Powering Satcom through Distressed Financial Markets

Financial markets have had an oversized impact on the satcom industry of late. We have observed an alarming 35%-50% decline in stock prices of SES, Intelsat, Eutelsat and ViaSat in just over a month. 6-month declines fare even worse with companies finally being able to focus on profitability (barring Intelsat). So, does an 8% video decline YoY by SES or a 5% revenue decline by Eutelsat warrant this correction?

While C-band has been largely responsible for price volatility for Intelsat, the impact should have been positive for SES considering the ~4B in U.S. C-band proceeds. Similar is the case for ViaSat and Hughes, who have consistently posted revenue increases, with strong Govt and equipment sales performance over the past 2 years. One must account for COVID-19 impact in the month of March, as it adversely affects commercial airlines, cruise companies, and O&G sectors. Though, backhaul, consumer broadband, business aviation and linear video should certainly prove critical in the times of quarantine and increased bandwidth consumption and provide cushion to stock prices. Thus, it is imperative to understand the state of play in this “new normal”.

NSR believes the overreaction by markets calls into question the long-term strategy adopted by several publicly listed operators. Consistently reducing contract backlog, higher commoditization and low product differentiation seems to have left investors searching for unique business cases. Several satcom verticals need to show growth, and operators/service providers must quickly innovate to increase price-volume effectiveness, increase bandwidth on existing plans, look to unlock newer businesses (as price declines by double-digits every year) and find ways to deliver VoD/OTT via satellite.

While the COVID-19 impact will be felt for another 2-3 quarters (at least) based on demand erosion in key network segments of commercial aero, cruise and O&G (due to contract negotiations on volume); the industry should largely focus on five key areas detailed below to build a long-term GTM strategy.

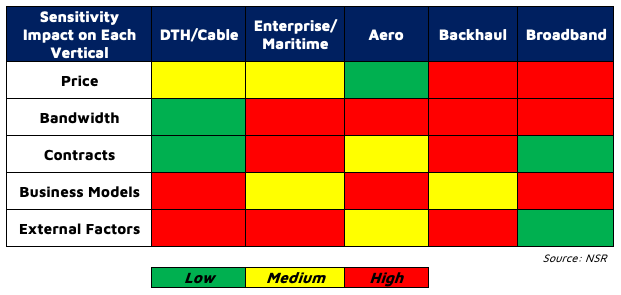

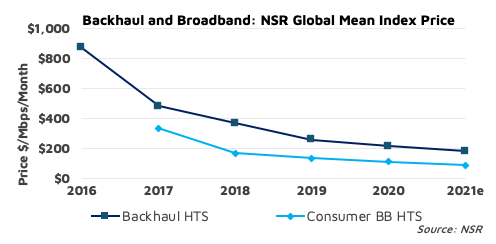

Price Sensitivity: Expected to be high in consumer broadband and backhaul segments. Adjusting to market prices in the short-term remains key, unless bulk deals are possible and enable high fill rates. Pricing across network verticals has decreased ~60-80% over the past 5 years as showcased in NSR’s Satellite Capacity Pricing Index, 6th Edition, and thus building the right fleet efficiencies to stay ahead of the pricing curve is paramount. For backhaul, this means unlocking high contract volumes selling at low(er) prices, with further growth expansion via smallcells in backhaul. For consumer broadband, operators will need to build low ARPU business models like community Wi-Fi as a global proposition.

Bandwidth Sensitivity: Deploying higher bandwidth per site is most critical for enterprise and maritime customers, with a high(er) reliance on modem efficiency to enable high bandwidth transition for IFC, while enabling increasing ARPU per site/vessel/plane YoY. An ability to match incremental capacity with incremental demand every year is crucial and will need a multi-orbit strategy to effectively mitigate volatile fill rates and consequent Return on Capital Employed.

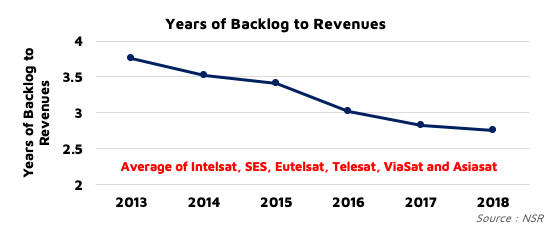

Contractual Sensitivity: Duration contract has decreased consistently, and with higher volume discounts and regional competition, backlog to revenue ratio has considerably declined as reported in NSR’s Satellite Industry Financial Analysis, 9th Edition. This decrease, with a current average 1.5 years of contract time, could keep investors from making long term bets, and in-turn reduce the market value of several operators. Reversing this trend remains important, by bringing the 4-year tech and 15-year satellite lifecycles closer and building a fleet that is highly complementary.

Business Model Sensitivity: Models are fast changing. With OTT/VoD the king, DTH/cable has lost relative importance, and operators should look at IP distribution or offloading to build secondary revenue channels. Large customers will look for a bargain sourcing managed services, while operators will look at Infrastructure-as-a-service for long term growth. Regional beam flexibility, multi-orbit capacity partnerships, and consolidation at the distribution layer all become critical to increase profit and reduce volatility risk. Ability to pivot business models with the same fleet and introducing “uberification” at scale on each layer (separating bandwidth consumption and generation) will be key in allowing investors to make long term bets. Regional top-down integration is another strategy that may be implemented, if the supply, equipment and distribution form a closed ecosystem.

External Factor Sensitivity: Some adjacent factors such as broadcasters decreasing connectivity costs, impact from increasing fiber coverage or impact from LEO should also be considered in future-proofing the business case. Scaling makes a huge difference in reducing sensitivity, where operators should focus either on:

- Building true scale to command highest fleet efficiency in a vertical, covering the majority of regions (ex: VHTS/MEO strategy effective)

- Or consider to sell/merge the business with a customer/competitor, where pricing decline is expected to be more than 50% in 4-5 years with revenue decline of 15-20%.

Bottom Line

Today, competition remains the biggest hurdle in stabilizing the top-line, and this is likely to exacerbate price wars. Rather, the industry must largely focus on either scaling fleets or M&As that consolidate the right fleet assets and the right verticals to build captive positions. Simultaneously, companies must fund innovation (internally or via start-ups) to predict MVPs of next product cycles that could be fast tracked in current business models.

Secondly, agile management of resources and quick pivot of business models remains key to unlocking growth. The company quick to build tech (think cloud) or distribution (think regional or application-specific) partnerships will be able to add value to existing products more seamlessly and be able to build secondary revenue channels faster in the future.