Satellite Data Commoditization: Are We There Yet?

“Everything happens somewhere” has long served as an epithet in the geospatial industry, from the brand reposition of a 275-year-old mapping agency to the regular campaigns of international geospatial events. The downstream satellite big data industry has often prided itself on the ubiquity and importance of location data, a USP for large scale geo-intelligence, in particular as a foundational layer for insights into remote, mobile and globally distributed assets.

With 100s of Earth Observation and M2M/IoT communication satellites being launched in the coming years, data supply does not appear to be as much of a problem as data accessibility is. The market is far from moving beyond its few legacy customers, i.e., large commercial entities and long-standing government/military/institutional users, with deep pockets. True commoditization of satellite big data will take much longer.

Over the years, multiple startups have risen to try and break into the satellite big data ecosystem, promising to break down the high barriers to entry, but in most cases, failed to deliver. This has been a question of both demand and cost: a small addressable market willing to pay a premium for derived insights, and the prohibitive costs of data and compute resources at scale.

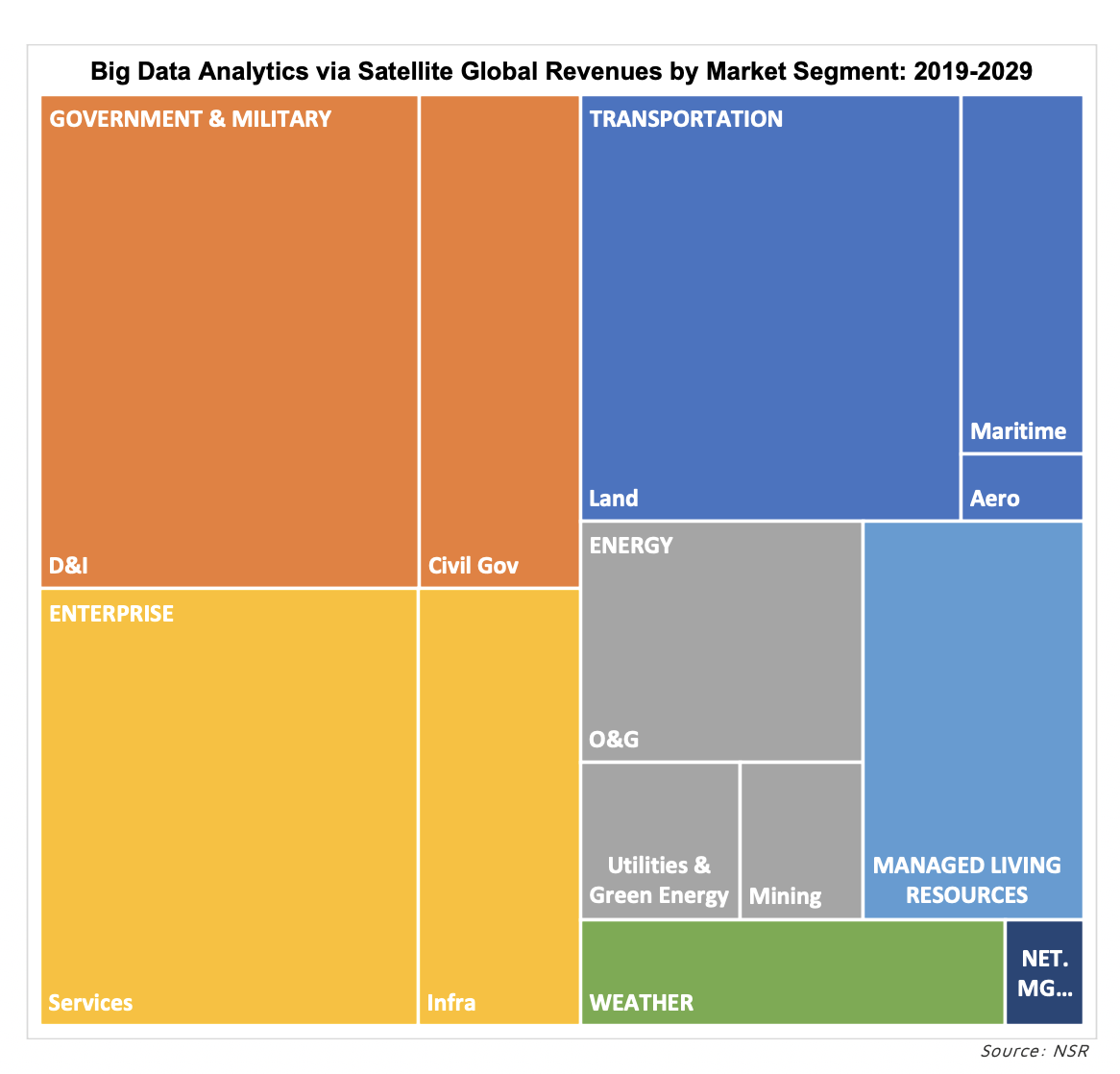

NSR’s Big Data Analytics via Satellite, 4th Edition research report presents the global revenue opportunity for downstream satellite big data, and much like the EO data market, it shows this is primarily driven by the government and military customers who are able to absorb expensive data costs and provide long-term business contracts.

Satellite players have taken to innovations in software defined networking and virtualized ground stations, paving the way for interoperable systems that might one day be well-positioned to leverage satellite big data. However, the need for end-customer education and prohibitively expensive data constrains this market from growing too fast. Users care for tools and insights that dovetail into their existing workflow and decision-making process, and/or improve their bottom line, either by performance or cost reductions (in terms of price and time). And for that to happen, data costs need to come down.

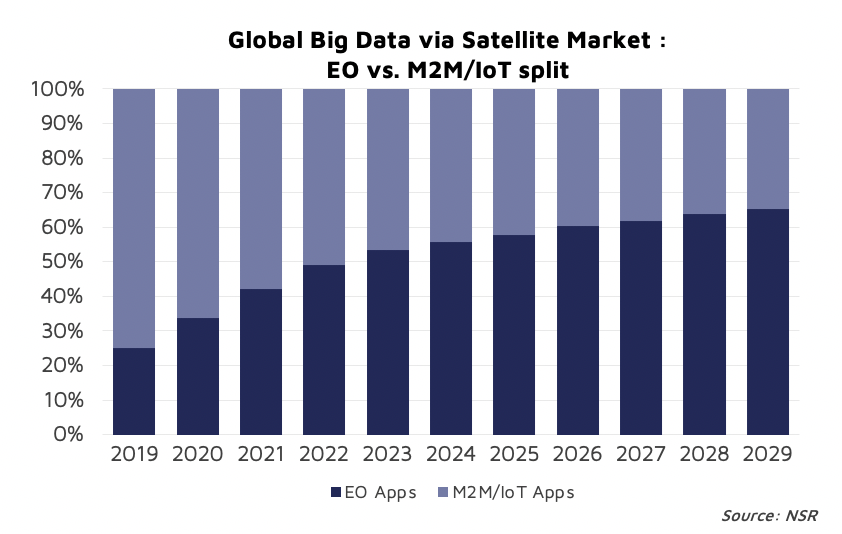

While the M2M/IoT Satcom-based market is comprised of traditional customers and operators (particularly in the transportation vertical), the current wave of Newspace IoT constellations make up for only a small portion of the revenue opportunity, primarily owing to the low-cost use cases of IoT satcom. For this market, NSR forecasts a revenue opportunity of $1.2 billion by 2029, at a CAGR of 8.3%.

Meanwhile, there is no dearth of data coming into the EO industry. However, a lack of standardization in the industry is a key bottleneck in driving prices lower if the industry is to move towards a “global satellite data stream” and high-volume purchases. NSR forecasts this segment to grow at a high 28.7% CAGR over the coming decade.

The commercial satellite data market is heavily fragmented and broken, with multiple providers/satellite operators, multiple platforms and applications, multiple APIs and a complex web of pricing schemes. Given such complexities, the pricing model in the downstream analytics sector continues to remain obscure. The presence of all these factors has given rise to newer business models, in the form of platform services and data marketplaces, which hope to serve as a bridge between the upstream and downstream sectors.

The Bottom Line

Years into the rise of next-generation machine learning applications over satellite imagery and complex cloud infrastructure services, the market for satellite big data, while growing, is not yet mature and is far from being commoditized.

Increasingly though, the demarcation lines across the industry are becoming blurred, as data providers (satellite operators) roll out new analytics products, or analytics providers push for data ownership and move up the value chain.

Market consolidation has already begun, and is expected to continue, especially as vertical-specific incumbents adapt to geospatial technologies in their business decisions. Platform solutions and marketplaces might fill a void in the interim, marching towards easier access to satellite data and decreased costs. However, commoditization as promised will hinge on the development of standards across providers.