The Ground Segment Di(LEO)mma

LEOs are transforming the satellite industry, and the ground segment is no different. While the opportunity for equipment vendors is massive, it is not absent of risks. Non-GEOs will certainly unlock new areas of growth where equipment vendors can capture a portion of the value. However, participating in the NGSO ecosystem requires heavy R&D efforts and an upfront financial commitment, many times with scarce support from the constellations’ sponsors. The dilemma for equipment vendors is then whether to carry the burden of developing the technologies for LEOs or assume the risk of being left behind in the race to serve NGSO constellations.

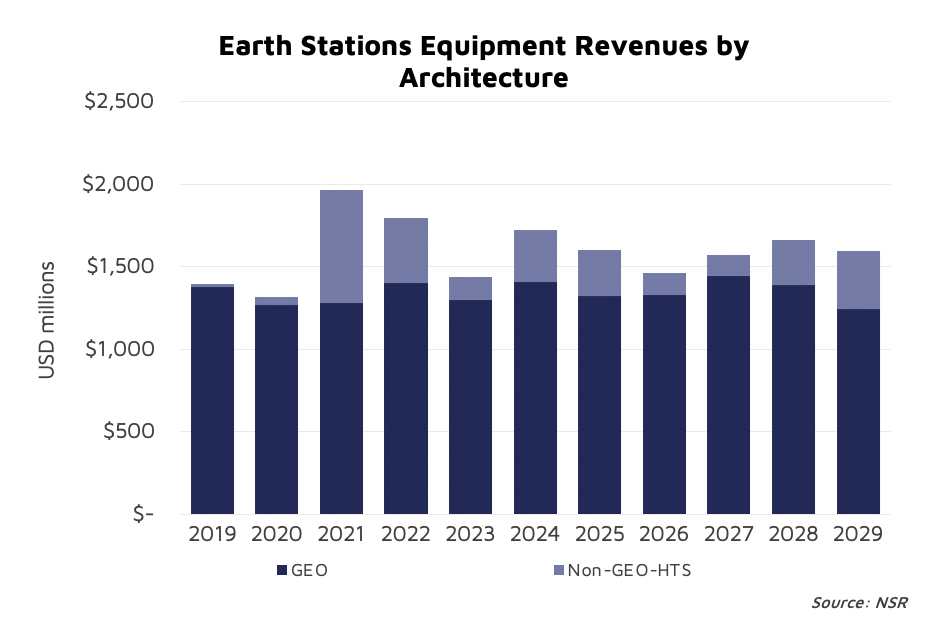

With various constellations having selected satellite manufacturers and even starting to populate these constellations, the next big chasm for them is ground infrastructure. Despite generating significantly less hype than the space segment, this is not a minor topic. In fact, NSR’s Global Satellite Ground Segment, 5th Edition report estimates the 2019-2029 cumulative revenue opportunity for Non-GEO HTS user terminals to surpass $5.3 Billion.

Unquestionable Opportunity

The arrival of NGSOs holds the promise of unlocking a new wave of growth for equipment vendors. The new attributes for Non-GEOs such as higher throughput per site, lower latency or potentially lower capacity pricing are very attractive for higher-end segments like Cruise, Backhaul and Trunking. These in turn are highly profitable segments for ground segment actors.

Equipment vendors can’t afford missing the NGSO boat. For some of the high-end verticals like Backhaul and Trunking, Non-GEOs will represent 50-60% of the remote terminal annual revenues when these constellations scale by mid-2020s.

Price to Access

Similar to what happened with the selection of satellite manufacturers, a big portion of the heavy lifting of technology development for ground segment is carried by the industrial partners, rather than the constellation themselves. This involves big risks for equipment vendors, as nothing guarantees they will be selected in the bidding process. Even if they win the deal for a specific constellation, there is still a big risk associated with each constellation being successful (OneWeb bankruptcy and the challenges experienced by the value chain are a clear example).

Some of the R&D necessary to play in the NGSO space are common to other areas like the transition to the cloud, adoption of SDN/NFV or standardized service orchestration leveraging 5G standards. But others are very specific to Non-GEOs with very different approaches by each constellation (bent-pipe vs. data-processing in Space, fixed beams vs. flexible payloads, Ku/Ka-Bands vs. Q/V-Bands, etc.). These specific requirements are the hardest to justify an investment on given the uncertainties around each architecture.

Bottom Line

The current concentration of NGSO constellations (just a few actors concentrating very large deals for equipment vendors) make it a “buyer’s market”, and constellation developers are putting a lot of pressure on the value chain.

Given the large share of the NGSO business, equipment vendors can’t afford being left out of the ecosystem. However, they must be very careful when selecting the right partners and carrying constellation-specific R&D efforts, as these will define the fate of their NGSO returns on investment.

###

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning.

Please contact info@nsr.com for more information.