Does Price Elasticity Exist for Satcom Markets?

Pricing has been the most painful headache for satellite operators for the last couple of years. Rapid erosion in pricing, coupled with lackluster top line demand, has led to widespread revenue declines. With the industry readying for the next tsunami of capacity supply coming from LEO constellations and VHTS, pricing is unlikely to rebound anytime soon. Will satcom be able to stimulate enough demand to generate revenue growth?

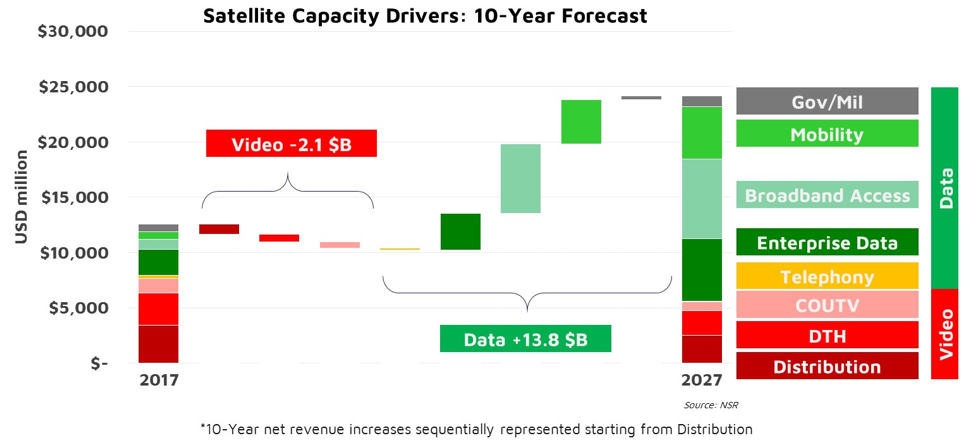

Multiple factors, both customer-centric and supply-driven, are aligning to generate the perfect storm for capacity prices. Consequently, the industry has seen revenue declines for the last 2 years. However, lower pricing does not necessarily need to be bad news for the industry, and NSR sees lower price points as the key to unlocking new markets. According to NSR’s Global Satellite Capacity Supply and Demand, 15th Edition report, satellite capacity revenues will grow at 6.8% CAGR over the next 10 years, expanding to $24.2 billion annually.

What is Driving Erosion in Pricing?

Each application has a very different set of drivers behind the degradation in pricing. While Video has been a bit more stable, it couldn’t escape from a progressive decline in price points. What is more concerning in this case is that the main drivers are customer-centric. OTT is starting to impact the subscriber count for DTH platforms, which is triggering traditionally big users of satellite capacity such as DirecTV, Dish, Sky or even actors in emerging markets such as Claro (Latin America) or Tata Sky (India) to launch their own streaming platforms independent of satellite. COUTV clients are migrating to terrestrial alternatives, and fiber is fiercely competing against satellite for distribution to head ends. All in all, media platforms are less reliant on satellite to reach their customers and distribute their content. Consequently, their willingness to pay for satellite capacity is degrading.

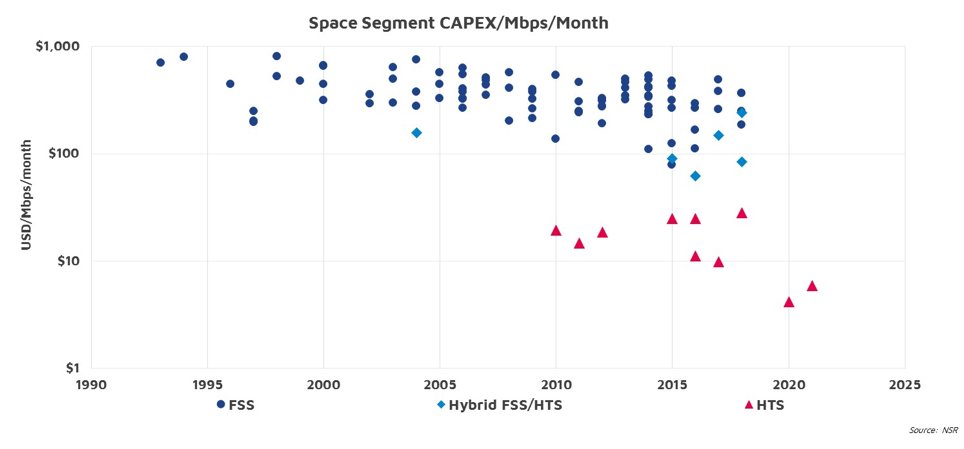

On the other hand, price erosion in data verticals is driven by a technology disruption. CAPEX/Mbps/Month for HTS is an order of magnitude smaller than for traditional widebeam satellites. Technology evolution continues at a quite rapid pace with HTS unit cost declining 50% every 5 years. This, mixed with abundance of supply, will lead to a continued downward trend in pricing.

Which Markets Will Take-off with Lower Prices?

Satellite capacity is a fixed cost for Video platforms. As the number of subscribers shrink, those costs are spread among a fewer number of customers. Furthermore, OTT platforms are increasing the price pressure on DTH platforms as service costs are usually much lower. In the end, capacity price declines in this vertical are a defensive move by satellite operators to avoid financially draining their video customers, but NSR sees video applications behaving inelastically. Channel count might grow as new niche content is added and emerging markets see the development of new platforms, some motivated by lower capacity pricing, but improvement in compression will lead to stagnant TPE leases. This combined with declining pricing will inevitably lead to a depressed revenue scenario for video applications.

Data verticals comprise a wide range of applications. Some of these use cases have little incentive to sign up for satellite services or boost bandwidth consumption with lower capacity prices. Having said that, several key verticals will experience impressive levels of demand elasticity, propelling the next wave of growth for the satellite industry.

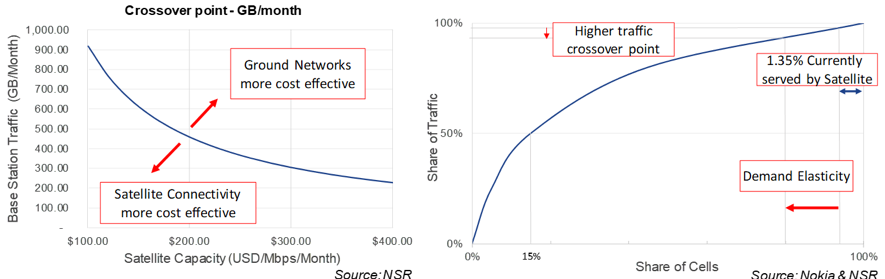

Cellular Backhaul is one such application. With lower price points, the monthly traffic at which satellite is more cost effective than terrestrial alternatives grows rapidly, especially as prices go below $400 USD/Mbps/Month. As there is a long tail of BTS stations consuming small amounts of traffic, an improvement in the GB/month at which satellite is more attractive than terrestrial solutions, then translates rapidly into higher levels of demand for satellite. A similar case could be built for Consumer Broadband as multiple studies suggest penetration skyrockets when services meet the “1 for 2” benchmark (1 GB of data priced below 2% of the GNI per capita). Last but not least, mobility will witness extraordinary growth as lower prices trigger adoption of Broadband services for maritime platforms and passengers on planes see connectivity reaching affordable levels.

While bandwidth pricing is a key driver for stimulating demand, one must not forget there are other barriers that drag growth. Installation, maintenance and even traffic routing and control requirements sometimes add complexity to backhaul deployments; underdeveloped distribution channels make consumer broadband a challenging business; and cost of the terminal is a big piece of the TCO in mobility applications.

Bottom Line

Price elasticity of demand exists for some key verticals in the satellite communications industry. However, legacy revenue generators (video) still weight more in the total mix. Consequently, price declines have had a negative impact on industry’s revenues.

Video platforms are reducing their reliance on satellite for reaching customers. Consequently, their willingness to pay for satellite capacity is eroding. On the other hand, HTS reduced the unit cost of satellite capacity for data services by an order of magnitude, driving rapid price declines.

Lower pricing does not necessarily need to be bad news. The “ABCs” of satellite communications will generate spectacular growth stimulated by lower TCOs and reduced capacity prices. Aero (and maritime), Backhaul and Consumer Broadband will drive the next wave of growth in the Satcom industry.

NSR supports equipment vendors, service providers, satellite operators, end-users and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.