Consumer IoT: A Vast Untapped Satcom Opportunity?

M2M and IoT via satellite has traditionally been dominated by industrial applications, with Transportation, Cargo, Maritime and Energy sectors all primary subscribers to satcom M2M and IoT services. At the same time, we’re seeing an explosion of growth in the consumer handheld space in terms of subscribers and revenues, and also new products coming to market tapping into satellite networks. With Cisco estimating 500 billion Internet connected devices by 2030, how far can satellite tap into the consumer space as well as new applications never previously been connected?

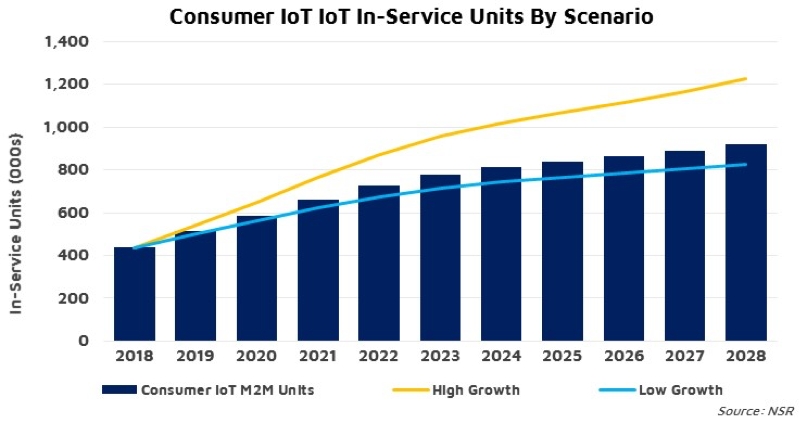

In our M2M and IoT via Satellite, 10th Edition report, NSR forecasted over 920,000 active consumer IoT devices in 2028, up from ~430,000 at the end of 2018, which corresponds to annual retail revenues of nearly $200 million in 2028 alone. This category primarily consists of consumer handheld devices, most notably Globalstar SPOT and Garmin. These product lines have now been available for years, with limited levels of competition to date. Seeing the popularity of these devices, in recent years a number of new devices have become available, such as the Satpaq, the Somewear, the Bivystick, and Thuraya’s own satellite smartphone.

While subscriber growth is strong for now, NSR believes that growth will slow over the coming decade, due to a smaller than anticipated addressable market, and competition from new smallsat devices designed for panic button type usage. Longer term, retail revenues will flatten out as well, as ARPUs are expected to decline as more intermittent usage is expected and to counter high levels of churn. Equipment pricing is also expected to decline due to increased competition – something that will prove to be a huge challenge to new entrants.

The strategic issue with the above types of devices is that usage is unlike that of industrial applications, which have a stable usage pattern. Consumer IoT device usage is inherently irregular and occasional. This leads to high levels of churn in this application, which is typical across the segment as consumers and eco-tourism users subscribe for short periods when travelling and then or almost immediately, cancel service afterwards.

Globalstar found this in 2018, with the company having net in-service subscriber growth of ~5,600 in 2018 compared to 2017. Gross subscriber additions were ~69,000 across the same period, indicating that a significant number of existing customers had discontinued service. While Globalstar derives a significant proportion of their revenue base from SPOT, Iridium is less affected due to a sufficiently broad subscriber base, and in the consumer IoT space new partnerships with Somewear and Bivystick further broaden this base.

The other issue is the addressable market size. Given there about 900 million iPhones in the world, plus 100s of millions of other smartphones, and assuming 10 million will be in areas outside of GSM coverage, in theory there should be 10 million consumer IoT or Satsleeve type devices sold. The fact that this isn’t the case, demonstrates that the need for always on connectivity isn’t compelling enough for consumers, based on sales numbers for devices such as the Thuraya SatSleeve and other products. This will be a cautionary tale for investments based on connecting every user outside of GSM networks – that the reality will be a much smaller share of users who really need to be connected everywhere.

With that said, there is also an opportunity for small satellite constellations to address this market with lower pricing structures, and NSR expects more to be developed in future years that connect to these new constellations – which could be priced as low as 1 cent per message. Some of the ~5.3 million in-service smallsat IoT terminals in 2028 will cater to the consumer market and have an impact on MSS services; even more if greater than 3 constellations fully launch. However, reliability will need to be proven on these constellations before these become trusted for an emergency response to be relied upon, and companies will need to partner with GEOS Worldwide Ltd (like other MSS operators) or a similar company to provide emergency rescue services. Such devices can come from unusual sources for the satellite industry – the Iridium connected Bivystick and Somewear have even been funded through Kickstarter – expect more to follow.

Bottom Line

The consumer IoT, with its billions of devices, for the most part will remain on terrestrial connections. Only a very small portion of these devices will have data routed through satellite connectivity. The challenge for service providers, satellite operators and consumer IoT companies will be to reach price points and form factors that will be palatable to casual outdoor enthusiasts, without reducing ARPU from existing higher value customers. This will involve limiting feature sets to consumers such as basic location tracking and social media, while avoiding high level data analytics. Nonetheless, consumer IoT applications will remain relatively untapped from a satellite perspective when compared to the much larger enterprise M2M satellite market, and it is these enterprise applications, which should be the primary focus for operators and service providers alike.