Will Software-Defined Satellites Take Off?

In recent years, satellite operators have busied themselves finding new ways to deliver cost-competitive connectivity in response to evolving consumer demand and price expectations. On the satellite design side, this encompasses new architectures, multiple forms of heightened risk taking, and adoption of low or no heritage technologies. SES is pushing this process even further with proposals for a standard-build, software-defined satellite that could be purchased off the shelf for use in any orbital slot by any operator. Yet, with buy-in needed from both manufacturers and competing operators, will the idea take off?

The appeal of a software-defined satellite is plain to see, and has been an industry target since before SES became its champion. The ability to change frequency bands, coverage areas, power allocation, and architecture (widebeam vs HTS, for example) on-demand, at any point in satellite lifetime, enables an operator to capture diverse markets. It can address new applications as they emerge, compensating if the initial target market falters, or more simply respond to a rebalancing of demand. Standard-build satellites also add flexibility to an operator’s fleet, making satellites interchangeable in the case of anomaly or shifting priorities.

All of this is advantageous considering today’s more variable market, where new applications emerge while others decline, contract durations are shortening, pricing continues to drop, terrestrial solutions overtake traditional satellite markets, and consumers are unforgiving in their search for optimal connectivity. Despite this variability, the chance of a software-defined satellite becoming obsolete in its lifetime is low.

But as is the case with any generalist/specialist tradeoff, a standard-build satellite will be able to address a broader overall array of demand but might not address individual markets as competitively as a tailored satellite. The full SES design targets are yet to be publicized, but the satellite will have limited payload power (with mass estimates below 3,000 kg, this would likely fall in the mid-range of a power spectrum that has been steadily increasing), may not operate in the full spectrum of commercial frequencies (L-band?) or offer next generation capabilities (optical feeder link?), obligate ground segment investments (changing frequencies mid-life?), etc… Moreover, operators today have access to a suite of options from which to compile a competitive strategy – not only are standard-build/software-defined satellites on the table, but very high throughput satellites (e.g. ViaSat-3), smallsats in GEO (e.g. Astranis), condosats (e.g. GeoShare), blended GEO/MEO/LEO constellations, and in-orbit servicing and assembly, amid other budding ideas, are feasible pathways as well. Each offers a unique blend of risk, cost per bit, flexibility, and market applicability.

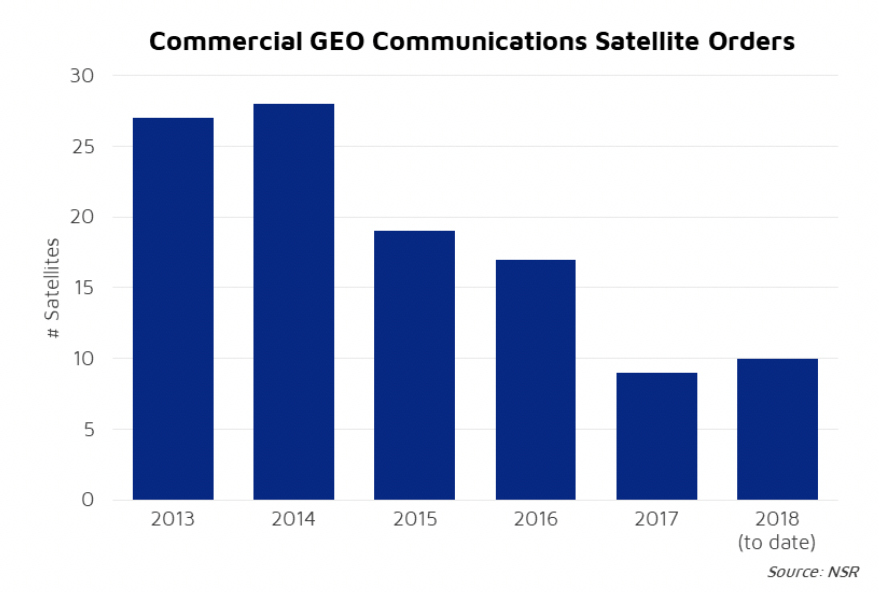

Yet SES, or the suppliers it chooses to work with (Boeing, Airbus, and Thales Alenia have been selected as finalists), must attract other customers to justify the NRE required to design the satellite and support initial production costs. Players like Eutelsat are intrigued by the idea (as seen in their partially software-defined Quantum program), but it is far from certain if other operators will sign on for the first run. And while risk-tolerance has increased, the value must be exceedingly compelling to justify an operator to pre-commit to multiple satellites of an unproven design in today’s CAPEX-conscious market. NSR found in its Satellite Manufacturing and Launch Services, 8th Edition that a decline in total GEO orders in the last four years complicates this, reducing opportunities to win orders and increasing the market share the standard-build satellite must win – thereby increasing risk. For manufacturers, development of this capability is a gamble – whether to undertake and risk not winning enough business to recoup investments, or to ignore and lose out on future demand if the approach is successful.

While this cost and risk must be resolved, in principal standard-build satellites dovetail with what manufacturers have been considering for years: standardization as a way to cut costs and reduce production timelines. Standardized satellites with customization only late in the production process or in-orbit does require operator pre-commitment, but it helps to streamline or eliminate the costly RFP process. It also allows optimal supply chain management for long lead or mass-produced components and can stabilize revenues and CAPEX planning for manufacturers and operators, respectively. To date operators have been hesitant to relinquish the control and customization offered by the RFP process, but a compromise in procurement might be required to enable the desired reductions in pricing – and a standard-build, software defined satellite serves this process.

Bottom Line

The standard-build satellite is not a solution for all players and all requirements in today’s market but can offer compelling value for operators seeking a flexible solution to optimize cost, risk, and revenue. The manufacturer who delivers on the concept stands to benefit from ongoing business, but only if the risk of recouping NRE can be supported. This undertaking thus requires both competitors and multiple layers of the value chain to move in tune with each other, committing resources to a capability as yet unproven. Full standardization and software-definition is a capability the industry will undoubtedly reach eventually; the groundwork for such a capability has been established, and in the increasingly challenging market of tomorrow for both operators and manufacturers, someone will take the risk to reap the reward.