In-Orbit Servicing: Technology and Market Readiness Undocked

The space industry is full of acronyms, but TRL or “Technology Readiness Level” is one that we hear often for many new and emerging markets. As a measure of the availability and status of the technology required for an operation, it gives an indication of how close to ‘lift-off’ is the said technology. In-orbit services have been constrained to low TRL due to lack of (enough) in-orbit demonstrations and thus a lack of confidence amongst customers. With the recent successful docking of MEV-1 with Intelsat-901, the technology readiness level for life extension has moved up to TRL 8 – 9 by validating a successful system level demonstration. As such, technology is no longer a hurdle for life extension from becoming a true space service.

However, technology is just a small – albeit significant – part of the puzzle, and the long-term success of the in-orbit servicing business model will rely heavily on the market interest and readiness.

A Sustainable Business Case or Just an Expensive Steppingstone?

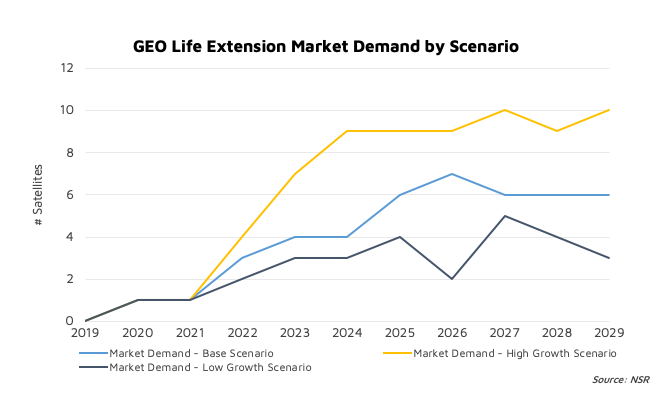

NSR’s In-orbit Servicing & Space Situational Awareness Markets, 3rd Edition report forecasts a demand for 44 GEO life extension missions by 2029 in the base scenario. The biggest drivers of the demand growth will be MEV’s mission success as well as the current GEO environment, which is compelling operators to delay investments in future procurements. While the most tangible advantage of life extension comes in the form of deferred CAPEX, a more significant benefit is that life extension is a steppingstone for other in-orbit applications. Indeed, as rendez-vous and docking are arguably some of the most challenging manoeuvres to overcome for most other in-orbit applications too, this operation cleared the path for robotics, salvage, de-orbiting and (to some extent) active debris removal, all of which not only offer immediate cost benefits, but also open more sustainable space possibilities.

However, over the last few years, the industry has developed alternative solutions like small GEOs, flexible and software defined systems, hosted payloads and condosats, all of which allow for low CAPEX investment and are therefore in direct competition with life extension services. Additionally, with rapid technology development in all areas of satellite manufacturing and launch, extending the life of an asset, which is already starting to average around 20 years, is no longer considered very valuable. The current prices of life extension services, especially, do not provide an attractive cost-to-benefit ratio. While this will improve over time, allowing the demand for life extension services to grow, in all of the scenarios, NSR expects the growth of life extension services to plateau towards the end of the decade as other technologies mature and in-orbit servicing moves to the next phase of its life cycle.

A Question of Perception?

Sustainability of space will rely on the ability to de-orbit satellites safely at end of life, salvaging repairable satellites, debris removal and recycling components from defunct satellites. Additionally, Space Situational Awareness (SSA) will be vital in providing more accurate and precise data to ensure a safe and sustainable orbital environment.

Despite the recent near misses of defunct satellites, risk of unresponsive satellites from mega constellations and anti-satellite missions, most players are still kicking the can down the road, and do not see the value in paying for a problem that is perceived to not exist right now. A disparate acknowledgment of the risks involved, outdated regulations and lack of clear and widely accepted technical and safety standards and regulations are some of the biggest hurdles, restraining the commercial market for these services.

Bottom Line

Technology and market are two different sides of the same coin in that both are essential for the success of a business model. On the technology side, the space industry experienced an incredible achievement with the successful docking of MEV-1 with Intelsat 901 on February 26th, 2020. This does not just mark the beginning of life extension services but opens the doors to applications that can change the industry as we know it.

On the other side, market readiness for any application takes into consideration the assessment of its benefits against costs and the market tolerance for its pricing. For in-orbit services, including SSA, technology might be (close to) ready but there are many hurdles that are yet to overcome in order to raise the market readiness levels.