Energy Satcom Markets: Digitalization Digs In

The mining industry, which has so far remained the smallest addressable market for the energy satcom providers, is gradually morphing into a growth opportunity for satellite connectivity. On the heels of the last commodities downswing, globally diversified miners are focused on increasing productivity and maximizing the value of their existing assets, while newer mining juniors are moving into exploration opportunities to meet expected demands. These factors, converging with the industry’s impending move towards mine digitalization in the wake of the “fully automated mine” presents a growing revenue opportunity for satcom players.

NSR’s Energy Markets via Satellite, 7th Edition reported the market opportunity for satcom in mining will grow by more than $150M from 2017 to 2027, at a faster rate than the traditional O&G market that forms the bulk of the energy satcom markets. As technology adoption efforts seep into all aspects and phases of mining, explorers are now seeing more intensive data reporting practices, including the use of real-time images and video from remote locations. Meanwhile, the data usage in established and larger production mines is driven by the adoption of IoT sensors, demanding high-bandwidth capacities. The notion that real-time visibility into mining operations will allow for enhanced production efficiency, safer environments, reduced (cyber)risk and improved compliance manifests itself in the digitalization strategies of major miners and juniors alike, and this will only increase, going forward.

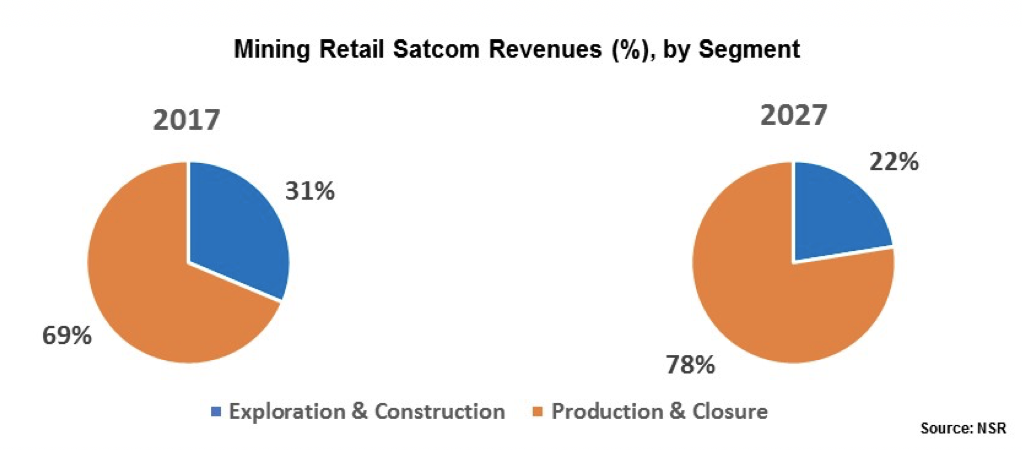

The revenue opportunity for satcom largely leans towards mines in production and later stages, with retail revenues in production more than double the opportunity in exploration and development mines. The growth of retail revenues at 8.6% CAGR from 2017 to 2027 will be largely driven by an industry hungry for low latency, high-bandwidth connectivity. It is an industry with requirements that non-GEO HTS can meet, and an opportunity ripe for the taking by satcom service providers.

On the other hand, this opportunity has not gone unnoticed by satellite operators. In early 2018, SES announced an agreement with Ivanhoe Mines to deliver managed services to a copper mining project in the DRC. The communications solution will enable the use of data-hungry cloud-based applications, be it video-conferencing, email or crew welfare apps, improving overall productivity and safety of the mine.

This uptick in high bandwidth requirements will drive retail revenues and the adoption of LEO/MEO capacities with improved latency, but FSS-Ku band will retain its dominance over capacity revenues despite low growth, driven by low-throughput critical communication requirements in the development and production mine phases. Additionally, miners are primarily concerned with coverage that is reliable and secure, alongside cost of the service. Even as terrestrial fiber and microwave reach more remote locations (particularly in production sites that last decades), the market for satcom will remain, either as backup connectivity services where more reliable terrestrial networks can be laid out, or as secure parallel networks.

Bottom Line

As the mining sector recovers from the commodities downturn, major mining corporations are cautiously focused on expanding established assets to maximize production. Meanwhile, the upswing in commodity prices has boosted exploration efforts by mining juniors. With the demand for both traditional and new-age minerals set to increase in the future, the mining industry will provide many more use cases for satellite connectivity.

Additionally, the industry is fast changing its perspective on technology adoption, as more and more miners look to leverage IoT and data analytics by a strategic shift in focus towards development of the connected, automated, intelligent mine. This strong push for digitalization coupled with strengthening market conditions will yield satcom an emerging market opportunity in the mining industry.