Is Satellite Backhaul a Refuge in Times of COVID-19?

COVID-19 and the resulting quarantine has heavily and negatively impacted the satellite industry in profound ways, especially in the Energy, Aero IFC and Maritime (Cruise market) sectors. Broadband/mobile segments are heavily impacted as well but in different ways. Broadband access to homes and mobile phones (where most of the traffic is taking place) are experiencing network challenges, congestion and lower quality of service. Whether streaming Netflix on 4 devices, conducting real-time to near real-time sessions on Zoom, to more critical use cases where populations on lockdown rely on the Internet for work, healthcare, education and accessing food supplies, one trend is clear: COVID-19 punctuates the need to boost network performance not just where the digital divide persists, but in locations where traffic surges will occur post the pandemic era. What does this mean for Satellite Backhaul?

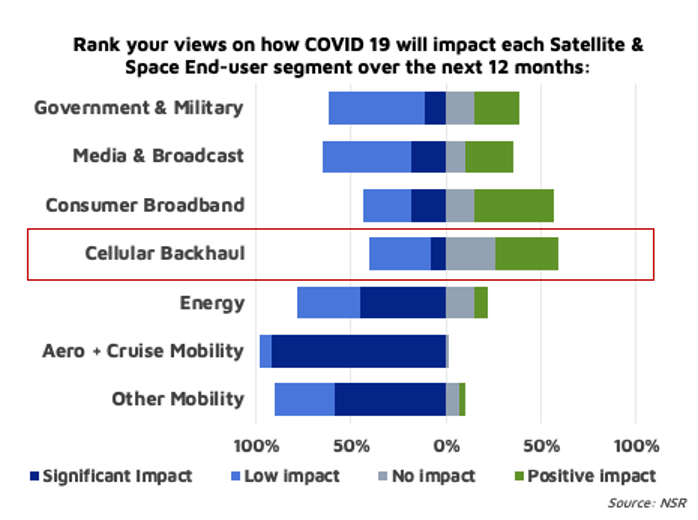

In a recent survey conducted by NSR, respondents overwhelmingly positioned Cellular Backhaul and Consumer Broadband as the least negatively impacted industries by COVID-19. More importantly, Cellular Backhaul will experience the highest levels of growth in terms of the ensuing market rebound. This finding is in line with growth expectations presented in NSR’s recently released Wireless Backhaul via Satellite, 14th Edition report.

From a government response level, UNESCO and the ITU’s Broadband Commission for Sustainable Development set a target of connecting 75% of the world’s population to fast internet via cable or wireless by 2025, even before COVID-19 hit. Regulators such as the FCC in the U.S. where more than 6% of the population (or 21 million people) have no high-speed connection, are putting forth measures to provide tele-medicine, tele-education and other critical services to unserved and underserved communities.

So, what is happening on the ground, and what is likely to take place over the next 3-12 months given the current situation?

- Most of the projects that were planned to be rolled out are obviously on hold with the consequent impact on revenues to the backhaul value chain. This impacts all use cases, and the situation will continue until the lockdown is over, depending on the country. As such, NSR expects a negative short-term revenue impact on the entire wireless backhaul ecosystem.

- Installed sites are seeing a spike in traffic demand, but this is difficult to monetize at this time. The same is happening with Consumer Broadband where demand has also seen a spike, but this is difficult to address as installers have stopped working and other supply chain issues prevent implementation. Once again, negative short-term revenue impact is foreseen.

- NSR has not seen much growth in emergency response demand, noting that this is a virus, not a natural disaster. But as terrestrial networks become saturated over time, impact and demand for backup satellite services should begin to take hold in response to future emergency response and crisis situations.

- Many of the RFPs that were ongoing are also on hold. This impacts digital divide programs as funds are moved to emergency response, economic stimulus and other programs. NSR sees negative impact once again in the next 6-12 months.

- Longer term or beyond the 12-month period, data usage will trigger many changes in customer behavior, and communications will be more critical than ever. NSR expects this to foster higher demand for resilient networks, emergency response, ubiquitous coverage and higher bandwidth support per site to address network congestion among the key measures to be implemented.

Bottom Line

Like most other satcom markets, the Satellite Backhaul market will be negatively impacted over the next 6-12 months. However, it is important to note it is not because the business fundamentals, value proposition and demand are not there. On the contrary, all key elements in building and closing a business case are present. More importantly, the COVID-19 pandemic has highlighted these critical aspects of the market.

The primary challenges that Satellite Backhaul currently face are due to logistical considerations where latent demand cannot be addressed because of the lockdown. But once the lockdown has been lifted and the installation of satellite BTS systems can begin to take place, the backhaul vertical will be one of the earliest to rebound.

The post-pandemic era will be one where governments and end users will clamor for ubiquitous, redundant and higher quality services from telcos and MNOs. The “new normal” (as they say) will need to incorporate higher-speed, higher-quality services at peak hours, not just in preparation for the next situation that may involve a lockdown, but as basic features in living in the “new normal” where communications is critical not only for a few key verticals like enterprises and governments but for everyone in their homes as well. At the very least, the definition and thresholds for contended services that feature comparatively lower SLAs will change.