing Pressure

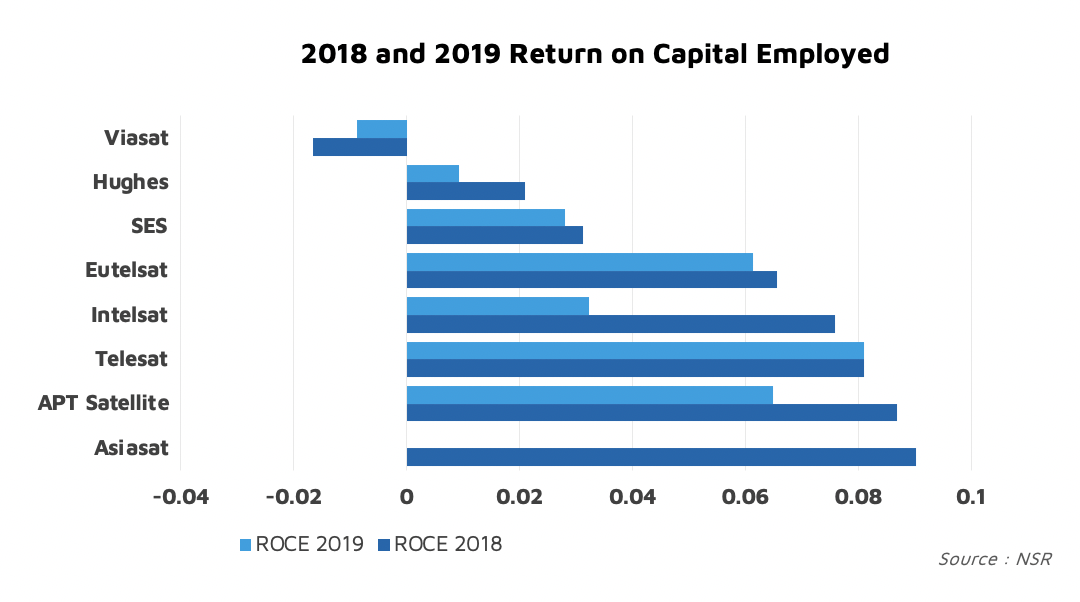

Return on Capital Employed (ROCE) continued to decline as customers demand more price discounts, directly eroding the value of critical assets. This trend has a long-term effect on satcom market dynamics as both smaller operators and the Big Six are caught in the murky water of price competition. Smaller operators feel the hit the most. Eutelsat, Telesat and AsiaSat show relatively better performance on ROCE due to a sustained wholesale business. However, ROCE will continue to decline as the industry shifts towards the service business. The implication is that investors will become more concerned, further exacerbating likely waning investor interest in this segment of the industry.

The Bottom Line

So, what is the overall implication of the hard reset? Well, that seems quite obvious as the resultant effect manifested in 2020 – a hard reset amidst a wave of bankruptcies. The 2020 wave of bankruptcies: Intelsat, Speedcast, OneWeb and GEE, show the common theme of refreshing balance sheets and raising new capital, a hard reset that could see the industry emerge stronger post-COVID-19.

However, expect to see more acquisitions as declining backlog will force operators to the service business, thus pushing M&A in the industry. M&As will follow two major paths: geographical vs vertical. The geographical pathway will see big operators acquiring regional operators/SPs to gain domestic market shares. Examples already include Eutelsat’s acquisition of Noorsat and Arabsat’s acquisition of Greek-Cypriot satellite operator Hellas Sat. Intelsat’s acquisition of Gogo’s commercial aviation division further indicates a vertical approach.

Service providers will move further downstream with more subscription-based offerings. The longer-term effect will help stabilize prices for existing offerings and unlock more addressable market when the next circle of innovation arrives.

NSR supports satellite operators, service providers, investors, financial institution, government entities and other corporates in their technology, investment, and business strategy assessment and planning. Please contact info@nsr.com for more information.