Taking Risks to Stimulate Backhaul Demand

Backhaul is poised to be a key driver for satellite industry growth. The combination of advanced ground segment technology and competitive capacity pricing makes satellite a compelling solution for MNOs to expand coverage. However, take up is still slow. What business models should the satellite industry therefore adopt to stimulate demand in Cellular Backhaul?

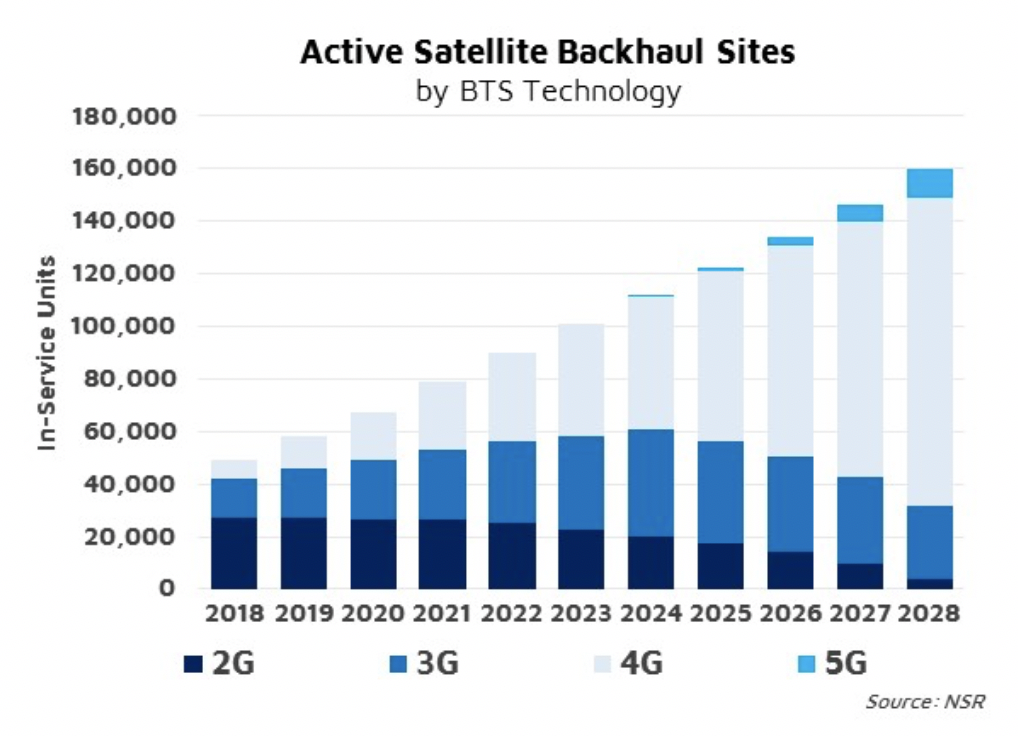

With today’s technologies and capacity price points, satcom is the most cost-effective option for MNOs to expand coverage when there is no direct line of sight with a terrestrial node. This will create enormous traction for this vertical and, according to NSR’s Wireless Backhaul and 5G via Satellite, 13th Edition report, the installed base will more than triple in the next 10 years. Despite this seemingly optimistic projection, stimulating demand won’t always be easy as MNOs are oftentimes reluctant to incorporate external technologies. Obviously, making it easy for Mobile Operators to adopt satellite, not only from a technology point of view but also operationally and commercially, will be critical to capture growth.

Satellite (Finally) Has a Compelling Product

For years, satellite has been used as a last resort solution by MNOs. It was implemented where there was no possible alternative and most of the time was dictated by regulatory obligations. However, there are multiple elements converging and making satcom much more attractive for MNOs. Ground segment has evolved tremendously, and performance (throughput, QoE) is now on par with terrestrial alternatives. In parallel, satellite capacity pricing dropped as HTS became prevalent. While this certainly creates pressure for satellite operators to grow revenues in the short term, this is key to unlocking the potential for cellular backhaul. At the same time, the addressable market is massive, as there are large portions of the population still unconnected, in Sub-Saharan Africa for example, 40% of the people live outside any broadband coverage.

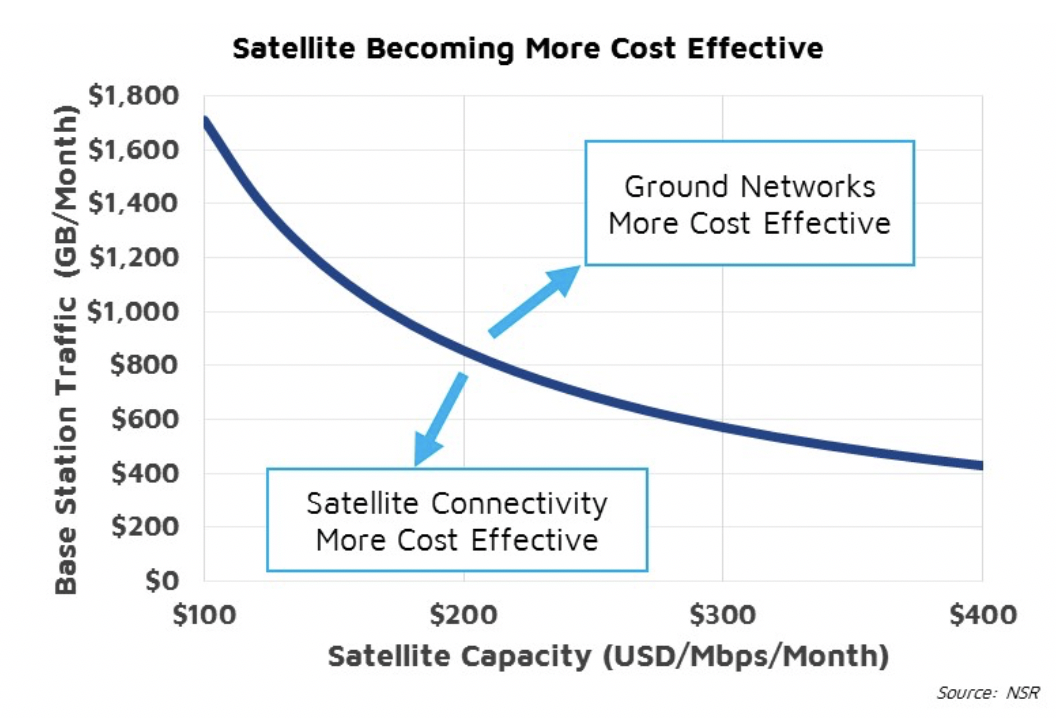

Under these conditions, satcom is finally a viable option to commercially expand network coverage, without having to rely on government sponsorship. Assuming a BTS 20 km away from the closest backbone node and satellite capacity pricing at $300 USD/Mbps/month, satellite is the most cost-effective solution if the station consumes under 600 GB/month. To add a bit of context, the average plan in Sub-Saharan Africa consumes 0.6 GB/month, so a new station supporting less than 1,000 subscribers would be most cost-effectively backhauled via satellite.

Understanding MNOs’ Perspective

Despite these renewed capabilities from the satellite industry, the market is still taking time to react. Outdated perceptions are still playing against satcom and educating MNOs on the new attributes of satellite backhaul will take time and effort. Furthermore, one must not forget that MNOs extract most of their profits from urban areas, and consequently they optimize their organization to serve those customers.

When a satellite actor pitches a rural deployment to an MNO, aversion to change is one of the biggest barriers. For the commercial department, an additional site in a rural location might not move the needle for their sales targets, and most of their efforts are centered on marketing for urban areas. Similarly, the operations department usually likes to work with standardized products that do not add complexity to managing their network. They might not have the know-how to run satellite networks or it might be an under-resourced team generally operating outside of the core of the business. All in all, it is very difficult for satcom to break into those organizations, which oftentimes leads to underserved rural areas with consequently missed opportunities.

Making Satellite Very Easy to Adopt

On the other hand, MNOs do need to continue adding subscribers and new sources of revenue. They might not be willing to risk CAPEX on those deployments, but there is a growing trend among MNOs to externalize non-core capabilities. A case in point, Telefónica recently spun-out its rural network in Perú coinvesting with Facebook, BID Invest and CAF to create an open wholesale rural network to accelerate rural coverage. If satellite can articulate an attractive solution that is easy to adopt by MNOs that helps them expand into rural areas, growth will be exceptional.

In this sense, managed services are the perfect match between satcom’s streamlined operations for rural areas and MNOs’ need to profitably expand coverage. And here, there is no one-size-fits-all solution. From simply managing the link, to offering an OPEX-model where the satellite integrator offers a turnkey solution including the management of the base station, or even going down to revenue sharing schemes where the integrator and the MNO cooperate in subscriber acquisition, the spectrum of business models is wide. Ultimately, all depends on the needs of the MNO and the willingness to take risks by the satellite integrator.

Bottom Line

The satellite industry will capture sizable growth from Cellular Backhaul; this is a certainty. This growth is based on advanced ground segment technology and competitively priced capacity converging to create a very attractive alternative for MNOs to expand coverage into rural areas.

However, MNOs still perceive satcom as an expensive and difficult to implement solution. The industry as a whole needs to try to educate MNOs on the new capabilities and create solutions that are easy to adopt by MNOs.

Managed services are the perfect match between satcom’s renewed capabilities and MNOs need to continually expand broadband coverage. While satcom will need to incur bigger risks (investing in CAPEX, participating in subscriber acquisition), the reward is promising with a huge addressable market waiting to get online.

NSR supports equipment vendors, service providers, satellite operators, end-users and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.