Maintaining Relevance for Satellite TV

While many actors in the satcom scene have turned their focus to data markets, the reality is that video continues to generate over 50% of overall satellite capacity revenues. OTT and other alternatives are slowly impacting DTH offers such that satellite needs to evolve to stay relevant. The set-top-box (STB) is at the forefront of the customer interaction, hosting applications that will make satellite TV continue to thrive. How should STB capabilities evolve for DTH to continue to be a successful market?

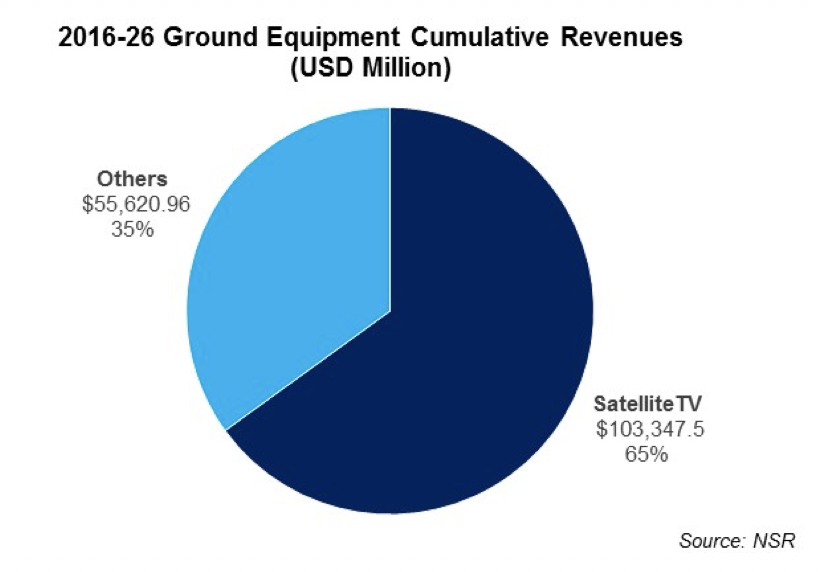

One of the only mass markets satellite has been able to penetrate is Satellite TV, generating over 120 million annual shipments in 2016. According to NSR’S Commercial Satellite Ground Segment 2nd Edition report, this translates to $103 billion in cumulative revenues over the next 10 years. However, the video market is under rapid transformation and technology must adapt to defend this massive revenue opportunity.

Technology Evolution Can’t Stop

OTT has real impact on subscriber churn via emergence of multi-channel platforms challenging traditional means of broadcasting. Technology evolution must continue to remain competitive against new threats. On one hand, new compression standards (MPEG4, HEVC) and advanced modulation schemes (DVB-S2X) can offer great capacity (and consequently cost) savings. On the other hand, satellite TV needs to catch up with the convenience of OTT, and some DTH platforms are opting to continue growing memory capacity to offer an on-demand experience.

One must not forget that cost is just one side of the equation. Some services that are natural to IP ecosystems are increasingly relevant, such as measuring user engagement and targeted advertising. Satellite must incorporate innovative products that can respond to these new requirements for enhancing TV platforms’ revenue potential.

An Ecosystem under Pressure

While OTT is a real challenger for the ecosystem, other factors have a major impact. Cost of content acquisition is growing, and only the largest operators can afford to sustain it. Competition is fierce in all steps of the value chain, even for TV platforms in emerging markets previously perceived as “blue oceans”. All in all, pressure on STB pricing is exacerbating at a time when investments in technology development are accelerating. This leads to a number of exits (STMicroelectronics), consolidations (Arris, Technicolor) and verticalizations (Dish-Echostar) in all steps of the value chain.

In this context, satellite operators need to take greater responsibility in ensuring a strong ecosystem. Beyond providing increased levels of services such as content aggregation, playout or content delivery, leading actors are taking the initiative in developing systems with advanced features such as Eutelsat’s SmartLNB offering a return link for interactive services or the Sat > IP alliance creating protocols to feed IP networks from a satellite link.

UHD and Multiscreen, Satcom Wildcards

With heavier content, the satellite multicast cost advantage is of higher relevance. Consequently, the migration to UHD is of prime importance for satcom. While some factors like the limited content available or the cost premium carried by UHD chipsets still drag widespread adoption, DTH platforms are progressively adding UHD content, and UHD TV prices are going down rapidly and thus increasing penetration and adoption. UHD share is still minimal today, but technology evolves quickly and UHD could take-off in the short term.

With consumption of video in the personal device skyrocketing, multiscreen becomes an essential feature. This transition goes in parallel with the consumption of higher quality video (HD and UHD), and satellite can offer a fantastic cost advantage in broadcasting this kind of heavy content. Initiatives like Sat > IP create the framework for multi-room/multi-screen content delivery, but overall acceptance in the market is still low.

Virtual Reality is still in very nascent stages, but satellite will need to play a major role in content distribution if (or when) this format takes off. Depending on the quality of the content, a single streaming of VR content could require as much as several hundred Mbps. Very few broadband links would be able to support these data rates, hence satellite has a tremendous opportunity to capture in the transition to broadcasting immersive video experiences.

Bottom Line

Satellite TV still generates the majority of capacity revenues and STBs, as the customer facing devices, play a primary role in the competitiveness of the solution. Satellite operators must not underestimate the importance of these elements in the end-to-end solution and should play a greater role shaping technological requirements.

The ecosystem is under pressure from multiple angles, and satellite operators need to make a step forward to ensure features continue evolving and offering the convenience and quality to stay relevant.

NSR supports equipment vendors, service providers, satellite operators, end-users and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.