Optical Satcom: Under the Spotlight

With more data being created and circulated than ever before, Optical Wireless Communication (OWC) technology is emerging to serve the demand for higher data rates and lower latency, acting as an alternative or complementary to RF. Given its interconnections with both space and ground segments as well as with satellite operations, successful synergies are conducted by major players aiming at a fruitful incorporation of the OWC technology. But what is the technology readiness level (TRL), and what does it take for a broader market adoption?

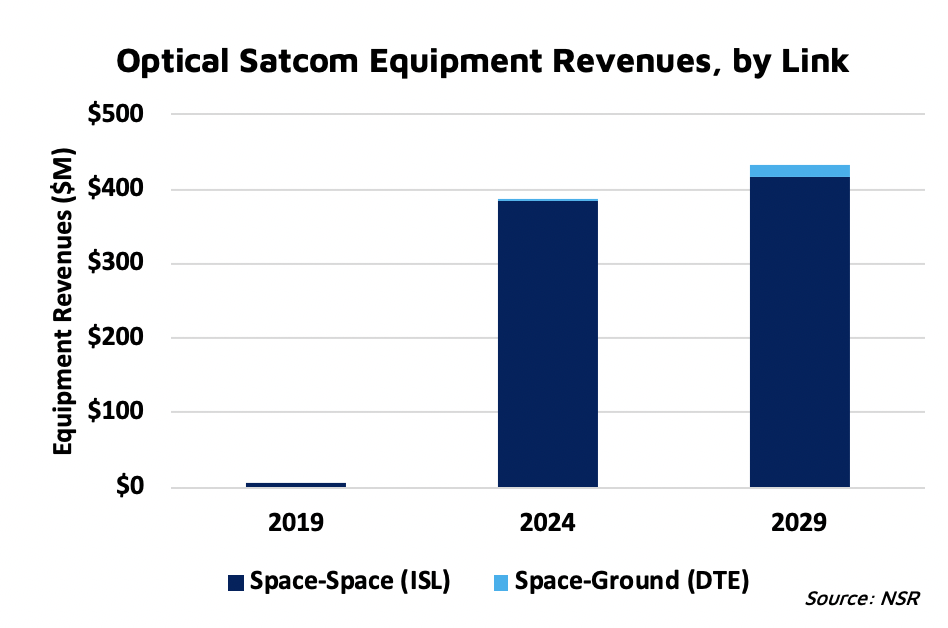

NSR’s Optical Satellite Communications, 2nd Edition report forecasts the Optical Intersatellite Link (O-ISL) market to reach nearly $3.8 billion in cumulative revenues by 2029 at a CAGR of 54.5%. By fully exploiting this innovative technology, it could rise to the competitiveness level of either existing RF solutions or virtualized cloud-based systems and meet the downlink volume demand in the long run. But it will take time, and NSR expects its adoption from one of its key segments, Earth Observation platforms, to begin beyond 2025, a year when the manufacturing cost per unit of the Laser Communication Terminals (LCTs) is expected to be reduced significantly. Applications linked with Optical Satcoms range from real-time, high definition video data to highly secure and intelligent communication services for government/military use and commercial instantaneous transactional data. Last but not least, OWC technology could facilitate the successful deployment of 5G/6G and IoT systems.

From a technological perspective, there is a great diversity of LCT manufacturers across regions catering to this market. Tesat-Spacecom has proven a high TRL through the SpaceDataHighway (SDH) LCTs in GEO and Bartolomeo with a 10 Gbps DTE (Down-to-Earth) lasercom system. In parallel, looking at the need for cooperation between space and ground segment, this is highlighted through partnerships among Tesat, KSAT and GomSpace and strategic alliances of BridgeComm with different EO operators and LCTs manufacturers; e.g. with HySpecIQ, aiming at a new LEO constellation. Established players such as Ball Aerospace and Thales Alenia Space, are gradually increasing the maturity level of their technology, while new Early Stage Terminal Manufacturers are joining, such as Astrogate, Xenesis, Odysseus Space.

In contrast, Optical Ground Station networks, although playing a pivotal role in the success of this technology, are still in development, facing a significant challenge from both technological and business perspective. The TRL of Optical Ground Segment is low, requiring large telescopes for higher precision, driving solution costs higher. Similarly to new technologies being developed for the SWaP miniaturization of space laser terminals, pushing forward ground laser terminals technology will play an important role towards optimized and commercially viable services.

Bottom Line

The rapidly growing space data downlink volume alongside the increasing access to information of remote areas, supports the transformation of digital technology. Future challenges consist of more intelligent and secure data transmission, always considering the rising trend in cyber-risk concerns of the commercial world.

Currently, the development and operational cost of Optical Communications Systems is, in its greater part, government-owned and operated. Once the terminal price drops and the business model consolidates, the transition to commercially developed services will be easier. Only then, a global and robust Optical Ground System infrastructure in support of the space-ground Optical link will reach commercial viability.