Taking Risks to Stimulate Satcom Growth

Global satcom capacity revenues continue to evolve at low single-digit rates scoring 2% growth last year. Obviously, data is becoming the star for revenue growth and operators with higher exposure to video and legacy FSS capacity are more prone to turbulence. But, in these transformative times in which raw capacity is commoditizing, operators must rethink their business models and take more responsibility of the value chain to both stimulate demand and capture higher portions of value.

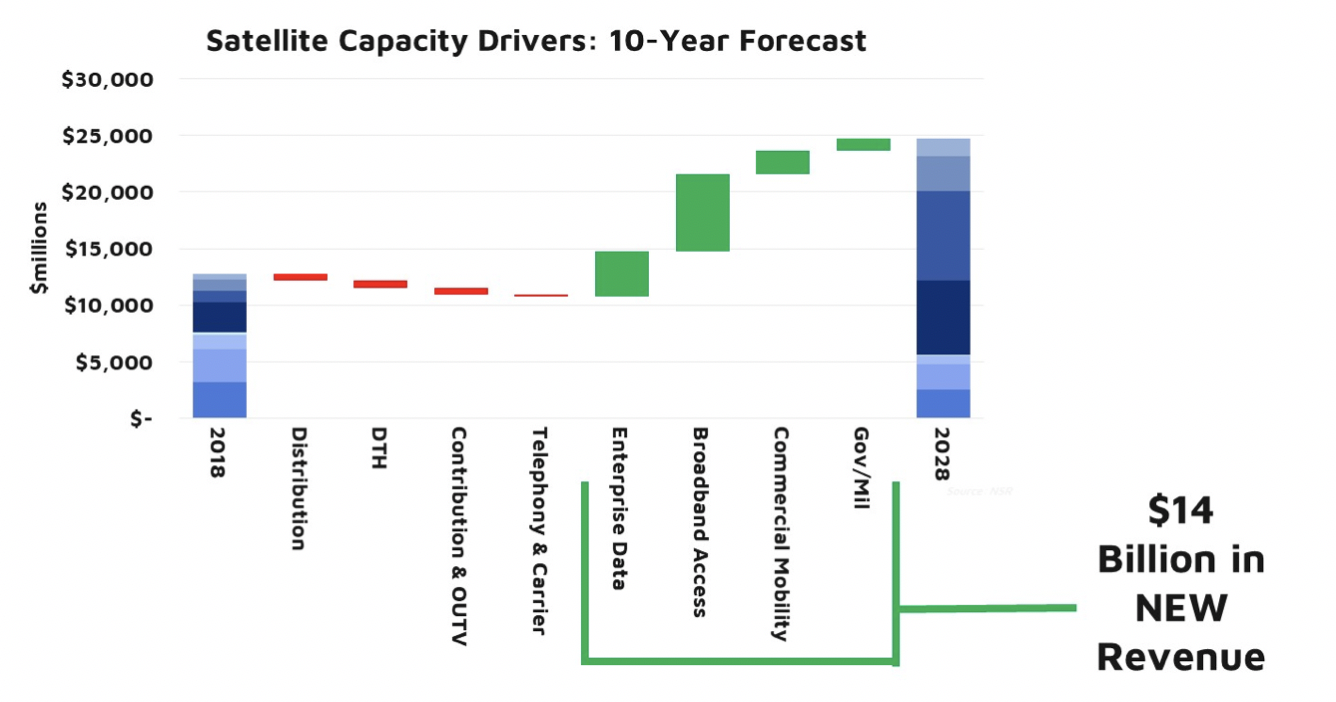

While the industry today is still facing difficulties in finding the path for growth, NSR is optimistic on the long-term prospects. According to NSR’s Global Satellite Capacity Supply and Demand, 16th Edition report, capacity revenues will grow at 6.8% CAGR over the next 10 years. However, to capture revenues, operators will need to get closer to end-users. Unlike in the past where satellite operators’ main focus was on managing its space infrastructure, today that is taken for granted and the differentiator will come from better understanding and responding to end customer needs, even indirectly.

The “Real Estate” Model Isn’t Driving Growth Anymore

For years, video was the foundation of the satcom business. While DTH and Video Distribution have driven extraordinary growth and generous margins, it also built some disconnection between the industry and end-users. Operators generally engaged in wholesale deals where their primary focus was to create hotspot positions for video. Even in data markets, operators were usually several steps away from the end user. Furthermore, the broadcasting advantage of satellite was so prevalent that there was little incentive in technology evolution.

During the heydays of video, these challenges didn’t worry the industry as growth continued at very healthy margins from premium video positions. However, factors such as market saturation or OTT are putting pressure on video revenues. In parallel, the arrival of HTS and greater levels of competition are commoditizing bandwidth for data services. All in all, operators don’t have any other option but to stimulate new sources of demand and climb to higher layers of value creation if they don’t want to exhaust their margins.

New Layers of Value Creation

Operators need to find new ways to differentiate now that value is moving from assets to networks. This is very clear in applications like Cellular Backhaul, where operators are starting to take bigger risks co-investing in rural Mobile Network deployments. On one hand, this has the potential to stimulate new levels of demand as the service is much easier to adopt by potential customers. On the other hand, it creates some lock-in effects for customers while adding new layers of value like network management alleviating the pressure on bandwidth commoditization.

Similarly, mobility is creating opportunities for operators to get closer to final customers. Apart from the global operators, a number of regional players like Thaicom or JSAT have launched services for maritime markets. This does not mean that integrators are put outside of the equation as there are still many specific applications that can add value to the end-customer, but the greater complexities of these kinds of networks facilitate operators taking bigger control over the service.

Balancing Risks, Opportunities and Rewards

The current difficult position for certain satellite operators as they experience rapid revenue degradation invites desperate moves. However, before committing to invest in developing new services, operators need to carefully evaluate the potential for return.

Value added services and closer relation with end-customers need a completely new set of capabilities for satellite operators. Furthermore, scale is critical for many of the new markets like maritime. Additionally, in some emerging models like revenue-sharing (becoming popular in Backhaul and even Mobility), the risk accepted is very high and operators must be very careful in evaluating the opportunities.

Bottom Line

The industry is still immersed in a profound transformation. Revenue growth continues flat but as new verticals like Backhaul, Mobility or Consumer Broadband develop, the industry should see a renewed wave of growth.

Having said that, the business models of the past will experience challenges, and operators need to take greater responsibility of the value chain. This will both help stimulating new demand and keep margins at healthy levels.

From co-investing with Mobile Operators in rural deployments to creating specific solutions for verticals like maritime, the opportunities are varied. With interim CapEx cycles ending, few operators are expected to invest in closed partnerships with equipment providers or create separate service business entities with external investments and fuel growth (like APSATCOM). Though, notwithstanding borderline Net Debt to EBIDTA margin and future vHTS systems plans of multiple operators, investments towards end-user solutions remain a high-risk bet. Operators must build a careful evaluation of risks as the level of organizational transformation required is not trivial and returns are not guaranteed.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.