Price Optimization for Satellite Backhaul

Backhaul will undoubtedly be one of the key verticals for satcom growth in the coming years. Lower capacity pricing is certainly unlocking demand elasticities; however, not all markets are homogeneous in terms of adopting 2G, 3G and 4G services. Operators must find the right balance between stimulating demand through aggressive price offers while at the same time avoid revenue cannibalization for markets that only require 2G services. How should Satellite Operators set their pricing strategies and business models to optimize returns in the Backhaul market?

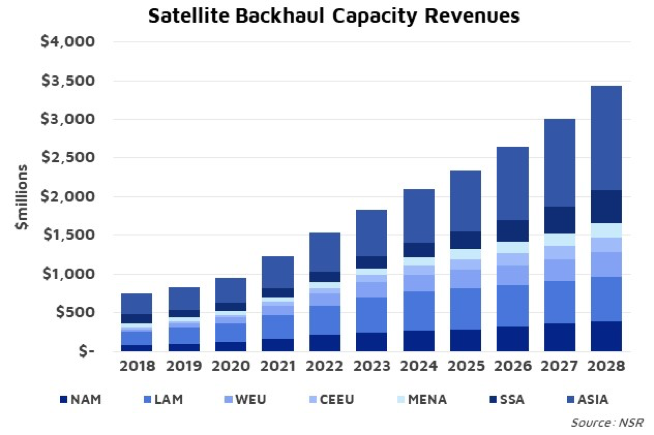

From a purely revenue generation standpoint, global satellite capacity revenues in the Backhaul market will grow at very high levels. According to NSR’s Wireless Backhaul and 5G over Satellite, 13th Edition report, capacity revenues will evolve at 16.5% CAGR over the next 10 years. But despite this rapid climb, MNOs are not an easy customer segment given their purchasing power and challenging internal processes. Consequently, the satellite industry must be very careful when articulating its value proposition by offering attractive pricing to stimulate demand but avoiding MNOs to disproportionally dominate value capture across the value chain.

Demand Elasticity in Broadband Markets

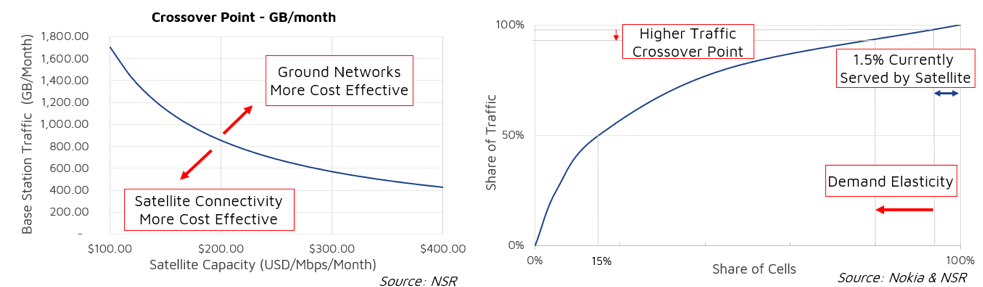

There are multiple factors to be considered when analyzing demand elasticity for Satellite Backhaul. These include the distance to the nearest backbone node as well as the volume of traffic to be carried by the base station, to name a few. What is clear is that for broadband sites (3G/4G), capacity pricing is a major factor in the Total Cost of Ownership (TCO) for the base station. In a 2G site, the cost of capacity might be in the 5-15% of the TCO range, which can easily climb to over 50% in a broadband site. Hence, capacity pricing elasticity is significantly more pronounced in broadband deployments.

Assuming a BTS 20 Km away from the closest backbone node, one could plot the data volume at which satellite is more cost effective than terrestrial alternatives as capacity pricing varies. With declining capacity prices, the crossover point grows rapidly towards higher data volumes, thus increasing satellite’s attractiveness. More interestingly, there is a long tail of stations carrying small levels of traffic. Consequently, improving the crossover point at which satellite is more efficient than terrestrial solutions will significantly expand the market capture for satcom.

Picking the Markets Wisely

While lower capacity pricing is critical to activate broadband deployments, some markets might not be ready for 3G/4G and lowering prices would only cannibalize revenues. This is the case for example in Africa, where NSR is aware of 3G test deployments in which end-users continued to use 2G services and the broadband connection remained idle. One must bear in mind that in many areas, income availability or smartphone penetration are still tremendous barriers.

Furthermore, there are tremendous differences in the price per GB depending on the conditions of each country (competition, terrain, quality of service, etc.). It would be very hard for satellite to close the business case in markets like India, where the average price per GB of a 4G plan is in the 0.26 $/GB range. On the other extreme, satcom is a perfectly viable solution in markets like Zimbabwe where data is priced at 75.20 $/GB. Each market and each deployment such as a first-responder network with high availability requirements that could hold a premium, needs to be priced strategically.

Understanding Customer Requirements First-Hand

The old wholesale model is very unfavorable for satellite operators, particularly in the backhaul market. MNOs are comfortable with reverse auctions and, given the large size of deals, MNOs are in a position to extract extraordinarily low prices. Moreover, perceptions play against satellite as many Mobile Operators still see satcom as an expensive and difficult to implement solution and do not really have the understanding, skills and initiative to adopt satellite.

In this sense, operators need to move closer to end-users and be more fully integrated in the technical and market aspects of the MNOs’ rural deployments and operations. This might involve adopting greater risks with co-investments where such arrangements have the advantage of capturing a greater share of the value generated (revenue-sharing schemes, pay-per-GB, etc.). Integrating more closely with MNOs not only facilitates the adoption of satcom solutions to MNOs but extracts greater value in terms of revenue generation for satcom operators.

Bottom Line

Backhaul will be one of the key areas for satcom growth in the coming years. Lower capacity pricing, advanced ground segment, and the need from MNOs to continue expanding coverage converge to create the right conditions for this market to take off. However, MNOs do have strong purchasing power, and satcom risks falling into the commoditization trap if the value proposition is not articulated strategically.

Lower capacity prices are necessary, especially in 3G/4G deployments. But some markets are still driven by 2G and a race to the bottom in pricing could cannibalize revenue opportunities. Even in broadband deployments, satcom needs to place barriers to avoid value flowing downstream to other actors in the value chain, for example adopting managed services business models.

It is essential that the industry gets a better understanding of end-user requirements in terms of bandwidth pricing (very wide variations from country to country) or network expectations (coverage, availability, etc.). Only by following these requirements closely will the satcom industry be able to optimize its business models.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.