Satcom Business Models in a 3.0 Era

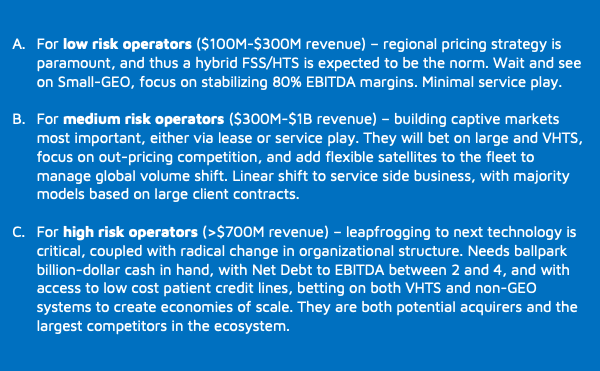

NSR analyzed various fleet replenishment strategies in the year-end NSR’s article on Satcom 3.0 era, discussing relevance to operator per size and risk-taking ability starting in 2020. The growth patterns look quite different for operators falling between revenues of $100-$300M (low risk), $300M-$1B (medium risk) and finally greater than >$700M (high risk), and thus we began to inspect elements of business models that might be relevant to each category. Seven major elements are reviewed within the 3.0 era context.

- Growth Applications: While video remains essential to most operators, most growth will occur in ABC (Aero, Backhaul and Broadband) segments. Every operator is expected to hedge the video decline with a growth in mobility, either via incubating an in-house division or with external partnerships.

- Break-even Pricing Targets: With multiple new satellites coming online, and tech cycles shortening, this metric has been on the decline and for good. Mass market play would dictate future floor pricing create new targets, with consumer broadband requiring less than $15/Mbps/Mo, backhaul less than $30/Mbps/Mo, and Aero at less than $60/Mbps/Mo. Gov/Mil will continue to attract the most dollars per Mbps bandwidth leased/used. Constellations aren’t expected to match VHTS on pricing, though will certainly compete on volumes in selling to telcos to airlines.

- Market Access Focus: While low risk operators are expected to have a regional strategy due to limited orbital spots, medium and high-risk operators will look at Latin American and Asia Pacific markets to register growth across data segments. SES, Inmarsat and ViaSat remain bullish on mobility, while Hughes and Eutelsat punt big on consumer broadband. North America, Atlantic Ocean, Europe, Middle East and East Asia will continue to be hotbeds for aero connectivity.

- Revenue Model Focus: While low risk operators are most suited to build lease-based revenue models, extracting maximum advantage/EBITDA from a small operational team, medium sized operators will need to build both bulk lease and limited service play targeting regional end-users. Large sized operators must punt on deriving maximum growth via services, either via large end-user (maritime/ aero) specific business cases or investing in a new partnership with a service provider to create a second pillar of business. Third party revenues will be critical to growth as companies start to commercialize non-subscription-based offerings either via content delivery or advertisements.

- Types of Partnerships: Regional landing rights, terminals and distribution are the toughest issues to solve, in a greenfield market or in a VHTS/ constellation fleet model. Partnerships with local vendors are key for most operators, with equipment-based partnerships essential to future-lock an ecosystem, especially for large risk operators. Service provider partnerships are expected from medium sized operators in a bid to outperform large ones, where such partnerships could result in a possibility of a consolidation too. Cloud partnerships have begun to revel as operators look to make content available directly to the end-user on the choice of node/device.

- Accessing Credit: As the industry returns to growth, operators will need faster access to capital. Renewed interest from private equity is a good sign for operators/service providers, while drying up of credit via export credit agencies is a cause to worry. Standard 15-year business cases carry more risk than ever, and thus options like small GEO (6-7-year lifetime) have begun to spring up for new operators to get cases funded. Other options are hosted payloads or condosats, which reduce risk on one operator and enables a quicker access to capital.

- Consolidation Strategies: Future proofing expected growth requires consolidation. The last 14 months is evidence to the confidence of the industry, backed by low CapEx and extraordinary supply growth. With 3 large acquisitions and 2 buyouts across operator, service provider and equipment vendor layers, the focus has been on consolidating revenues per vertical. The Globecomm deal strengthened Gov/Mil revenues for Speedcast, while the Gilat deal gives Comtech an almost monopoly in backhaul equipment business. Such targeted, complementary and horizontal acquisitions will definitely be seen more in 2020/21.

The Constellations Effect

Due to competition in volumes and preference for constellations to lease in bulk – the pressure on pricing will be immense for the GEO-HTS players. Flexible satellites could showcase the way if GEO-HTS players will need to switch regions on account of constellations pricing (post landing rights acquisition). Although, constellations currently look to disrupt limited verticals of the industry given the dearth of terminal tech and non-accessibility to most large populated regions. This is where large GEO-HTS can make a difference with a lead time of at-least 3-4 years.

Bottom Line

The above metrics indicate clarity for each operator category around fleet, pricing, growth applications, market access and credit access. However, operators are finding it difficult to choose types of revenue models, market access regions and methods, and partnerships. This is where most uncertainty lies today.

Service model and mass market shifts are clear, along with the need of consolidation, as evidenced in the balance sheets and deals of the past year. 15-year business models will face sizable scrutiny, and the fight will be towards subscription models (to showcase independence from backlog metrics) to build confidence on an Annualized Run Rate basis.