Earth’s watchdogs: Satellites leading the charge against climate change

The growing global awareness and imperative to address climate challenges has made Earth Observation (EO) a critical asset for businesses and governments worldwide in their quest to combat climate change effectively. Indeed, EO serves as a vital tool for monitoring climate change. To address climate challenges, assesses vulnerabilities, and manage disasters, EO has become a critical asset as businesses and governments worldwide are increasing monitoring climate policies in an attempt to make informed decisions in renewable energy, agriculture, and conservation. What are the catalysts then for climate change applications for Earth Observation? Is the solution a one-off or a convergence of market dynamics, regulatory frameworks, and cutting-edge EO technologies?

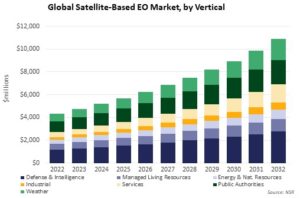

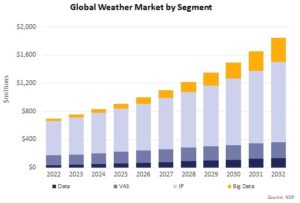

NSR’s satellite-based Earth Observation 15th edition forecasts cumulative opportunity in this field to reach a substantial $78.5 billion across seven verticals. Weather-related applications represent a significant portion of this opportunity, growing at a robust CAGR of 10.3%, accounting for 16.3% of the total revenues. However, the impact of climate change initiatives extends beyond weather monitoring and across multiple verticals.

Verticals such as Energy is Natural Resources, Industrial, Services are seeing greater compliance needs with regulations introduced to combat climate change. The Public Authorities vertical is tied to government spending on data and analytics for identification of influencing factors and implementation of regulatory framework. In addition, it increases the opportunity for new data types such as greenhouse gas (GHG) emissions monitoring, and Thermal Infrared (TIR) monitoring. There is increased investment in climate change monitoring: Airmo, OroraTech, Kayrros and GHGSat are all actively targeting GHG emissions monitoring and TIR data for climate change action and all aim to have direct impacts on the economics that climate change brings to sectors such as oil and gas.

Oil and Gas Customers to lead adoption

North America is set to take the lead in global investment for advanced methane detection within the oil and gas industry. This dominance can be attributed to the substantial volume of assets requiring meticulous monitoring, notably in the Permian, Anadarko, and Appalachia basins of the United States. The impetus behind this surge is multifaceted, driven by both regulatory mandates and corporate objectives aimed at mitigating methane emissions, thereby fostering environmental sustainability and regulatory compliance within the sector.

The United States, Canada, and Europe stand out for having the most rigorous regulations pertaining to methane emissions. In addition to stringent governmental oversight, publicly traded oil and gas companies are encountering mounting pressure from investors to embark on a process of “demethanization” that involves actively reducing and ultimately eliminating methane emissions from their operations.

There is increased interest for satellite data utilisation by Insurance Providers too, such as AXA Climate focusing on loss related to climate change for managed living resources, public and industrial sectors that NSR sees growing at CAGRs of 8%, 8.7% and 10.6% respectively.

Regulations to shape the market uptake

ESG (Environmental, Social, and Governance) regulations are poised to have a positive influence on Earth observation markets as well by spurring heightened demand for environmental data, stimulating innovation and investment in Earth observation technologies, and providing a reliable income source for companies specializing in environmental data services.

The stakes for ESG action are set to rise due to a convergence of factors, including regulatory mandates for ESG disclosures and growing pressure from diverse stakeholders. Although, these regulations could entail compliance expenses, data privacy apprehensions, and potential market consolidation as the industry adjusts to the growing emphasis on sustainability and responsible corporate practices, ultimately transforming and expanding the EO market.

According to NSR’s Space ESG Assessment report, at least 70% of companies surveyed are expected to meet at least one regulatory requirement to report Greenhouse gas (GHG) levels within the next five years. With the right impact and price-point, the EO market is positioned for significant revenue capture potential as the Space & Satellite industry takes its place in the emission ESG TAM.

The Bottom Line

In the ongoing race to combat climate change, it’s abundantly clear that Earth Observation (EO) is no longer relegated to a mere afterthought; instead, it stands as a vital tool for collecting actionable data, reducing emissions, and ensuring a sustainable future. Whether it’s tracking greenhouse gases, supporting climate-vulnerable regions, or assisting industries in meeting increasingly stringent regulations, EO takes centre stage in the battle against climate change.

ESG regulations are poised to further shape the EO market, boosting environmental data demand, fostering innovation, and providing a reliable income stream. As the industry adapts to these changes, the Earth observation market is set to evolve and expand, with significant revenue capture potential in the growing emissions ESG market. Satellite operators and downstream service providers should increase customer awareness of utilisation of satellite data for action against climate change and tailor the products to address specific needs of the end users.