A 2020 Turnaround for Oil & Gas SATCOM Markets?

We won’t lie – 2018 was a hard year for satellite players with an interest in the Energy Markets. Commodity pricing for energy products was weak or unstable, global economic activity shrank, and energy customers had their own financial challenges. So – in the face of ongoing macro-economic challenges, why does NSR continue to be so optimistic around a 2020 turnaround?

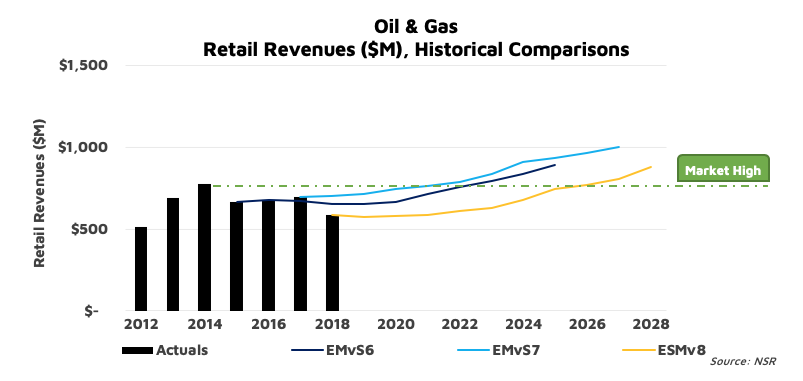

According to NSR’s Energy SATCOM Markets, 8th Edition report (and our 7th Edition published in 2017, and 6th Edition published in 2016) the Oil & Gas Markets are shaping up for 2019 into 2020 to be a ‘turnaround year’ for onshore activities, offshore exploration, and generally better levels of project expansion. Moreover, the two major Energy SATCOM Market Service Providers that publish financial data (SpeedCast and RigNet) have both given indications of positive revenue growth in their energy segments in the first half of 2019, and all indications of ongoing positive growth into the end of 2019 and into 2020. We at NSR agree.

Breakdown Down the Growth Drivers

The Oil & Gas Markets are driven predominately by two factors – the price of crude and the backlog of ‘extractable resources’ companies have; fairly straightforward metrics. In the runup to the crash in 2014 – 2016, the price of crude fell dramatically, to the point where cost to extract oil & gas that made up the backlog of ‘extractable resources’ vastly exceeded the market rate (and the projected market rate).

As such, oil & gas end-users faced a dilemma – wait out what could be a short-term dip in pricing or start the long process of shutting down exploration and production sites, stacking rigs, and retooling themselves to operate in an environment with lower crude prices.

Practically, most waited it out as long as possible (and some went bankrupt in the process), pushed off greenfield activities, and stacked rigs or killed-off new build contracts. For SATCOM Service Providers, the impact meant fewer sites required connectivity, and new ‘cash optimization strategies’ from their customers meant that if you wanted to keep business, you had to cut a pretty significant deal. 2016 was largely a ‘stabilizing year’ due to that impact of the greenfield sites were shut-off, and cash optimization strategies were only beginning to roll-out. By 2018, end-users retooled their operations, optimized their backlog against projected crude pricing and starting to expand exploration & production activities. Yet, service providers are still feeling the cash-optimization strategies in terms of their overall pricing abilities.

Looking into 2019 and beyond, the digitalization of rigs/platforms/vessels will continue to drive bandwidth demand to newer heights, and the years of backlog neglect are catching up with oil & gas end-users – they need to explore for tomorrow’s revenue stream. This process of retooling and optimizing their internal operations takes time – with most estimates saying somewhere in the 24 – 36 months. Beyond 2020, and satcom market factors start to weigh-in on the forecast; What’s capacity pricing doing? Is LEO going to be a ‘big thing’? Do SPs need to ‘pass along the savings’?

Overall, we shouldn’t expect the market to return to the ‘heyday’ of 2014. NSR expects that with the combination of lower latency satcom services and end-user demand for more automation that 2025 might be the year which we see revenues exceed 2014 levels.

Bottom Line

SATCOM Service Providers in the Oil & Gas Markets aren’t out of the woods – ‘return to growth’ doesn’t mean a return to a 2014-market overnight. End-users are still looking for a good deal, and the path to the ‘good old days’ remain challenging. New satcom services in LEO and MEO will be key to some of that growth, while GEO-HTS serves as the new-normal for network architectures. Overall, NSR has looked at 2020 as the ‘year of improvement’ for a few years now, and all signs are shaping up that next year will be ‘the year’.