The Endpoint Drives the Architecture in Mobility SATCOM

Connectivity is not a luxury anymore for mobility markets. Be it terrestrial or satellite – anything that moves frequently needs to be connected. Increase the number of people, the cost of the asset or the criticality of its mission – and the need for connectivity scales exponentially. Put those assets – a car, train, ship or airplane further from terrestrial sources, and they will increasingly turn to satellite-based connectivity.

Connectivity is not a luxury anymore for mobility markets. Be it terrestrial or satellite – anything that moves frequently needs to be connected. Increase the number of people, the cost of the asset or the criticality of its mission – and the need for connectivity scales exponentially. Put those assets – a car, train, ship or airplane further from terrestrial sources, and they will increasingly turn to satellite-based connectivity.

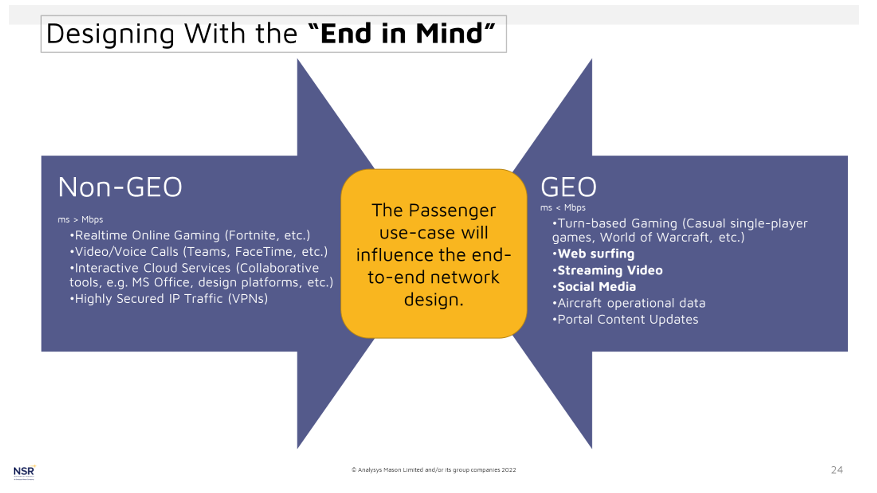

Once there, the choice of ‘which satellite service’ continues to become more complex from a range of orbits (GEO, LEO, MEO?) and architectures (FSS, HTS?), frequencies (C, Ku-, Ka-?) and providers (vertically integrated or “vertically” specialized?). Overall, it is the end-use that influences the architecture choice, not entirely the architecture itself.

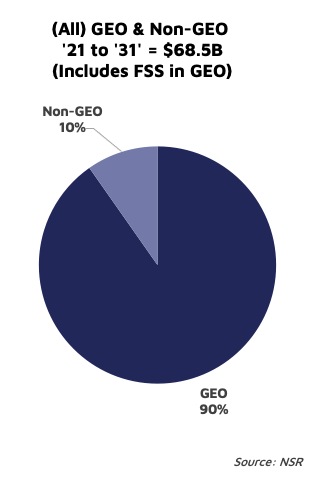

According to NSR’s LEO and MEO Broadband Satellite Markets, GEO-based orbits from any FSS or HTS and C/Ku/Ka-bands will account for 90% of the cumulative $69 Billion opportunity from ’21 to ’31. With Non-GEO starting at 2% of revenues and growing to 18%, challenges abound for these new Non-GEO systems. Look at any Non-GEO solution’s marketing materials though, and one would be hard pressed to find anything except for mobility markets, which starts to ask the question – why so ‘controversially pessimistic’ for the role of Non-GEO?

Chiefly, revenue growth for Non-GEO solutions will be limited by a few key factors:

- Most markets do not start adopting Non-GEO solutions until later in 2023 and start with a slow ramp-up into 2027.

- Pricing competition remains strong, and onboard equipment installed today is likely to remain active well into 2025 in markets such as Aeronautical.

- Land-Mobile is still a niche opportunity, with sporadic revenue generation. While the TAM is ‘huge’, the ability or willingness to pay every month is more challenging to identify.

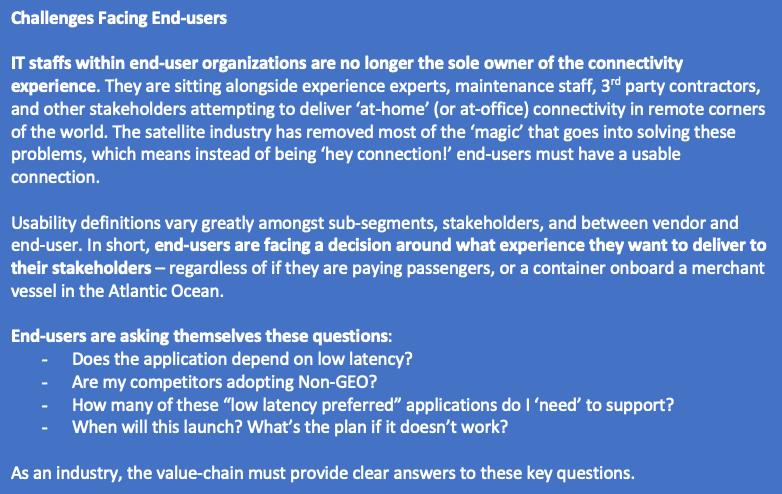

Moreover, End-users themselves are faced with a complex decision matrix around what services and stakeholders they need to support. Increasingly, IT staffs are no longer the sole owner of the connectivity experience. Airplanes are no longer just a place for a few emails or maybe streaming movies – but a co-working location, a maintained and monitored asset, a workplace, and a range of other internal and external use-cases that these networks must support. Furthermore, they must support the economics that can unlock further investment into the connected experience, which continues to be another complex balance of monetization vs. ‘sunk cost’.

Overall, end-users are more frequently designing their networks with the end-use in mind which further drives all of the upstream network and technology choices.

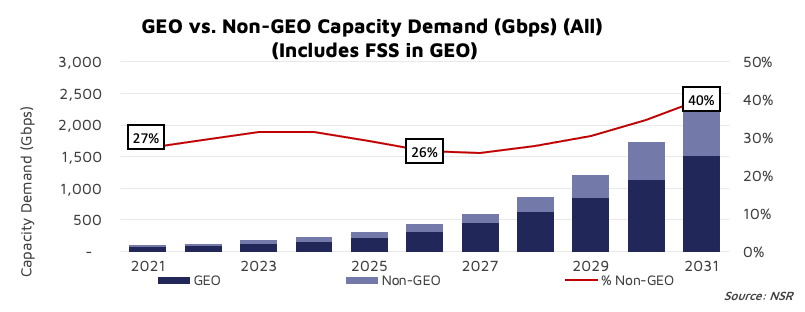

Amongst all those choices – financial vs. performance vs. time-to-market vs. ___, a few trends are clear – more throughput per site will be unlocked over Non-GEO (approaching 40% of total capacity demand by 2031) – and passenger-centric connectivity will be the key driver of that demand. “Connecting the Guest” be it on a plane, train, or ship will continue to be the leading source of connectivity demand for satellite mobility broadband services. These end-uses have the most complex network installations, face the biggest demands on their pipes, and can generally bring ‘the most’ to spend on their connectivity solutions through a mix of monetization and operational improvements.

The Bottom Line

What all of this means is this – Mobility will not be a ‘this or that’ architecture. Non-GEO is a longer-term threat to the GEO value-chain. On a site-by-site level, it is unlikely that in the near term any customer will be willing to go ‘all-in’ on a single-sourced solution to replace a current service. Greenfield opportunities might be the true battle of the orbits, but for now the answer to which service on which endpoint is likely an ‘all of the above’ solution.