The Growth of Edge and Cloud Computing in Space

Terrestrial technological innovations such as cloud connectivity, artificial intelligence (AI), machine learning (ML), and interoperability are continually transferring to the space sector as more industries move towards digitization. While the vision to increase efficiency in orbit is there, the reality is that it is more challenging to achieve the same in the space sector because of longer and costlier developmental cycles. With that in mind, what do these technological innovations imply for the satellite industry, and why do they matter for satellite cloud computing?

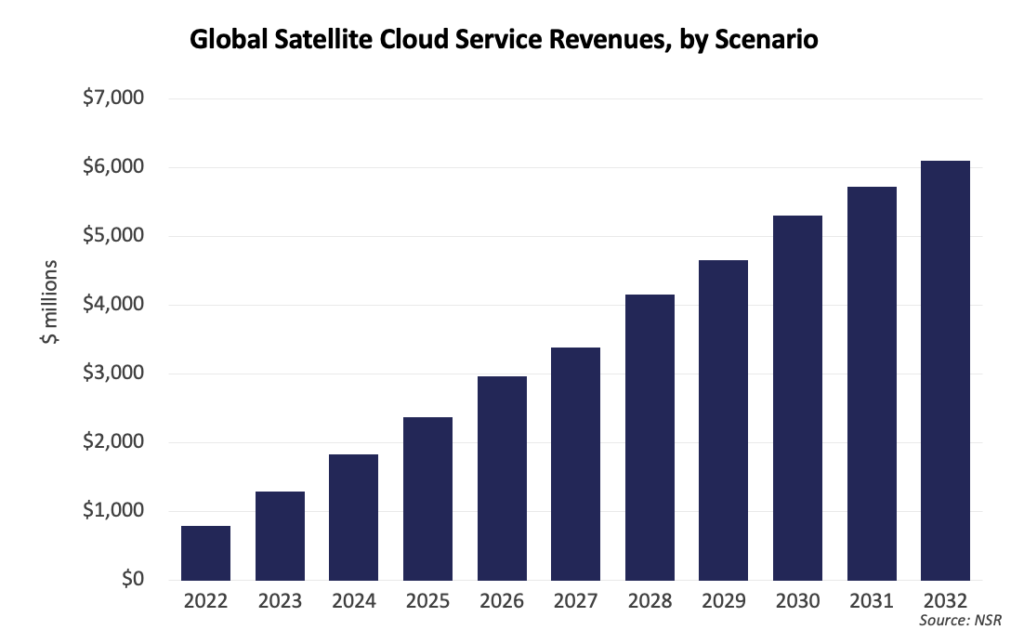

Digitization, an Enabler for the Cloud

NSR’s Space Cloud Computing Report, 4th Edition report forecasts $37B in satellite cloud service revenues from 2022 to 2032. Of this, 71% is driven by data downlink and 29% by SATCOM as the increasing volume of satellite data requires more storage, processing and API whether in data centers or on the cloud.

LEOcloud and Axiom Space are cooperating on space-based edge computing, extending compute and cloud storage needs to the space environment. Meanwhile, AWS successfully demonstrated in-orbit AI and ML capabilities, via analysis and processing of data to only downlink the most useful images afterwards.

Although these developments are unique attributes for now, they may become must-have assets in the future. It not only is more challenging to analyze large quantities of data, but the industry is also constantly looking to move faster in everything. As a result, the NRO incorporating ML/AI capabilities on satellites in orbit could be a game changer happening right before our eyes.

With more data being generated from thousands of satellites, especially constellations, it makes sense to extend edge computing, the cloud, and ML/AI capabilities to orbit, especially if it proves to be more reliable and drives costs down. The European Commission is even looking into the possibility to move entire data centers to orbit, reducing carbon emissions from data centers on Earth.

The New Ground Movement

To reach peak efficiency, space and ground segment developments need to be better aligned. Some government organizations such as the U.S. Space Force, NOAA and ESA have recently turned to the private sector to modernize their ground infrastructure. And hyperscalers AWS and Microsoft are also heavily invested in the space industry to offer ground station-as-a-service or virtualization.

Overall progress has been slow, as the ground segment is often forgotten. With few(er) players focused on ground infrastructure due to high developmental costs and technical challenges, digitization is moving faster on the satellite itself, creating a technological mismatch between ground and space.

As the industry calls for a “new ground movement”, they work through DIFI, which is supporting the standardization to interoperate with different satellite networks, including Software Defined Satellites, and LEO/MEO constellations that are compatible with cloud-based networks.

The Bottom Line

Satellite cloud computing has limited benefits as a standalone service compared to server data storage. Its value lies in how it can be used in combination with digitized systems and facilitate interoperability, automation, and efficiency in orbit. However, a technological mismatch between ground and space still limits the industry. As these technologies converge and mature, the cloud opportunity will continue to grow and change the way we process and gather data from space.