SATCOM Data Traffic in GEO

Space data traffic is dominated by satellite communications (SATCOM), making up 530 EB out of the 566 EB of global space traffic over the period from 2021-2031. The SATCOM market is experiencing a transition from video to data, driven by changing end-user demand and technical innovations, with overall growth amounting to 26% by 2031. Within this figure, GEO currently serves as the largest platform for space traffic; however, changes are coming with Non-GEO constellations taking center stage.

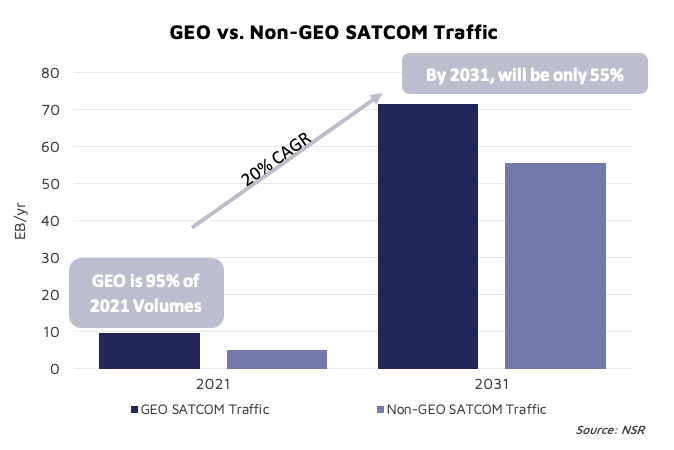

According to NSR’s latest study, NSR Space Traffic Study, 2nd Edition, GEO-based use cases for satellite connectivity will rise from 9 EB to 71 EB over the next decade. However, GEO needs to change tactics to continue competing within the connectivity provider market. Video is embarking on a new journey of “streaming”, leaving the traditional linear market in the dust. “Data” now frequently includes streaming media, leaving GEO providers to build new products and services around not only streaming media to consumers – but tailoring what’s left of the traditional video markets to better meet end-user needs. End-users want a cheaper solution to their ever-growing demand, as customers look to stream media across a range of household devices, engage in remote work or school, and remain connected with friends and family. All combined, GEO SATCOM data traffic volumes will amount to a cumulative of 335 EB, or roughly 60% of the total amount of data volumes projected for all space-based use cases, including Earth Observation, Situational Awareness, and Crew & Cargo, to name a few.

Losing the monopoly GEO once had on remote internet connectivity via satellite does not “spell disaster” to service providers but requires a change of business strategy. GEO still provides widebeam capabilities and already matured infrastructure on the ground for both FSS and HTS markets, of value to Government and Military customers and commercial service providers alike. The technology on-orbit as well is not standing still amongst this sea-change of on-orbit capabilities.

GEO continues to answer these challenges through innovative business models and technical solutions. The development of small GEOs allows service providers to acquire their own capacity using radically different ‘satellites as a service’ business models. Adaptive beam forming enhances network utilization improving $CAPEX per Mbps metrics, and utilization of Cloud Infrastructure unlocks the ability to scale up or down to meet market requirements. Looking forward, development of using more adaptive beams techniques will play an even greater role, with its capability to have multiple beams covering a region and eliminated idle or stranded capacity should market conditions change. Overall, Year-on-Year data traffic growth for GEO throughout ’21 to ‘31 is due to GEO maturity, with a record of high reliability and stability, including industry acknowledgement of needed innovation, which can be observed by their investment strategy.

However, GEO providers are no longer operating in a monopolistic environment, and the rapid advances of Non-GEO capabilities have put the entire satellite communications industry on unsure footing. Space Data traffic within Non-GEO will grow exponentially with a CAGR of 53%. Military operations such as those in the Ukraine are showing some of the potential advantages of a Non-GEO connectivity system, cruise ships are highlighting the transformative impacts it can bring to the guest experience, and other connectivity verticals are weighing the risks vs. reward of adopting new or hybrid connectivity architectures. Beyond connectivity markets once owned by GEO infrastructure such as consumer broadband, new and emerging opportunities continue to proliferate, such as the direct to device smartphone opportunity.

Non-GEO will experience the largest growth over the coming decade. Commercial mobility will expand over the early half of the decade, as the impact of 5G and other network management technologies expands across the market. Enterprise data also shows strong uptake of demand, driven by social inclusion and overall universal coverage initiatives. Consumer broadband will contain the greatest amount of data volume for Non-GEO, as more households look towards improving their connectivity experience. Yet, it is not all sunshine for anyone within the Non-GEO market or thinking of embarking into the Non-GEO market. There are challenges.

One of these challenges is oversupply, especially when it comes to the second generation of LEO constellations. Knowing this may encourage less traditional markets to take advantage of their capabilities. Other issues that Non-GEO market will encounter is the lack of ground infrastructure on offer to end-users. Flat Panel Antennas are addressing this lack of ground infrastructure, with its technical complexity, but have their own challenges within the supply chain, power consumption, and the cost of product compared to its rival (parabolic antenna). All combined, these factors will slow down adoption of Non-GEO services from end-users.

The Bottom Line

SATCOM will continue to utilise GEO as it continues to adapt to changing market conditions. Software-defined GEOs, Small GEOs, cloud technologies and adaptive beams, amongst other innovations, will help drive overall GEO-based data volumes. As SATCOM data volumes increase through ’21 to ’31, Non-GEO, and GEO will use different techniques to gain the most efficient use their on-orbit resources to maximize the amount of data traffic. However, more investment needs to be provided for customers to truly utilise these advancements on the ground. Ground segment and consumer equipment terminals will continue to require investments in both R&D and productization. Non-GEO financing and business models are not fully settled, and terrestrial competition will continue to move into rural areas against satellite-based consumer broadband plays.