Satcom Reality Check

The satcom industry is going through turbulent times. A wave of high-level bankruptcies, layoffs, cost-cutting measures and investment deferrals have rattled the industry. COVID-19 obviously places significant pressure in an already challenged ecosystem, hitting key areas of Satcom growth like Mobility. But putting aside the panic around COVID-19 for a moment, it is clear the business fundamentals for Satcom remain very solid. The actors that play their cards well will be able to capture double-digit growth once we reach the “new normal”.

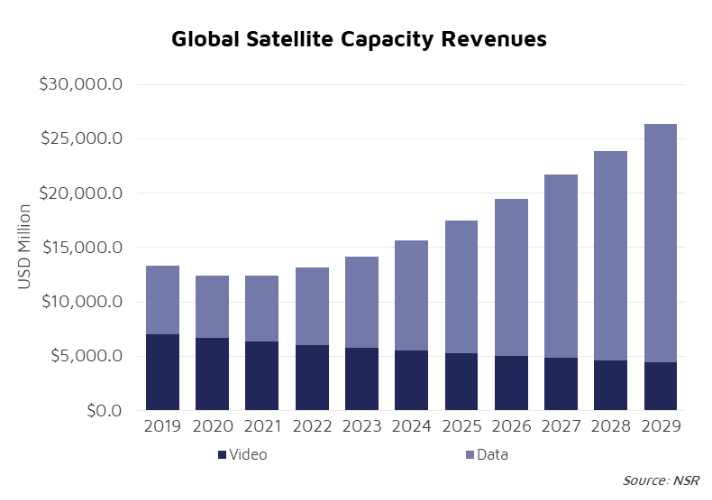

COVID-19 is having a major impact in Satcom, and the recovery won’t be immediate. According to NSR’s Global Satellite Capacity Supply and Demand, 17th Edition report, revenues will dip at 7% and will need 3+ years to recover to 2019’s levels. Having said that, the underlying opportunity continues to be exceptional with revenues forecasted to grow at double-digit rates in the 2023-2029 period.

COVID-19 Hitting the Industry…

Some areas of the business will suffer severe readjustments in this period. Aero is probably the most impacted for the next 18-24 months with big portions of fleets being grounded. Maritime is slightly less impacted with some segments like Merchant or Fishing still sustaining a large active base. Cruise is surely impacted, and it is still uncertain how the market will recover. Video revenues will continue degrading, although this cannot be associated with COVID-19 and is dependent on pressure from OTT platforms and degradation of capacity prices.

On the other side of the coin, fixed broadband applications show high levels of resiliency. Consumer Broadband and Backhaul show similar dynamics. The installed base has seen bandwidth requirements grow, leading to a migration to premium plans. However, new installs have been put on hold due to supply chain challenges and lockdowns.

…but It Shouldn’t Bear All the Blame

The blunt truth is that if COVID-19 hadn’t happened, the short-term perspective for the industry would look challenging. Traditional operators had a slow 2019 with most of the actors seeing stagnant to negative revenue growth. Data-verticals were unable to compensate for the losses in Video, which was starting to show worrying symptoms of saturation with continued pressure on pricing added to the mix.

A wave of bankruptcies shocked the industry, many times using COVID-19 as an alibi. But the truth is that all these developments were generally bound to occur, and COVID-19 may have just provided the extra boost for the industry or the market to clean house:

- OneWeb has launched satellites and raised capital but well below full constellation level and full funding status. The business case continues to be questionable, and key elements of the technology mix such as consumer-terminals are unresolved yet.

- Speedcast grew too fast, paid too much for certain acquisitions, and did not integrate companies under its M&A plan well. The company has also been struggling financially for some time.

- Intelsat is overleveraged and it has been on the verge of bankruptcy for years. Unmet expectations in C-Band repurposing and COVID-19 were just the last straws.

- Phasor simply has no product, so it is no surprise that investors pulled out.

- Other steps of the value chain may see further M&A activity such as service providers in the IFC business as mentioned by Gogo in its recent quarterly call.

- For the rest of the field, there are just too many emerging space companies for the market to bear, and this circumstance will continue such that the exit parade is not over yet.

Business Fundamentals Promise Rapid Growth

Industry-wide and looking beyond bankruptcies from a handful of companies, the good news is that the business fundamentals and the addressable market still show great promise for the Satcom industry. While Aero is one of the hardest-hit segments, post-2022 NSR expects it to resume the fast-growth path it followed before the pandemic. Consolidation of the free-service model and continued growth in penetration will act as market catalyzers. In the Maritime market, the transition to Broadband is unstoppable, creating sustained growth.

In Backhaul, the convergence of cheaper capacity, high performing ground systems and Smallcells allow MNOs to close the business case, triggering extraordinary elasticities that will take 4G (and eventually 5G) to the most remote and underserved locations of the globe. Similarly, Consumer Broadband shows a massive addressable market. Again, cheaper capacity and new business models like Wi-Fi hotspots will unlock large Greenfield markets.

Bottom Line

Satcom cannot escape the impact from COVID-19, and the next 2-3 years will be difficult for the industry. Key growth segments like Aero stalled, and others like Backhaul saw the growth curve interrupted.

It is easy to panic with the recent wave of bankruptcies, usually blaming COVID-19, but the truth is that many of these developments have been simmering for a while now, and the pandemic was the last straw on already challenged balance sheets.

Despite the current overarching pessimism, NSR still sees great long-term value in the Satcom industry. New technologies such as FPA, 5G, SD-WAN matched with more cost-effective infrastructure like flexible satellites or performing ground segment together with new business models like managed services set the conditions for the industry to capture a portion of the extraordinarily large addressable market in segments like Mobility, Backhaul and Consumer Broadband.

Noteworthy is that even bankrupt companies, specifically OneWeb, generated huge levels of interest to rescue the project with hundreds of USD millions from the likes of the U.K.-government-lead consortium just weeks after going into Chapter 11 and well within the time of COVID-19. This signals renewed interest in the preservation of technology, support for innovation and underscores the unique value the satellite industry brings to the marketplace.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.