Yield Management in Satellite Backhaul

Satellite capacity price reductions have been critical to unlocking growth in markets like Backhaul. New price points made ultra-rural network deployments ROI-positive, unleashing solid elasticities and growth. But, is satcom leaking value to other steps of the value chain (MNOs, integrators) due to price competition? How should satellite operators and integrators optimize their pricing strategies and pivot their business models to maximize value capture in Satellite Backhaul?

Backhaul will be one of the key verticals for satcom growth in the coming years. The COVID-19 crisis might delay some deployments (challenges with financing, installation or supply chain), but in a world in which communications are more critical than ever, NSR continues to be bullish about the prospects for this vertical despite the current uncertainties.

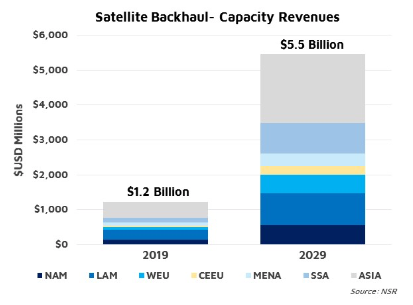

According to a recent survey conducted by NSR across a wide variety of the Satellite & Space sector value-chain, satellite backhaul was identified as a resilient application in the wake of the COVID-19 global impact. In fact, NSR reiterates its long term forecast for Satellite Backhaul generating over $30 Billion in 2019-2029 cumulative capacity revenues (Wireless Backhaul via Satellite, 14th Edition). But in a vertical attracting more and more attention from the industry, establishing the right price and business model strategy is more important than ever.

Finding the Right Equilibrium

The advent of HTS and oversupply in certain markets led to drastic price reductions over the past several years. While this has obviously had an impact on Satellite Operators’ bottom line, one could also observe an upside with multiple new markets unlocking elasticities like Cellular Backhaul. Traditionally dependent on government obligations or subsidies, new price points have transformed the landscape where it is now possible to deploy Satellite Backhaul without any government support in ultra-rural areas and find a positive return on investment. This is a critical moment for the industry as there is a massive addressable market to be captured with many years of growth ahead.

However, price pressure continues in many markets due to the arrival of fresh capacity and greater levels of competition. This is putting the industry in a delicate situation where some portions of the value created by satcom leaks to other stages of the value chain. Assuming a typical Macrocell in an emerging country consumes 3,000 GB/month (serving 1,000 users at 3 GB per user) at an average price per GB for the end-user of 3.5 USD/GB (graph above), one could plot the costs of serving that Macrocell at different satellite capacity costs (TCO considering RAN equipment, Backhaul, Teleport, Commercialization, etc.).

NSR sees the current average price for large Backhaul deployments in the neighborhood of 300 USD/Mbps/month, very much in equilibrium to allow MNOs to close the business case and at the same time capture a healthy share of the value. However, as prices might continue to degrade, the industry could see part of the value generation (the average price that the MNO could charge to the end-user) moving to other steps of the value chain, making the margin for the MNO or the integrator greater but at a loss to the satellite operator. One must also consider that the average price per GB that the end-user is willing to pay also decreases every year, so satellite capacity prices and infrastructure costs should evolve in parallel to keep the business case profitable.

It is also worth noting that as MNOs need to close their own business case, satellite operators have a limit for the price they can charge for the capacity. While the demand for HTS-Ku for Cellular Backhaul in the U.S. is greater than supply, operators are unable to raise prices as MNOs need to capture their own margin from deployments.

Selecting the Right Markets

The price per GB that the end customer pays varies widely depending on factors like technology (2G/3G/4G), package (contracted volume) or service provider. But it is sometimes surprising to observe how divergent the average prices per country are, as this can range from 0.26 USD/GB in India to 75.20 USD/GB in Zimbabwe. Satcom must obviously prioritize those markets where it can extract the highest value and offer a targeted price strategy depending on the local conditions in each country.

These wide differences partly explain why markets in which one would expect high levels of demand like Russia (vast inland territories with challenging fiber backbone deployments) or India (underdeveloped terrestrial infrastructure) show very low levels of Satellite Backhaul demand given the extremely low average price per GB. On the other hand, developed markets with healthy average price per GB like the U.S., the UK, or Japan do make extensive use of satellite despite having nearly ubiquitous fiber coverage.

Getting Closer to End-users

MNOs are quite comfortable with reverse auctions and can easily exert a lot of pressure on suppliers to reduce prices given their scale. Consequently, the old wholesale model is very risky for satellite operators. In parallel, many MNOs lack the skills to implement satellite, leaving a lot of latent demand unserved.

The industry needs to get closer to end-users by developing fully integrated solutions. This means accepting greater risks by co-investing in rural deployments and adopting innovative business models such as revenue sharing schemes, pay-per-GB, etc. This offers a win-win scheme where MNOs can expand into new markets at low CAPEX risk and without putting more pressure on their operations (rural network operation stays on the satcom party), and the satellite industry can extract a greater share of the value.

Bottom Line

Capacity price is one of the heaviest contributors to Total Cost of Ownership. With recent price declines, Satellite Backhaul is (finally) an economical alternative for MNOs to extend network coverage into rural areas. The market is at an inflection point where this will trigger solid growth for the industry.

However, price pressure continues as new supply hits the market. This can be counterproductive for the satcom industry as some portions of the value created can leak to other stages of the value chain (MNOs).

Staying with the wholesale capacity lease business is risky for satellite operators as it would be relatively easy for MNOs to continue putting pressure on pricing. Consequently, the industry should move closer to end-users and accept a bigger share of the risk by developing co-investment schemes with MNOs.

NSR supports equipment vendors, service providers, satellite operators, end-users, public agencies and financial institutions in their technology and business strategy assessment and planning. Please contact info@nsr.com for more information.