Tip of the Iceberg for Maritime SATCOM?

Today, it is easy to find dramatic pictures of icebergs floating around the world’s oceans – themselves chunks from some larger ice shelf, their mass mostly underwater, unseen. However, both the above water and underwater parts of these icebergs are subjected to environmental pressures – pieces falling off are a response to those external factors. Similarly, SpeedCast and GEE both had problems before COVID-19 hit, and their bankruptcy filings should really come as no surprise. As the mobility satcom market experiences an unprecedented disruption, these already stressed businesses made hard choices around their future – internal fractions in the iceberg of Maritime SATCOM Connectivity. What is less certain, and what should worry everyone, is what these events mean for the larger mobility SATCOM markets, particularly the maritime SATCOM sector. What other external factors can we observe, and more importantly, how should we think about what lies beneath the surface?

Looking at perhaps a ‘simple benchmark’ to start to answer that question of the health of the other providers is the number of ‘connectivity contracts’ that have been announced lately, compared to years past. While an imperfect metric due to differences in deal sizes (number of vessels/revenue), changes in publication of announcement preferences, etc., it does give at least some barometer in which we can start to look at the structure of the market. In short, if connectivity contracts are only the tip of an iceberg we call the “Maritime SATCOM Markets,” any changes above the surface are probably signs of instability both below the water line, and indicative of some changing environmental conditions causing a shrinking iceberg.

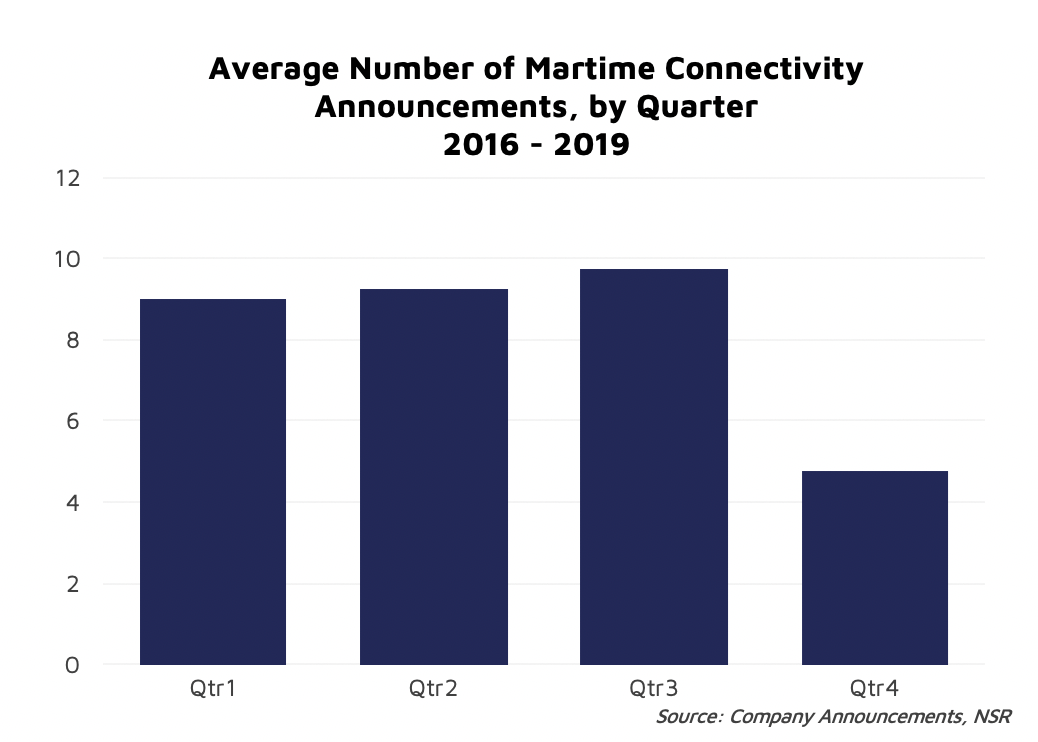

According to data NSR tracks from announcements in the public domain, on average from 2016 to 2019 we recorded annually around 30 – 40 public connectivity contracts for Maritime End-users. Specifically, Quarter 3 (this quarter) is typically when we should expect to see a peak of announcements. Again, this doesn’t account for the ‘volume’ behind these announcements, just a reflection of the number of press releases service providers issue.

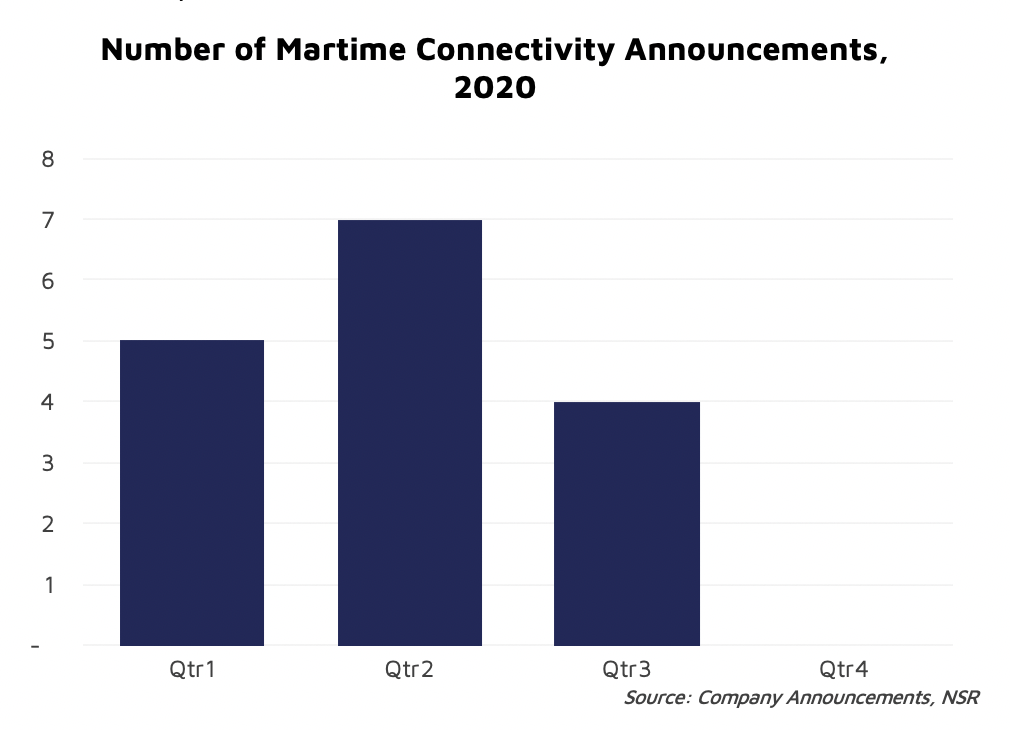

So, how is 2020 shaping up? Well, the Q1+Q2 announcements have totaled around 12 – down from the historical average of 18 announcements for the first half of the year. While we have already recorded 4 announcements in Q3, Q4 is historically the ‘slowest quarter’, so we would need to exceed the Q3 announcements from 2016 to really see a significant recovery in ‘year to date announcements’ by the end of Q3. Again, this doesn’t reflect the amount of ‘actual vessels’ being equipped in these announcements or what percentage these announcements represent in terms of ‘total connected vessels’ – but, problems on the iceberg above the surface are no doubt going to work their way through the entire market.

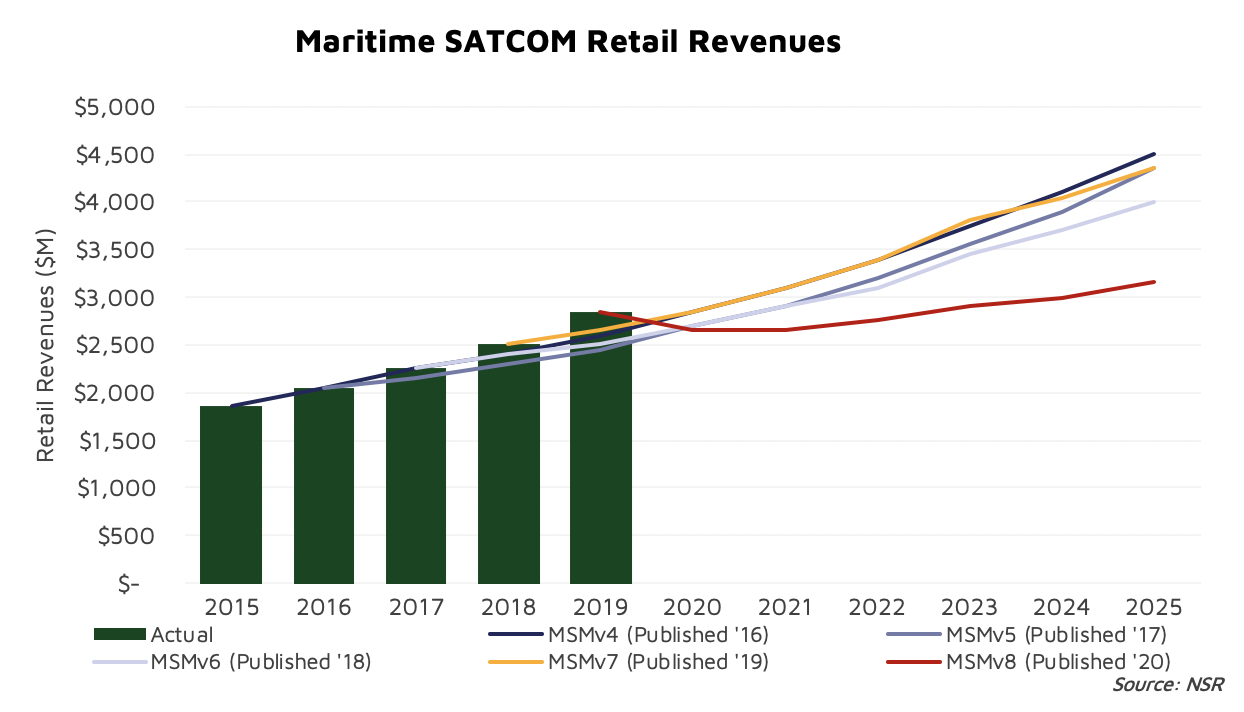

Announcements are the ‘above the waterline’ factors for our Maritime SATCOM iceberg. Already, As NSR mentioned in its April 2020 Maritime SATCOM Markets, 8th Edition report, the overall market is in a period of hardship. From 2019 through 2021 the market is expected to decline by around $230M, or roughly an 8% decline. In a market that between 2015 to 2019 posted about 10% year over year increases… any decline in topline figures is a ‘big deal’. Largely concentrated in the Passenger Maritime and Energy Sectors (both of which SpeedCast and GEE have significant presence), and it isn’t a significant surprise that already stressed businesses are falling on harder times than their peers. However, it does start a conversation around the mid-term viability of current players in the maritime (and larger mobility) SATCOM markets.

Overall, the market is in a period of transition from MSS connectivity to VSAT. With 2019 adding almost 3,500 new VSAT vessels compared to 2018, and 2020 still poised to add more VSAT vessels amongst all the challenges the market faces, concentrated challenges in passenger and energy markets are only a part of the overall Maritime SATCOM market. While physically installing hardware and supply chain issues are likely to continue well into 2021, the market is already on a “VSAT-focused” path. However, that transition will fuel the longer-term health of the market. Without access to robust connectivity, ‘digital transformation’ is a non-starter. In short, while we are seeing every indicator that our iceberg is shrinking, future conditions all point towards better external factors to enable growth.

Bottom Line

While this week marked the first ‘large ship’ cruise voyage (TUI’s Mein Schiff 2 on a Hamburg-to-Hamburg trip with 1,200 guests aboard), for the satellite connectivity sector everyone is asking – how long does it mean to be ‘in it for the long haul’? Two of the major mobility players have declared bankruptcy, SpeedCast and Global Eagle Entertainment, and while both of those companies already had challenges in the pre-COVID-19 economy, it does start to ask the question of how long can the ‘well positioned’ players survive? As conditions on the ground continue to change, cruise sailing dates continue to get pushed back, and other macroeconomic conditions impose challenges for Energy and Commercial Maritime Markets – is it just ‘matter of time’ before others face their own set of challenges? Just how much should we read into these ‘tip of the iceberg’ factors?