Polar Militarization a SATCOM Opportunity?

Conversations in 2019 on the U.S. position in the Arctic noted their inability to defend national interests compared to Russian forces within the region. SATCOM for government and military within the Arctic region increased based on these conversations, generating a noticeable CAGR. Non-GEO HTS is a highly attractive option to government and military interests, as GEO equatorial position is not favorable for operations in the region. The region also lacks cybersecurity and cloud services, leaving huge economic potential open to service providers. Overall, Government & Military SATCOM retail revenue will experience a growth rate of 6.1% over the next decade, with the Arctic experiencing a 39% growth rate over the same 10-year forecast as presented in NSR’s 19th Edition, Government and Military Satellite Communications report.

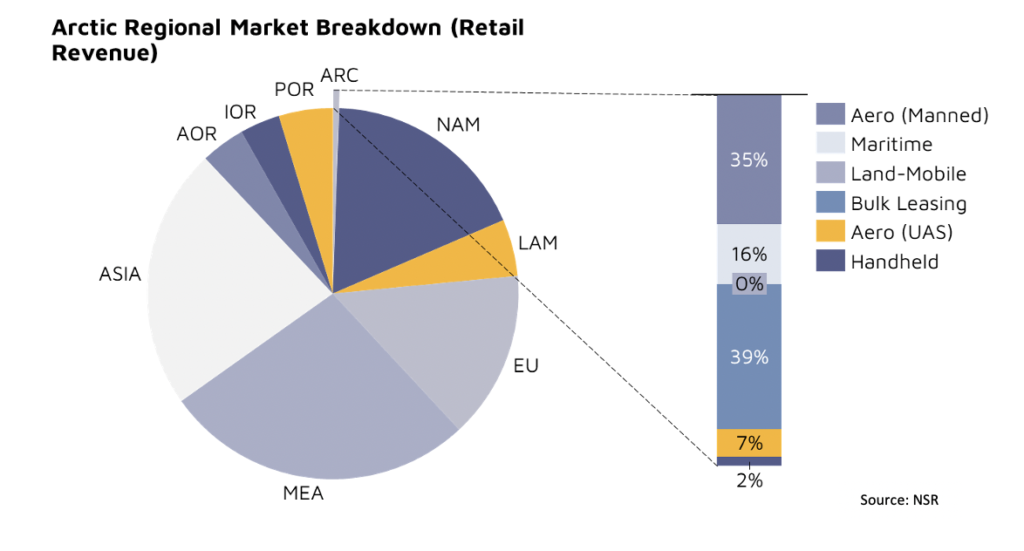

Interest in the Arctic Region

The U.S., Canada, Europe, and Russia are finding new economic opportunities within the Arctic. A lot of discussion surrounding investment happened in the late 2010s into early 2020s, but the beginning of Arctic service uptake is starting to show via revenue from 2023 into the early 2030s. Between 2021 and 2031, satellite connectivity services for government and military users will reach USD$382M, growing at a rate of 40.9%. Driven by these new economic opportunities, the Arctic is experiencing a growing need for SATCOM services.

Commercial players such as OneWeb and SpaceX Starlink are investing in capturing this growing opportunity. Both OneWeb and Starlink are including polar orbit satellites within their fleets, and SES continues to explore operating an inclined plane with O3b mPower. Government-owned programs also have an interest in connecting far northern latitudes, with countries such as Norway, UK, and U.S. under the “Arctic Satellite Broadband Mission” (ASBM) and Russia under the “Russian Satellite Communications Co.”. ASBM has a payload offering secure communications within the region, named “Enhanced Polar System Recapitalization” (EPS-R), launching in 2023.

Non-GEO Impact in the Arctic

While demand continues to grow for Arctic connectivity, Non-GEO HTS demand dominates (0 Gbps ’21 to 41.8 Gbps ‘31) the Arctic. Once Non-GEO HTS is removed, GEO HTS Ka-band is the second largest capacity demand. The Arctic’s niche requirements and specialized operating environment will restrict the overall revenue opportunity for commercial providers; however, for companies with the connectivity infrastructure – the opportunity to capture and grow a user base is appealing.

The Bottom Line

Driven by geopolitics, the Arctic will remain a region of growing interest. Having solid connectivity is essential to any military mission, and currently within the region it needs an “upgrade.” This “upgrade” is the latest technological advancements within SATCOM, covering low-latency, cybersecurity, and cloud infrastructure. As the Arctic becomes more connected, it will play a key role for any multi-domain network. Consequently, the growing SATCOM infrastructure in the Arctic will lead to growing economic opportunities, mainly geared towards service providers.