Last Mile Delivery in Space: A Strategic Market

As the space sector experiences growth, satellite manufacturers are improving production capabilities to meet demand from players like EchoStar and Inmarsat. However, even with some good news stories such as for Starship and ISRO’s SSLV, launch service providers still struggle to keep up with the increasing demand for satellite deployment. Last Mile Delivery (LMD) service providers are stepping up to address the challenge of meeting the growing deployment demand and improve launch access. LMD providers can help to ease the burden on launch service providers, beyond the traditional services of integration, last-mile delivery, and constellation/mission planning. However, given the market is emerging and there’s more competition in the launch market, can Last Mile Delivery service providers gain market share, from whom, and how?

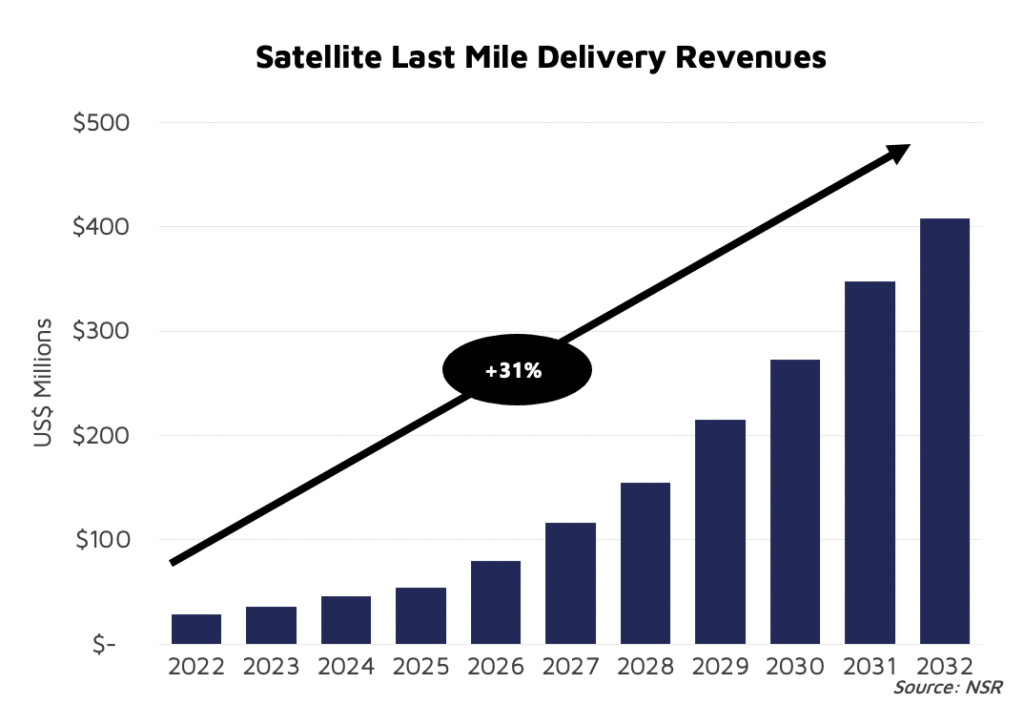

NSR’s In-Orbit Services: Satellite Servicing, ADR, and SSA 6th Edition report forecasts over 4,500 satellites could be serviced via Last Mile Delivery service providers. However, the actual market demand reaches only 1,350 satellites, generating over $1.8 billion in cumulative revenues. The lower market demand is primarily due to trade-offs between extremely reliable launchers and ridesharing launch cadence, which affects launch and deployment costs. Because of the availability of ridesharing options, LMD service providers are becoming increasingly aware of the pricing pressure in the launch market. This is especially true for smaller businesses and start-ups that lack funding for launches, the expertise to obtain necessary licenses, and the resources to comply with complex international regulatory standards for satellite deployment and operation.

Solving Price Pressure

LMD service providers may find it difficult to break into the market due to the high costs of satellite launches and the deployment technologies required to get them into orbit. However, ridesharing launches have a limited yearly launch cadence, which has a direct impact on the total mass launched to orbit metric and lowers the launcher payload capacity fill-rate. Despite enormous demand for launches, launch service providers are increasingly seeing this as a pressing issue. As a result, fewer satellites can be launched into orbit at the same time, making it more difficult to place satellites in the required orbits. As a result, LMD service providers must collaborate with satellite operators to ensure that their satellites are launched as quickly and affordably as possible. By offering a range of solutions, such as integration, constellation/mission planning, and hosted payloads, LMD providers make it easier for satellite operators to access launch services and complete satellite deployments to their intended orbits.

Last Mile Delivery (LMD) service providers are positioned as a bridge between launch service providers and satellite operators, and they are also making strategic moves to gain a market foothold. This includes obtaining financing and forming new strategic alliances to strengthen and expand their service offerings. Some LMD service providers, for example, Exotrail and Atomos, have raised new capital, while Spaceflight has formed new strategic alliances. Plasmos, a new entrant, has also introduced a dual-purpose vehicle to meet the growing demand for satellite deployment.

LMD service providers are capitalizing on the opportunities provided by cutting-edge technologies such as nano- and small satellites, and their delivery of satellites and hosted payloads provides satellite operators with several benefits. Because of the development of spacecraft that can function as a traditional deployer on steroids with special power, size, and deployment functionalities, LMD vehicles can be built for longer spacecraft life cycles. This creates new business opportunities for satellite-based services such as communication, edge computing, remote sensing, position, navigation, and timing technology development and testing. This trend is being driven by rising demand for these services in a variety of industries, including telecommunications, agriculture, and transportation.

The Bottom Line

The market opportunity for LMD is determined by the launch provider’s costs and capabilities. LMD providers can gain market share by offering cost-effective, flexible, and agile services, forming strategic alliances with launch providers and satellite operators, and innovating with added benefits such as payload hosting and longer spacecraft lifecycles. LMD providers need a dual-opportunity business model, good working relationships with launch providers, and simple satellite integration for operators to gain higher market share.