Satellites in the Cloud

Earlier this year, Amazon activated services on two of its ground stations, bringing to bear the cloud computing capabilities of Amazon Web Services (AWS) through the new AWS Ground Station venture, leveraging Lockheed Martin’s network of Verge antenna systems. This is but one solution expected to ease the data downlink bottleneck, even as the deluge of geospatial data continues its steady rise. Meanwhile, IBM (in partnership with Cloud Constellation) published a report on the evolution of data architectures and data security, detailing a move beyond traditional cloud services into storage on space-based assets. The satellite industry poses interesting use cases and opportunity for cloud adoption, and mainstream Cloud Service Providers (CSPs) are beginning to take note.

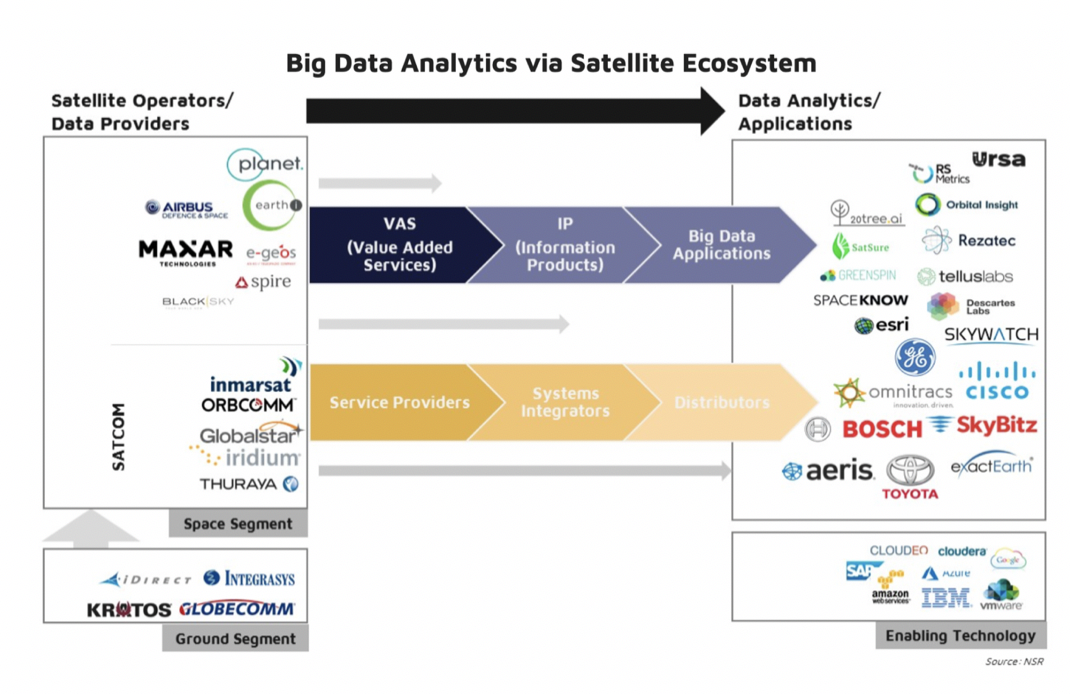

NSR’s Big Data Analytics via Satellite, 3rd Edition report identified the cumulative revenue opportunity for satellite big data to be nearly $17.7 billion by 2028, much of this driven by the growing interest in satellite-imagery based geospatial analytics and IoT sensor-based applications. A quick look at the satellite big data ecosystem reveals what might be obvious to industry insiders: cloud services form the bulk of the enabling technologies driving this industry forward.

New entrants in the Earth Observation (EO) markets are driving the supply of space-based sensor data: in today’s world of a continuous supply of satellite imagery, tasking a satellite for specific imaging requirements (single scenes) is becoming an archaic method: deriving actionable insights from a growing repository of high resolution, high revisit satellite data (whether historical or current) is becoming more prevalent. This is an industry in transition: Planet, for instance, historically focused on imaging the Earth acting as a data provider. In mid-2018, the company made a strategic shift towards boosting its analytics offerings, building on top of data stored on a variety of cloud services.

Running data analytics offerings on virtual systems has many benefits: information and insight extraction for end-users becomes much less expensive, and the focus moves away from building the underlying infrastructure to dealing with the influx of big data and solving actual problems. By capitalizing on the scalability and ubiquity of cloud computing platforms, satellite data analytics solutions are that much easier to deploy, thereby accelerating adoption.

The importance of Amazon in the satellite industry runs much deeper than the proposed ground stations: a number of downstream geospatial analytics firms use AWS for storage and compute, and the lower CAPEX required only helps to further decrease the barrier to entry. Moreover, Descartes Labs, a leading geospatial analytics provider, built one of the fastest high performance computing platforms this year, running it completely on virtualized AWS cloud resources.

Meanwhile, digitalization is fast taking over many historically intransigent industries: this is particularly true of the energy and maritime sectors, both of which rely heavily on satellite services for remote communications. The IoT revolution has seeped into this world, driving further demand for connectivity and advanced analytics, and satcom managed services will be a key enabler here: Iridium CloudConnect is one solution expected to meet this demand.

On the other hand, there is increasing user demand for bandwidth-intensive applications delivered over the cloud, from video streaming services to mobile applications. Satellite network operators and service providers looking to improve their bandwidth delivery services to meet this demand also look to cloud technologies for answers: dynamic Software Defined Wide Area Networking (SD-WAN) solutions that allow for real-time network optimization can be understood in terms of the virtualization seen in the cloud computing world. The industry is thus catching up in its adoption of the cloud: SpeedCast recently announced its Advanced Partner status with the AWS Partner Network, becoming the first satellite service provider to do so. Earlier, SES Networks announced a collaboration with IBM, aimed at delivering satellite services to IBM Cloud customers globally. And the ground segment is not far behind. Kratos introduced cloud-enabled ground systems to help customers further their virtual operations strategies.

The Bottom Line

The cloud has gradually made its mark in the satellite sector over the past decade, beginning with the delivery of cloud-based applications to remote locations via satellite. With newer constellations in LEO and MEO expected to make latency much less of an Achilles’ Heel for satcom, fully-managed satcom services are on the rise.

Regardless of application, cloud computing will reduce the barrier of entry to market for new startups in the satellite industry. Different CSP delivery models each have their own pros and cons. However, the advantages of incorporating the cloud into satellite businesses are clear, whether in EO or satellite network operations: a reduction of upfront capital, reduced operational costs, rapid scalability, ease of development and ubiquitous accessibility.