EO Smallsat Market: Where to Go from Here?

These days, smallsats generate a lot of attention, from players raising millions of dollars, losing millions of dollars, or providing thousands of images to spy on Iranian oil smugglers. Among the attention and potential, it is fair to say that the overall picture of the emerging EO smallsat market is sending mixed signals. Smallsat operators, now more than 40, all expect to capture a sizeable piece of the EO downstream market. The questions are: How big is this pie and who is it for?

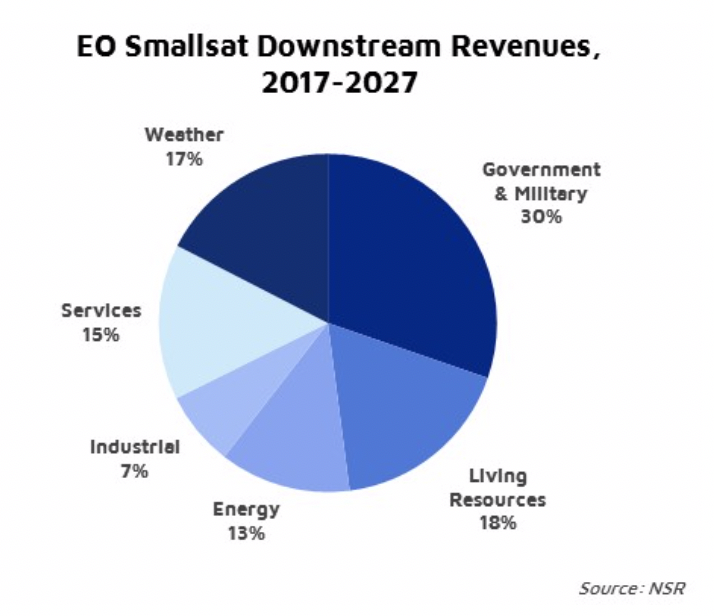

NSR’s Satellite-Based Earth Observation, 10th Edition report forecasts the EO smallsat downstream market will experience double-digit CAGRs, and cumulatively account for $9.7B in revenue over the next decade. Growth will come from all verticals, but a large segment of this growth is to arrive in the form of Big Data analytics for Defense & Intelligence and Managed Living Resources (Agriculture, Forestry, etc.).

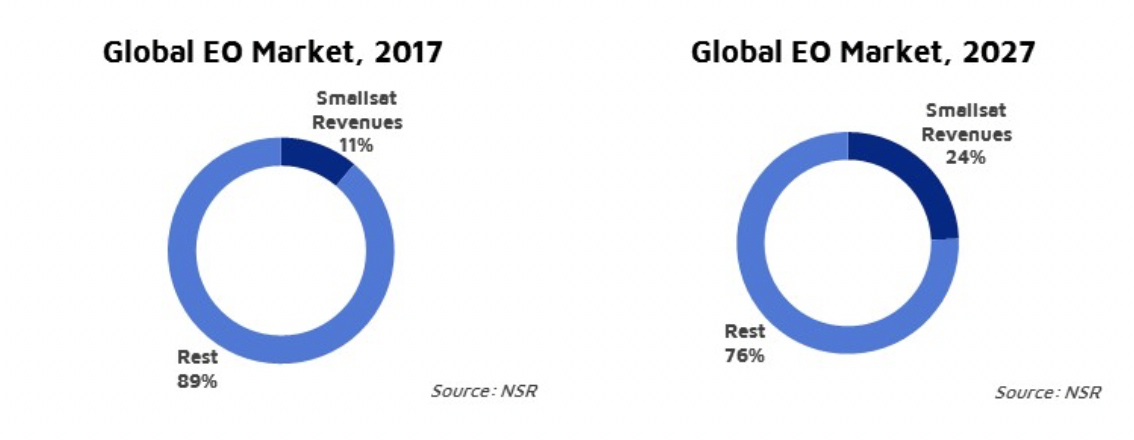

Smallsat players are expected to push their revenue envelope, growing from controlling 11% of all EO downstream revenues in 2017, to 24% by 2027. EO revenues are growing, due to high volume imagery sales and a growing focus on analytics, from HR and MR imagery.

Most of the demand will focus on HR and MR data and analytics. For area monitoring, MR is generally satisfactory, and suitable to a large percentage of customers. HR provides a better resolution of target, especially important for analytics and target monitoring, and HR imagery is generally less expensive and more accessible than VHR. As such, most of the supply coming to the market will focus on HR and MR, from players such as Planet, Earth-I, BlackSky Global, Planet, Urthecast and Astro Digital.

Another factor driving change and growth in the industry is the devaluation of imagery and the growing focus on Big Data analytics. Currently, Big Data analytics players favor MR imagery due to its easier access and lower costs. However, upcoming supply and growing archives are serving to depreciate the cost of imagery, lowering the barrier to entry for utilization of HR imagery.

Additionally, freely accessible MR imagery from programs such as Sentinel and Landsat, are shifting the revenue focus in MR from data to analytics. Ecometrica, which grew its revenues by 109%, while almost doubling its profit serves as a potential example to the opportunities that exist with using freely accessible data. As a result, while HR and MR data and analytics will drive the revenues, HR is expected to control more than double that of MR revenues by 2027.

Bottom Line

EO downstream revenues are forecast to grow four-fold from here. The focus will be on Defense & Intelligence, and Managed Living Resources verticals, and especially for HR and MR imagery, due to coming supply, continuing demand, and shifting focus on analytics. As investment and interest continues for EO smallsats, operators must consider these dynamics, as the tradeoffs between resolution types and data vs. analytics will be key to more effectively target the market and ensure their upward trajectory.