Shifting Satellite Operator Financials

NSR’s Satellite Industry’s Financial Analysis, 10th Edition (SIFA10) report provides an in-depth assessment of the global satcom industry, analyzing critical financial, strategic, and competitive outlook of satellite operators and service providers across multiple metrics.

The satcom industry continues to witness mixed financial results, with non-video revenues growing across multiple verticals, while the video business maintains its downward trend. Below is a peek into revenue growth trends across a broader spectrum of video vs. non-video, lease vs. service, and trends in vertical markets for the 2019/20 financial years.

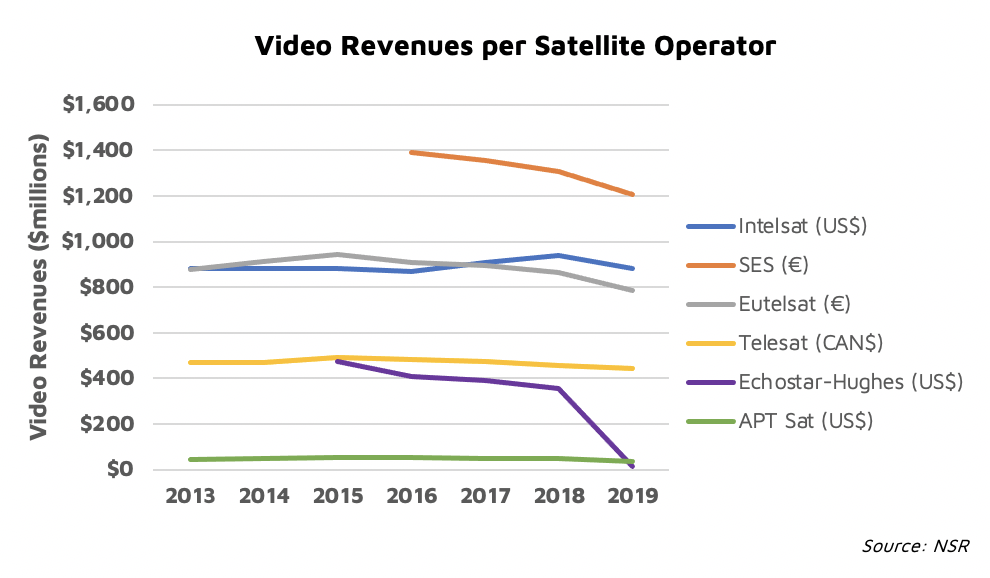

Video Revenue of Top Six Operators Contracts by 15.1%

Video (including DTH and Video Distribution) revenue continued to slow massively, contracting by 15.1% cumulatively in 2019 YoY for the top six operators analyzed. European hotspots remain under stress as SES and Eutelsat continue to face challenges in declining hotspot prices. 2019 witnessed a further decline in cumulative video revenue figures as Hughes sold its video business, the ESS division, to DISH Network internally under the same parent company to consolidate prices as Pay-TV headwinds continue in the US.

Satellite operators are experimenting with price, de-commoditizing offerings, aggressively pursuing new markets in Africa, Asia, and Latin America, and acquiring critical hotspot positions to reverse declining revenue trends for the video segment. However, video headwinds arising from the shift in advertising revenues to social media and Internet platforms have not changed to warrant a reversal of trend. The situation is exacerbated by pressure from OTT providers such as Netflix and traditional broadcasters now giving equal or more importance to OTT revenues, following a shift in advertising.

Looking forward, NSR expects video revenue to improve slightly on the back of reduced price pressure, market consolidation and the growing demand for High Definition (HD) and Ultra-High Definition (UHD) channels.

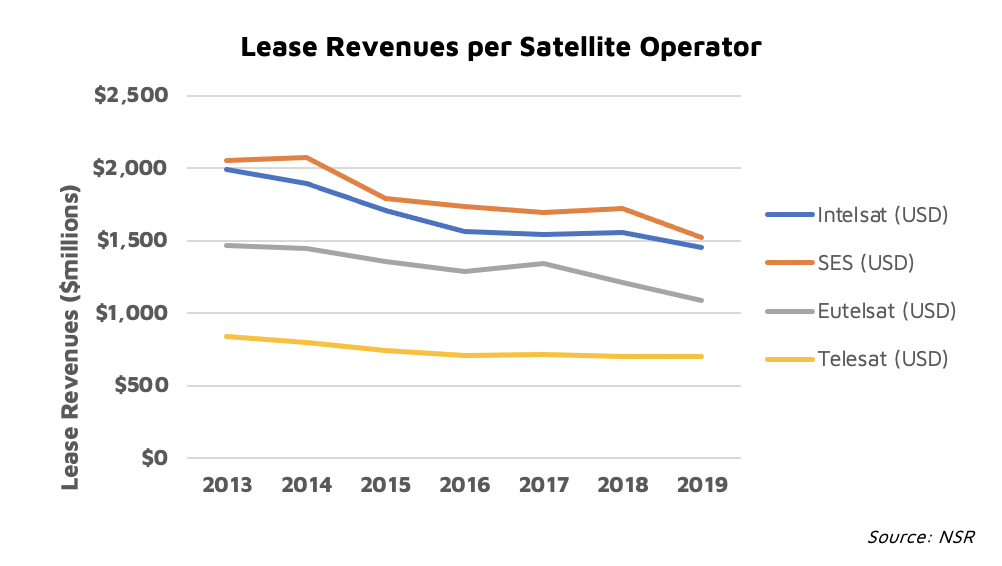

Service Revenues Continue to Grow at the Expense of Lease Revenue

A critical analysis of lease vs. service revenue trends reveals the operator vs. service provider business model’s changing dynamics, with average growth representing the market tailwinds for each model. Lease revenues have declined at a moving average of -3.6% over the last seven years, while service revenues have increased YoY at 6.7% across operators and service providers.

As might be expected, dwindling video revenue and price erosion for fixed data drag lease revenue performance for the big 4 operators. The impact is that operators continue to see reasons to move closer to consumers, further contributing to service revenues growth and vertical consolidation.

However, service revenue growth did not come cheap as a significant portion is driven inorganically at high customer acquisition cost. Service revenue growth comes at a substantial loss of EBITDA. Despite expanding revenue significantly, Speedcast and GEE filed for bankruptcy in 2020 due to low cash availability and no viable means of external funding at a high Net Debt to EBITDA ratio.

Integrated operators such as Hughes, ViaSat and Inmarsat have managed to find a balance between lease and service business, outperforming operators on revenue growth and beating SPs on EBITDA. Hughes, ViaSat and Inmarsat reported an average of 9% increase YoY in service revenues, driven mainly by broadband and aero business. Hughes sold its ESS division to focus its broadband and network business.

The Bottom Line

As every operator strategizes to move closer to consumers, NSR expects service providers bargaining power to dwindle, thus providing some buffer for wholesale prices to stabilize. Operators will be forced to optimize offerings and integrate added value such as distribution efficiency, cloud etc., rather than compete on price. Channel and transponder upgrades, enabling delivery of content over HD and UHD, will drive the next wave of growth for video. However, video will most likely stabilize, posing a slight improvement on price and revenue uptick.

The industry is set to witness the expansion of service revenue, driven not only by the consolidation of existing operators/SPs but also by the market entry of new satellite operators and SPs. Non-GEO constellation operators pose competition in Gov/Mil, mobility and consumer broadband verticals, further pushing legacy GEO operators downstream, thus expanding service revenue lines. The implication is that the market’s overall size will expand significantly as new technologies and business models will unlock value in non-traditional satellite-enabled sectors, and further deepen application use cases in existing markets.

NSR expects high growth to continue in backhaul, trunking, Gov/Mil and VSAT verticals as Non-GEO and HTS systems unlock more value for telecom and government customers. Mobility is expected to rebound post COVID-19, with maritime recovering in late 2021/2022 and aero fully bouncing back in 2022.

###

NSR supports satellite operators, service providers, investors, financial institution, government entities and other corporates in their technology, investment, and business strategy assessment and planning. Please contact info@nsr.com for more information.