Optical Satcom and the Digital Revolution

As enterprise and government actors digitize their systems and processes, they continue to transition to cloud-based services to meet their needs for more storage and data transportation solutions. The characteristics of optical satellite communications include speed and data volume are well placed to meet the needs of those customers with an ever-growing appetite for highly secure data storage and transfer services.

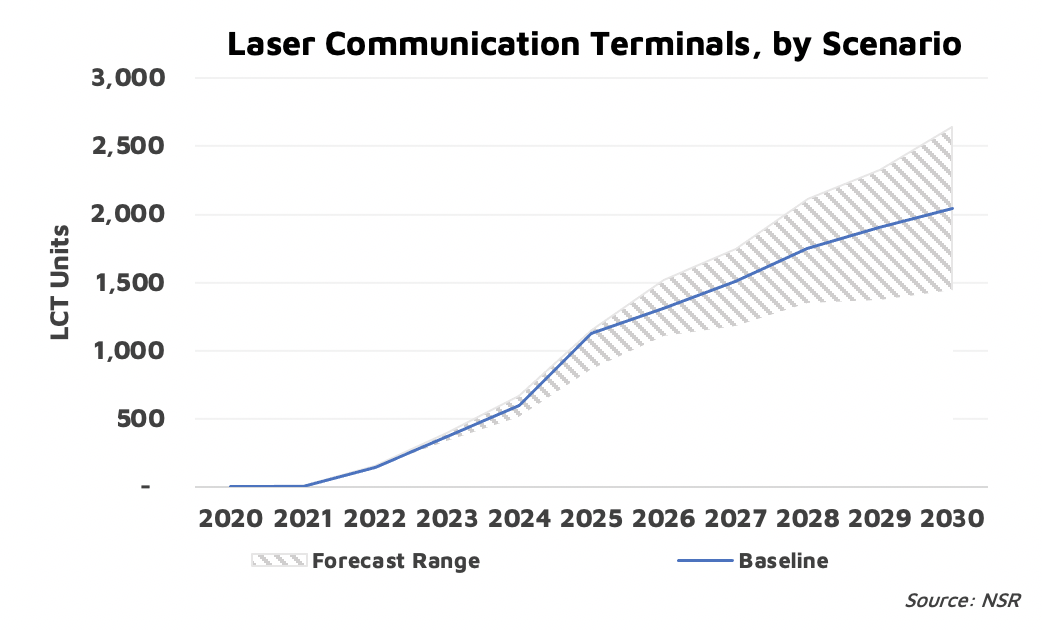

Demand is Developing

NSR’s Optical Satcom Markets, 3rd Edition report forecasts over 10,000 optical laser terminals will be launched into orbit over the coming decade. Revenues in this market are driven primarily by the expected demand from various constellations, requiring a large number of laser terminals, with many operators citing at least 3-4 per satellite.

In the last weeks alone, Japanese optical LEO relay startup Warpspace closed a $3.6M Series A round with the aim to have 3 optical satellites launched by 2023. General Atomics won a $6 million grant to conduct a space-to-air optical communication experiment with the U.S. Space Development Agency (SDA). And German manufacturer Mynaric signed a cooperation agreement with U.S. start-up SpaceLink and was later selected to deliver all optical intersatellite laser terminals for the first 10 SpaceBelt constellation satellites.

Security is Independence

Many deals have security as a key backdrop story. It continues to dominate user concerns, as seen with Microsoft’s latest announcement, the EU Data Boundary plan, which aims to satisfy customer concerns. Entities like SDA or NASA (aiming to launch an optical payload in June) and other institutions are no stranger to optical satcom, and the technology’s security applications have long been held up, especially in contested environments. We also find it is related to quantum key distribution (QKD) and communication research. LeoCloud recently announced a partnership with LeafSpace to enable space-edge computing services at collocated ground stations, with a purely optical satcom constellation in the planning. Lyteloop takes security one step further to offer data storage in space. A key benefit to in-orbit data storage relates to the independence of the owner’s data in space, free from the reach of terrestrial sovereignty and many judicial oversight impediments. Should this service catch on, having an optical satcom infrastructure as proposed would be a strong asset critical to enable the transition from terrestrial to orbital storage and computing at scale.

Longer term, cloud service providers could augment their service offering from today’s expanding regional data center availability to orbital availability for cloud services. Moreover, the speed and security brought by optical satcom applications could improve latency and unlock improved real-time intelligence applications. The need for timely and accessible data transfers from space assets at growing data volumes presents a commercial opportunity for optical data relay systems such as those proposed by SpaceLink, Skyloom Global, Warpspace, and Analytical Space.

Bottom Line

The global transition from hardware to software will continue to drive appetite for storage and computing power. Advancements in cloud technology will mean that many companies will have to adopt cloud solutions to stay competitive. This will lead to increasing demand for computing, storage and data transfer services and will push the adoption of secure high data volume and high speed (low latency) data transfer solutions. It’s a perfect match for Optical Satellite Communications systems. Lest we forget, Starlink’s recent partnership with Google Cloud, is perhaps a testament of what is to come.

But most importantly, satellite operators, optical terminal producers and data specialists understand that the ability to transfer data to remote locations quickly can bring tremendous value across multiple industry verticals. While many advantages place optical as a prime candidate for a next-gen satcom service, the commercial optical satcom business case is far from closed. The industry has seen rapid improvements with respect to the size of the technology, but challenges regarding pricing and the right product-market fit will still need to be addressed. But such infrastructures are expected to facilitate further digitalization that may otherwise not be economically feasible.

###