Earth Observation: Analytics-as-a-Service

Satellite-based Earth Observation (EO) is changing from an imagery-driven to insight-driven business. Until now, most satellite operators have been content with supplying imagery, while emerging downstream companies have begun unlocking the value behind the pixel, through Big Data analytics. However, satellite operators are beginning to shift focus.

Last month, Planet completed “Mission 1”, to image the entire globe, daily, and has since focused on Big Data analytics. Urthecast’s collaboration with Esri shows a desire to move to a more application-focused, Software-as-a-Service (SaaS) model, and even DigitalGlobe, whose dominance in the market is unquestionable, recently announced an Imagery+Analytics service.

Big Data analytics has received tremendous funding in recent years, and the marketplace has grown quickly as new start-ups are frequently announced; however, with satellite operators shifting focus, the EO business stands at an inflection point. Considering the threats of competition and consolidation, players in the industry should be asking, “How can we succeed in this increasingly competitive market?”

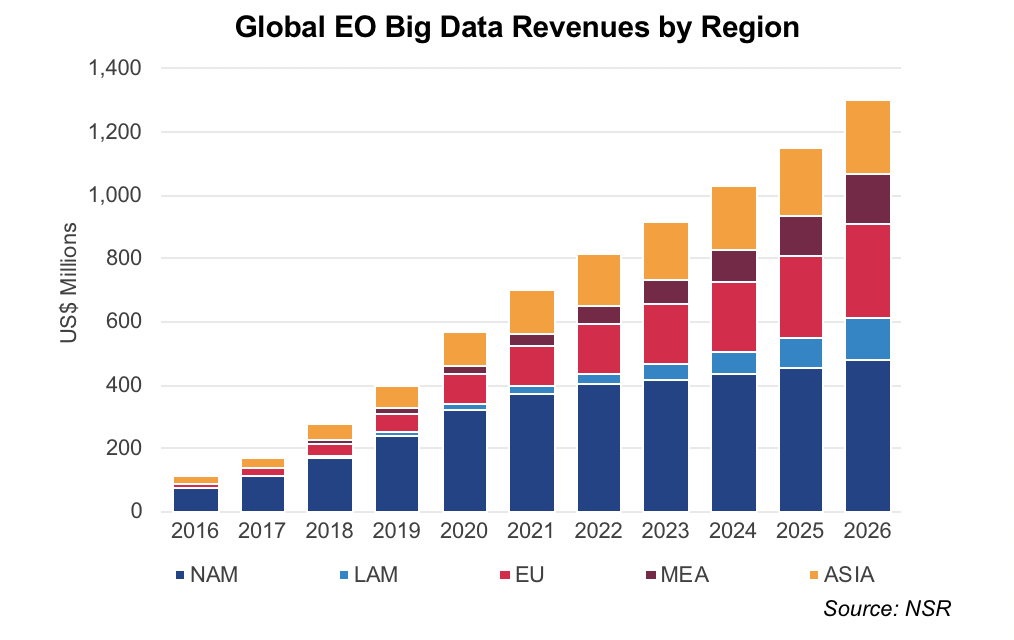

NSR’s Satellite-based Earth Observation, 9th Edition report forecasts annual revenues from satellite-based Big Data analytics for EO will reach $1.3 billion by 2026, growing 5 times faster than the rest of the industry, at 28.1% CAGR. North America will lead the way, reaching $480 million in revenues by 2026, with Europe and Asia close behind. Services are expected to be the largest vertical, and Energy continues to be the fastest-growing, at 34.1% CAGR over the next decade.

Beyond Volume, Variety, Velocity, and Veracity, NSR contends that Vertical is an important focus for Big Data analytics companies. From counting cars to analyzing agricultural financial risk, most ideas in this space have a single vertical focus, with specific challenges to overcome. However, while the entire market is expected to grow, competition and consolidation are looming threats, and many downstream players will find a vertically-focused approach difficult to scale up, especially as satellite operators shift focus toward analytics. In some cases, such as with Planet and Terra Bella, and EagleView and OmniEarth, consolidation has proven easier.

The final barrier for Big Data analytics is commercial sustainability. Project-based models are only as sustainable as the buying power and interest of anchor customers. Moving to a service-based model will ensure that revenue opportunities are inherently long-lasting.

Pipelines supporting the long-term analysis and delivery of market insights, through a subscription and expanding beyond algorithms to easy-to-use platforms, are just some ways to develop a service-based model.

Recent funding for companies such as Orbital Insight, Ursa Space, and Descartes Labs support this move, with each company stating the need to expand partnerships and international sales operations, as well as in improving the technology behind their pipelines specifically to ensure a more frequent, ongoing delivery of insights to their customers. SpaceKnow, who also received funding this year, continues to make headlines due to insights delivered over Bloomberg terminals worldwide.

Bottom Line

Until now, most of the effort has been in creating and improving the technology responsible for extracting information from imagery. Artificial intelligence, machine learning, and vertical-specific algorithms are sure to increase the information/pixel ratio, increasing the value of the process and final product. Yet, there is a difference between technological capability and commercial sustainability.

Service-based Big Data analytics applications may be the most difficult to develop, necessitating not only timely and precise information, but accessible and relevant insights. However, these challenges, once overcome, expand the market outside of the norm, beyond traditional markets, and will represent the greatest revenue opportunity for players in this space.