Insight-as-a-Service for Satellite Networks

The terrestrial telecom industry is fast shifting towards 5G networks, with Software Defined Networks (SDN) and Network Functions Virtualization (NFV) forming key parts of major strategic efforts. This is seen in multiple market movements where organizations such as Verizon, AT&T and Ericsson have begun to shift towards adopting SDN/NFV approaches to manage increasingly complex networks. But what does this mean for satellite players, and how can they remain competitive?

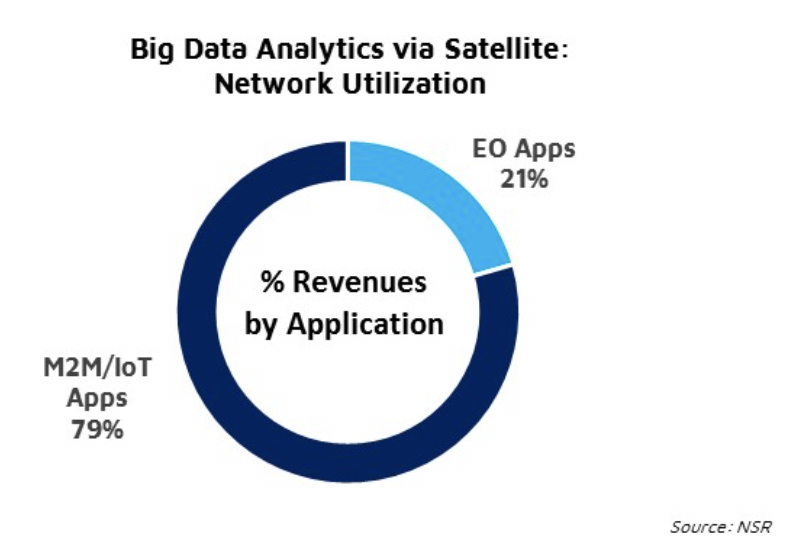

With satellite operators beginning to unlock value behind pixels and bits, the industry is moving downstream towards a data-driven application business. Earth Observation (EO) and Machine-to-Machine (M2M) / Internet-of-Things (IoT) satcom stand at an inflection point. While most of the opportunity will remain in the application layer, a parallel story is emerging in the network layer as well. NSR recognizes this potential opportunity as part of the Network Utilization vertical.

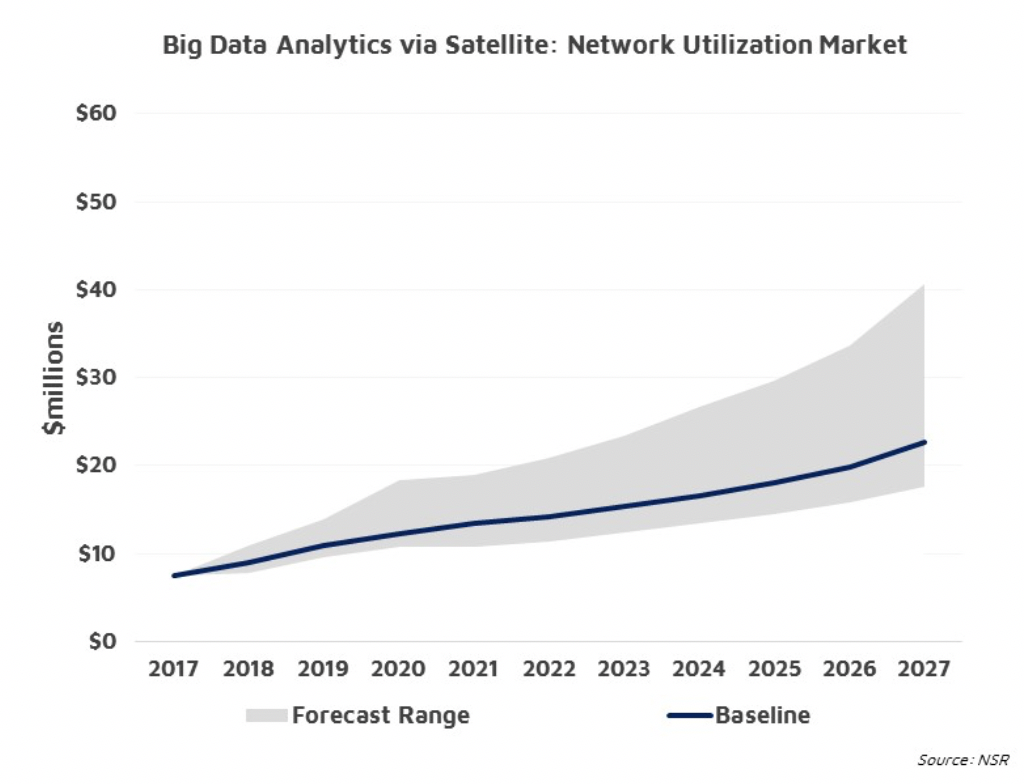

NSR’s Big Data Analytics via Satellite, 2nd Edition report establishes the revenue potential for satellite big data lies largely in the Transportation, Gov/Mil and Energy markets. Amongst the 7 verticals identified in the report, Network Utilization and Reporting stands out as the smallest piece of the pie, expected to grow at 11.7% CAGR from 2017 to 2027, moving beyond $20 million in revenue by 2027. This will include Software-as-a-Service (SaaS) applications that improve the network management strategies of satellite operators and service providers (SPs), and even RF spectrum monitoring services on the ground/from space.

A major driving force of this growth is the increasing complexity of networks. Satcom companies are already making acquisitions and forging partnerships to meet the surging demand for connectivity. Customer demand for value-added-services (VAS) is ever increasing, and satellite players cannot afford to remain behind their terrestrial counterparts. The ability to provide customized solutions with a quick turnaround time will be key in gaining a competitive advantage. On the other hand, the pricing decline of satcom capacity spurred by increasing capacity supply puts network operators/SPs at risk of lower margins.

The promise of HTS is well underway, and the rise of non-GEO satcom constellations will only add to the complexity. With applications ranging from mobility to energy taking up HTS supply, this complexity will increase furthermore with every subsequent node added to the network, making effective bandwidth management more critical. Solving this problem will be key if satellite players want to meet increased capacity demand and reduce the OPEX of network operations as well.

Adopting “cloud-first” virtualization and automation strategies will play a major role here, and they have quickly ramped up on this: in late 2017, SES used dynamic bandwidth allocation based on SDN principles on its O3b fleet. The adoption of such methods to manage spectrum allocation, thereby providing a highly reliable QoS to customers operating many distributed assets will ensure the satcom industry remains competitive.

Partnering with and taking advantage of established experts in the big data ecosystem will be essential if satellite players intend to provide cost-effective solutions. iDirect, for instance, is making use of one such data analytics platform to provide satellite performance optimization solutions to their customers. Such a move will ensure that SPs/operators remain at the forefront of technology, shifting away from long transactional decision processes for bandwidth allocation, towards near real-time network management. Newer technologies can also be used to provide prescriptive insights to network operators, thus making complex networks manageable at lower costs.

The Bottom Line

As satellite networks continue to evolve in complexity, addressing bandwidth optimization problems will be significant in effective network management. Big Data solutions providing decision intelligence tools to address such problems will drive the market for Network Utilization.

Solution providers looking to capitalize on this opportunity will need to not only understand end-user requirements, but also address the security and privacy concerns posed by customers. Only then can satellite players hope to remain competitive and deliver reliable services that are economical and affordable.