Scaling VSAT Platforms through M&A

M&A activity in the VSAT platform segment has been very dynamic in the last several months. After iDirect/Newtec fired the starting gun, Comtech conducted a series of acquisitions including UHP and Gilat. This consolidation rush seems natural given the current technology and market trends and was anticipated by NSR long ago. With the satcom industry at the verge of profoundly transforming events (NGSOs, 5G, New markets, Cloud, etc.), what are the implications of these mergers?

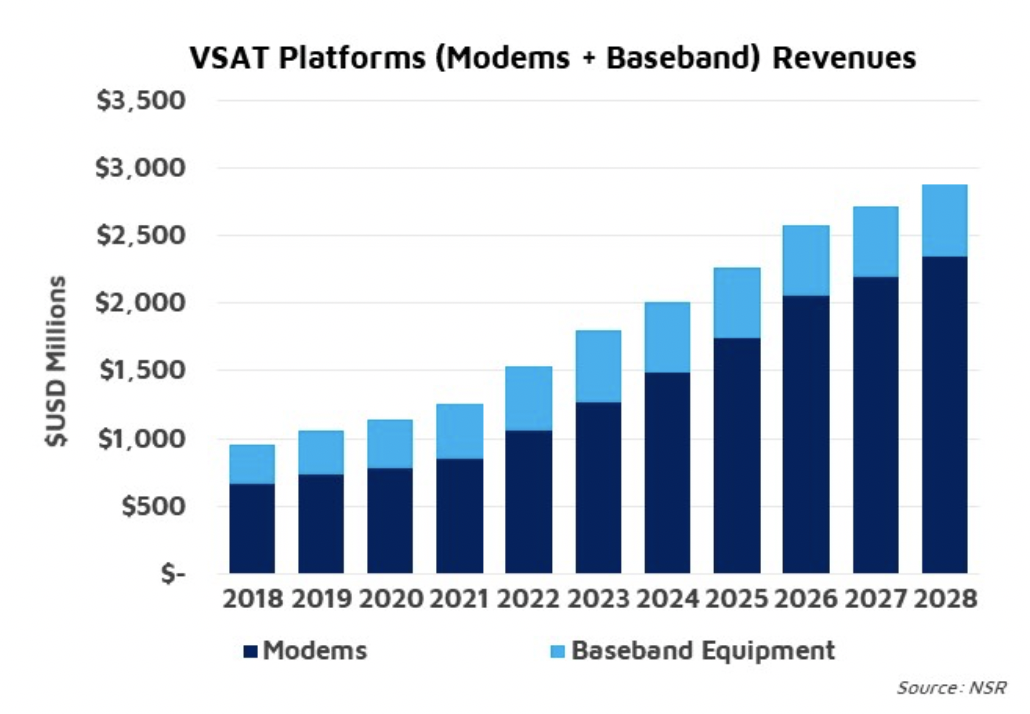

VSAT platforms will experience extraordinary growth in the coming years as the satcom industry moves from video to data verticals. In fact, NSR’s Commercial Satellite Ground Segment, 4th Edition report forecasts VSAT platform revenues will triple in the next 10 years. However, staying competitive in this market won’t be easy as the industry is putting a lot of pressure on equipment vendors in terms of technology development, business model evolution and price competition, prompting this wave of consolidation.

Scale is the New Name of the Game

Satellite networks are reaching new levels of complexity. From a business strategy point of view, managed services are now a key offering for satellite operators. With the aim to simplify their operations, it is now common to see a single VSAT platform per HTS payload; meaning there are fewer, albeit larger, deals for equipment vendors. Furthermore, given the large CAPEX required to set up the ground segment (with the consequent potential win for the equipment supplier), some operators are starting to pressure vendors to take a bigger share of the risk. Business models are transitioning from just selling equipment to having more skin in the game with equipment leases or even network operation and revenue share. While these models can potentially offer better margins, they require adequate scale and financial health of the equipment vendor.

From a technology point of view, VSAT platforms need to respond to new sophisticated requirements such as a multiplying number of beams, skyrocketing throughputs, networking requirements, etc. This translates into heavy investments in R&D that are sometimes difficult to amortize if scale is insufficient. As a reference, both Comtech and Gilat invest about 10% of their annual revenues in R&D.

Technology Convergence

The same VSAT platform is now required to serve a wide array of use cases. This is probably one of the key triggers for the latest acquisitions. Comtech has traditionally been the dominant actor in high-end segments, but they experienced challenges when customers wanted to serve multiple use cases, for example a telco selecting a platform for backhaul but also willing to capture the SME/SOHO business. Actually, there are multiple backhaul deployments concurrently using Gilat for the high-contention sites and Comtech for the most bandwidth-hungry stations.

The logic in the iDirect/Newtec merger is similar. The throughput requirements outpaced TDMA performance capabilities in many use cases, and iDirect was pushed to incorporate new technologies to serve the most demanding sites. In fact, NSR anticipated the SCPC-TDMA convergence where the waveform of the return channel changes depending on the traffic profile.

Positioning for Growth

Access to key growth segments was undoubtedly a major factor in the recent M&A moves. Despite having a solution that could technically work very well in the aero space, given the barriers to entry, Comtech (VSAT platform) couldn’t penetrate the market. Gilat’s acquisition sets Comtech in a strong position to capture a portion of the fast growth in the vertical. Even in backhaul, where Comtech continued to lead, the fastest growth is coming from the low-end, where Gilat played very strongly and was eroding Comtech’s market share. Similarly, iDirect’s leading market share position in mobility markets was being attacked by Newtec (Panasonic, Telenor). Furthermore, iDirect gains access to new markets like video broadcast or high-throughput trunking modems (that can also be used in high-end mobility markets like cruise ships).

Regionally speaking, there are also important synergies with Gilat’s strong position in emerging markets like China or India, but Comtech also offers an easier access to markets in MENA, SEA or even the U.S. Government.

Not a Risk-Free Move

While NSR generally values these mergers positively, the moves are not free of risk. There is a certain level of uncertainty among customers on how these mergers will impact their own operations in terms of support of legacy networks. Also, the long-term goal will presumably be having a common technology platform, which won’t be an easy transition.

Furthermore, there are very different cultures in each company and aligning them into a common vision could be difficult. Gilat has repeatedly surprised the industry by its ability to take risk in aggressive business models and deals (managed services, revenue share, etc.), while Comtech continues to take a cautious position on the newest trends (Smallcells, etc.).

What is Next?

There are still many boutique vendors that will continue to feel pressure in the market given the current industry concentration. NSR wouldn’t be surprised if there are more similar deals announced in the short term.

Interestingly, the transition towards software defined satellites and virtual ground segment is pushing some actors to try to design space segment and ground segment in parallel. ViaSat-3 or the efforts from Thales Alenia Space to develop its own ground segment platform are examples of this. Perhaps the next step in this wave of M&A is towards incorporating adjacent steps of the value chain to offer an integral solution. One must not forget that Comtech already plays strongly in the RF Chain segment, and Gilat’s Wavestream subsidiary is also a big contributor to the company’s growth. Furthermore, Gilat continues investing in its ESA antenna, and beyond UHP and Gilat, Comtech also acquired CGC Technology, a company developing antenna products.

Bottom Line

NSR generally sees recent M&A activity in the VSAT space as encouraging. The new entities will have stronger muscle to accelerate technology developments needed to respond to the new requirements of 5G, NGSOs or VHTS.

This is a natural move given the transition towards fewer (and larger) equipment deals, emerging business models and heavy investments in R&D. Furthermore, the need to accommodate a wide array of use cases in a single platform also favors this M&A process. It is no coincidence that the two largest deals involved an actor focused on the high-end merging with an actor capturing business mostly from the low-end.

While digesting these mergers will take time and will experience challenges (cultural differences, technology alignment, etc.), NSR believes there is still room for further consolidation. But, this time it might involve a step towards adjacent stages of the value chain.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.