UAS Imaging: Roadblocks and Opportunities

The use of small Unmanned Aircraft Systems (sUAS) in the commercial world is still nascent and growing with drone technologies developing rapidly, be it with payload, energy or autonomous capabilities. Amongst the many applications being explored with UAS, ranging from delivery services to infrastructure development, imaging stands out as the frontrunner with a high interest in adoption from businesses, and a clear business case.

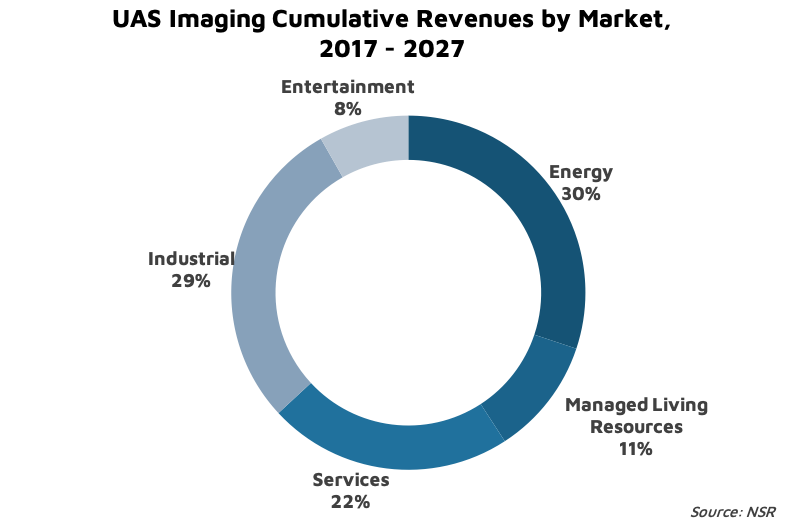

NSR’s UAS SATCOM and Imaging Markets, 5th Edition report projects the annual revenue opportunity for UAS imaging will reach upwards of $600 million by 2027, with a net revenue opportunity of nearly $4.2 billion through the years 2018-2027. What is driving this market? And just as important, what is restraining the market opportunity?

Regulations Easing Up

Even as the consumerization of drones is underway, NSR expects the Energy, Industrial and Services market verticals to remain the mainstay of commercial UAS imaging/analytics providers, providing ample opportunity for drone surveying/mapping solutions. Meanwhile, regulations have risen as the need of the hour, with the recent incident at Gatwick in the UK spurring discussions as more countries look towards implementing a UAS Traffic Management (UTM) system.

Notably last year, the Directorate General of Civil Aviation (DGCA) of India published its updated drone policy to tackle such concerns, ensuring that it addressed the UAS operating environment as well as ground/air safety concerns in an integrated manner, and took its Digital Sky Platform live. The commercial UAS imaging market in the country thus far held back by a lack of rules/regulations is now expected to take off as processes for obtaining licenses and clearances becomes easier.

The U.S. Department of Transportation (DoT) more recently proposed new rules relaxing some of its previous regulations. As regulators acknowledge the need to mitigate security/safety risks without hampering operational/technological advances, restrictive regulatory barriers are expected to decrease. In December 2018, Measure received an FAA waiver to fly within the DC Flight Restricted Zone (FRZ), for aerial inspection of a construction project.

More advanced operations such as broad area imaging will see greater adoption, as UTM begins to account for Beyond Visual Line of Sight (BVLOS) commercial applications. One of the first such use cases was seen in Germany in 2018, when the construction giant, Strabag utilized a UAS from Microdrones for BVLOS corridor mapping. With the current conversation tending towards UTM globally, the UAS imaging market awaits a more robust regulatory framework to really open the potential for increased commercial applications.

Potential for Analytics

Software for mapping/GIS solutions in the market is rapidly maturing, and the barrier to entry for imaging related drone services is relatively smaller. As more small and medium enterprises (SMEs) take up mapping contracts, commercial UAS service providers have begun to shift towards a higher-end “drone-as-a-service” analytics offering for premium clients. Asteria Aerospace, for instance, identified this opportunity for UAS technology in the imaging/analytics world, and partnered with data intelligence provider SatSure to jointly offer image analytics solutions, further cementing the importance of data agnostic approaches with hybrid datasets. This is similar to what NSR observed in the Earth Observation (EO) and satellite big data analytics markets: data is out, insight is in.

Fueled largely by technology development and competition, commercial drone imaging service providers / operators have begun to take advantage of decreasing manufacturing costs of the UAS platform, payload etc. to provide image acquisition/processing services at lower costs.

The Bottom Line

The commercial sUAS market is expected to become more crowded as barriers to entry gradually drop. The primary application will continue to remain imaging services, fueled by the needs of digitalized customers, particularly in the energy and industrial vertical segments.

Regions experiencing a high demand with a premium client base and robust regulatory environment (as compared to other regions) will drive this demand. Despite technology driving market growth, regulatory frameworks that are consistent at the international (and regional) level will be key in scaling this industry.