Is There Room for New Players in Software-Defined Satellites?

Software-defined satellites (SDS) are gaining global attention, as new platforms continue to be announced by major manufacturers. Flexibility of satellite and network design is driving many operators to invest in SDS, with Intelsat’s upcoming launch of a flexible satellite, and Eutelsat’s recent order from Thales Alenia Space showing the pace is faster than ever.

While manufacturing and launch activity are increasing, most orders, if not all of them, include only a small number of well-established players. Few emerging companies or start-ups appear to be involved in the SDS business, which bring to attention room available for smaller players to play a key role in the SDS manufacturing market.

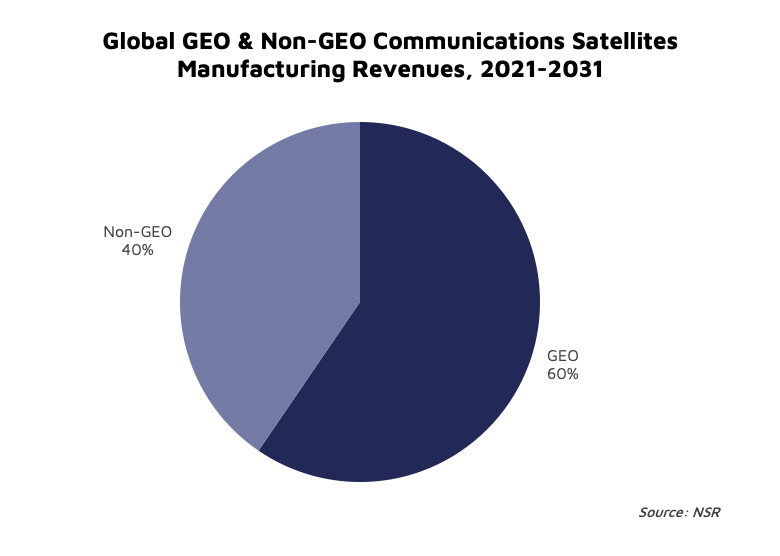

NSR’s Software Defined Satellite, 2nd Edition report forecasts over 27,000 satellites to be ordered by 2031, generating $64.3 billion in cumulative revenues. Non-GEO satellites drive these orders, as constellations dominate the manufacturing market with investments in SDS continuing to be strong. NSR forecasts 206 GEO Communications orders over the next decade, which, despite the much smaller number, generates 60% of cumulative manufacturing revenues due to the high cost of GEOs per satellite.

GEOs High-Barriers

Major players control the GEO market, leaving little to no space for small manufacturers in the SDS domain, due to the relatively low number of orders and the risks associated with this new technology.

Plus, flexibility comes with manufacturing challenges as its development of SDS is expensive and time-consuming, with manufacturers facing complex network requirements. The additional risk involved in meeting this complexity, coupled with the limited experience of newer players, increases the risk which operators are often not willing to take.

Moreover, players with wider portfolios and backlogs of orders are perhaps more capable of at supporting development of new applications, such as SDS, and even if that is not the case, they may be better placed to raise funding due to their position and place in the market.

Without these capabilities, smaller players have to shake up the market with novel approaches. Examples of this include Astranis and Saturn Satellite, who have been raising funds, securing orders from new clients, and applied novel “infrastructure-as-a-service” models. However, these untested models developed by emerging players are often co-opted by established players who can increase their competitive footing substantially just by applying these concepts to their current product lines.

Furthermore, the low GEO orders and high cost per satellite that has not decreased as much hoped for, apart from in-house consolidated exceptions, still see much interest thanks to SDS. But high development costs are often seen as inaccessible by smaller players.

Non-GEO Has Room

Emerging players experience difficulties in the Non-GEO market as well, but they can find a suitable place among this larger and more diverse landscape, compared to GEO.

Communication constellations are driving Non-GEO, leading to many SDS orders. Partially-flexible SDS is the “sweet spot”, as they are considered a balanced choice between providing software-driven capabilities, at a more moderate complexity and cost. NSR forecast nearly 26,000 partially- or fully-flexible satellites to be ordered over the decade, of which 55% will be partially-flexible each at a much lower cost per satellite at roughly $3.5 M.

But most orders are built in-house by players like SpaceX for its Starlink constellation and Amazon for its Kuiper project, which decreases significantly the addressable market. Outside of mega-constellations, the market is expected to grow but with less room to maneuver, small players will struggle to join the SDS market. As GEO orders continue, some operators are considering pivoting their strategies with Non-GEO players to a diversified architecture. If emerging players benefit from those strategies, they might find a window to the SDS market.

The Bottom Line

Small manufacturers do not have much space to move in the GEO market, considering how expensive GEO software-defined satellites are and the risks that come with this new technology. However, manufacturers may find greater opportunity in the Non-GEO market, where SDS orders are higher. In the end, if their strategies remain flexible to the needs of the ever-competitive communications market, smaller manufacturers will find more room to thrive in the SDS market.