The Impact of Capacity Pricing on M&A and Investment Decisions

The satcom industry today relies on five major elements – Pricing (competition), Supply (indicating Asset worth), Demand (Growth), Break-even pricing (manufacturing innovation) and Ground System (efficiencies). While the economics of demand growth and ground system efficiencies have been proven to be more linear in the last several years, the same cannot be said for Supply and Break-even pricing. The latter two parameters have seen an exponential push in the past 10 years, widening the gap between supply-demand, whereas coupled with increased regional competition, pricing has undergone a steep decline in recent years.

State of the industry

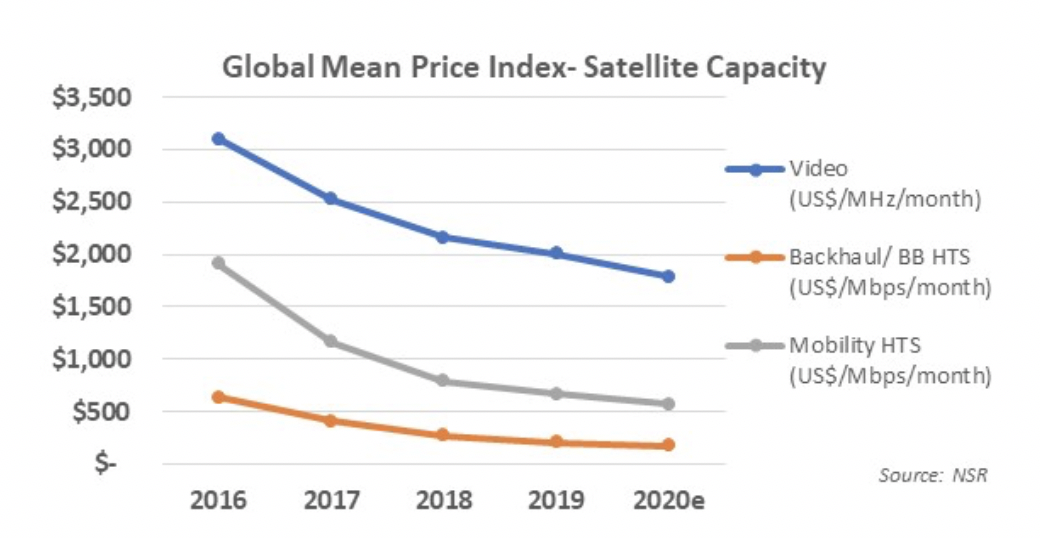

The Global Mean Price Index, built from NSR’s Proprietary Pricing tool in Satellite Capacity Pricing Index, 5th Edition, describes this rate of decline across key verticals in FSS and HTS. Notwithstanding, as the 2018 to 2020e price graph dips, the Global HTS supply-demand gap in the next graph climbs from 50% in 2019 to 65% in 2021, and then closing out linearly until 2027.

Thus, the HTS Supply-Demand Gap, one of the key price pressure points for both FSS and HTS capacity peaks around 2021-22 time-frame, indicating a certain bottom pricing levels for GEO payloads. Decreasing duration of contracts and further commoditization of capacity decrease the average price of lease capacity in the market as well impacting heavily on lease revenues, even if more demand can be generated through this elasticity.

With an average FSS Break-even price (lowest price for capacity without enduring a loss) of a satellite dropping from $1,500/MHz/month to $600/MHz/month, and with HTS Break-even prices dipping from $28-60/Mbps/month in 2017 for large Consumer BB payloads to $12/Mbps/month by 2021, this timeframe will prove to be a litmus test for multiple operators.

Will this Dynamic Push the Market into an M&A?

The key question arises – How does one reduce the impact of pricing, and how does a company future proof growth? Is it through acquisitions?

Answering this necessitates to look at the change in current business models: Most operators are adopting service business lines in broadband, maritime or video, with a late surge coming in data segments as well. Expectation of 25-30% managed services revenue by 2021 from the operator industry in not unlikely, thus acting as a shield to accelerating price decline. Preserving contract value via increased bandwidth consumption (with price reductions) has become a norm in 2018-19, showing partial elasticity in data, backhaul and maritime passenger segments. Operators look to create captive growth markets undercutting competitors, and with interim CAPEX cycles ending, many operators are also creating favorable Net Debt/EBITDA positions to acquire other companies. Growth through complementary mergers becomes straightforward, noteworthy with Inmarsat acquisition from PE investors, who unlike operators or service providers can shoulder a large cash burden to facilitate such scale.

How will the Investment Patterns Change?

Near-to-Medium Term

Operators will look to invest to grow revenues via newer product lines capitalizing on HTS launches, entering into complementary service business lines, enter new markets via condosats or via incumbent-aided market entry partnerships. Service Providers will look to invest to stabilize profitability and increase EBITDA via upstream fleet synergies (vertical integration possibilities), or horizontally consolidate to minimize competition in critical data centric growth markets. Regional operators could most likely resort to down-pricing HTS capacity with expectations of elasticity from markets like South East Asia and Latin America, while strengthening their Mbps centric offerings through tech integration towards large customers.

Long Term

Operators will look to build telco-like supply and distribution networks that enable recurring subscription retail models to ensure an efficient match between asset and revenue lifecycle, with duration of contracts tending to less than 3 months. Non-GEO plans are expected to necessitate such models even further, due to shorter CAPEX cycles. Country-specific segment dominant (video/data/mobility) positions will be vital to stability for both operators and service providers, and coupled with service business line double digit growth, an increased competition may lead to a merger (vertical integration) towards 2021-22 between some companies. Finally, cross-acquisition of satellites to support a segment specific dominant position for a service provider can’t be ruled out, as the industry moves away from niche-lease plays to a more efficient pay-as-you-go business model.

Bottom Line

With dynamics changing so fast, stakeholders will keep a close eye on the Pricing Index, complementary fleet synergies and distribution lines for a service provider, EBITDA margin recovery, and finally long-term sustainability of service business lines for semi-nationalized operators. 2021-22 may prove to be a litmus test for many companies, but it would also be an opportunity for a PE firm/Telco/Large Operator or SP to consolidate, streamline assets and build retail models. Mobility and video services segments in developed regions, and data segments in under-developed regions may witness more such acquisitions or incumbent-aided market entries in the near to medium term.